After a decade of low to negative free cash flow (FCF), the oil and gas industry now has an abundance of it in 2024, according to Bloomberg. Despite stronger balance sheets, many investors may be underweight in the sector, creating potential missed opportunities.

Elevated oil prices, strong demand, and production cuts by oil exporting countries benefit fossil fuel companies. The strong cash flow means these companies, in turn, require less leverage. According to Bloomberg data, in 2023, oil and gas company loans fell 6% year-over-year.

The industry’s leverage ratio (a measurement of a company’s ability to meet its financial obligations) dropped to 0.8 last year from 2.4 in 2020. This ratio is calculated using net debt divided by earnings before interest, taxes, depreciation, and amortization.

Reduced leverage alongside robust FCF creates healthy balance sheets for the industry. What’s more, Bloomberg Intelligence forecasts for increasing FCF-to-CapEx through 2030 for the industry. Capital expenditures (CapEx) are the funds a company uses to maintain, acquire, and upgrade its fixed assets, while FCF is the remaining cash a company has after covering all expenses. It can be used to invest in growing the business, pay dividends, or pay down debt.

Oil and gas companies generated an FCF-to-CapEx of 1.0 last year, up from 0.4 in 2020. Bloomberg forecasts that ratio to grow to 1.4 by 2030.

Boost Energy Sector Exposure Through FCF Focus

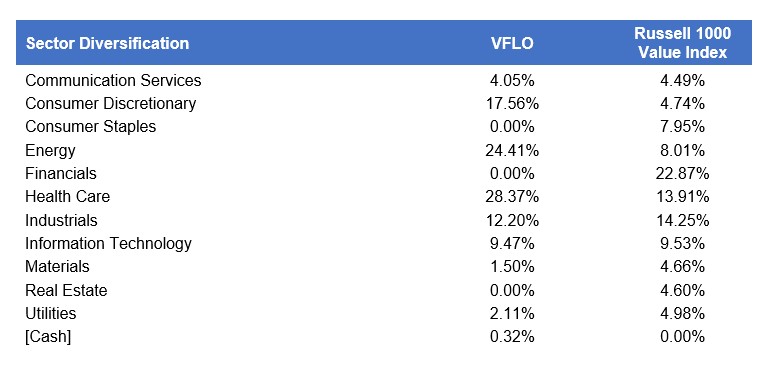

Major equity indexes such as the S&P 500 or the Russell 1000 Value currently underweight the energy sector. The S&P 500 Index held a 3.65% weight to the energy sector as of 6/30/2024. Meanwhile, the Russell 1000 Value Index offered 8.01% weight to the energy sector as of the same date.

Considering the current backdrop for energy, ETFs such as the VictoryShares Free Cash Flow ETF (VFLO) have a larger weight to this sector, given its approach’s focus on FCF. VFLO invests in quality companies with high FCF yield and tracks the Victory U.S. Large Cap Free Cash Flow Index (the Index).

FCF yield considers a company’s enterprise value or its total value, including debt. Enterprise value is calculated by dividing the cash left over after paying capital and operating expenses by the enterprise value.

VFLO has the potential to deliver diversified sector exposure for portfolios through its FCF yield focus. The ETF carried a weighting of 24.41% to the energy sector as of 6/30/2024.

When screening companies, VFLO’s methodology calculates FCF holistically by including both trailing and expected FCF. The Index also applies a growth filter intended to eliminate companies with high FCF but with weak growth prospects.

VFLO may provide one solution to diversifying a portfolio, adjusting to provide sector exposures that offer the highest FCF yields.

VFLO carries a net expense ratio of 0.39% and a gross expense ratio of 0.66%.

Net expense ratios reflect the contractual waiver and or reimbursement of management fees through at least December 31, 2024.

For more news, information, and analysis, visit the Free Cash Flow Channel.

VettaFi LLC (“VettaFi”) is the index provider for VFLO, for which it receives an index licensing fee. However, VFLO is not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of VFLO.

²/ FCF yield is based on the weighted average of index constituents and is equal to the expected FCF divided by enterprise value. Expected FCF is the average of the trailing 12-month FCF and the next 12-month forward FCF. Enterprise value measures a company’s total value and is often used as a more comprehensive alternative to equity market capitalization.

Disclosure Information

Carefully consider a fund’s investment objectives, risks, charges, and expenses before investing. To obtain a prospectus or summary prospectus containing this and other important information, visit http://www.vcm.com/prospectus. Read it carefully before investing.

All investing involves risk, including the potential loss of principal. Please note that the Fund is a new ETF with a limited history. The Fund has the same risks as the underlying securities traded on the exchange throughout the day. Redemptions are limited, and commissions are often charged on each trade. ETFs may trade at a premium or discount to their net asset value. The Fund invests in securities included in, or representative of securities included in, the Index, regardless of their investment merits. The performance of the Fund may diverge from that of the Index. Investing in companies with high free cash flows could lead to underperformance when such investments are unpopular or during periods of industry disruptions.

The Fund could also be affected by company-specific factors that could jeopardize the generation of free cash flow. Derivatives may not work as intended and may result in losses. Large shareholders, including other funds advised by the Adviser, may own a substantial amount of the Fund’s shares. The actions of large shareholders, including large inflows or outflows, may adversely affect other shareholders, including potentially increasing capital gains. The value of your investment is also subject to geopolitical risks such as wars, terrorism, environmental disasters, and public health crises; the risk of technology malfunctions or disruptions; and the responses to such events by governments and/or individual companies.

Additional Information

The Victory U.S. Large Cap Free Cash Flow Index aims to select high quality companies from its starting universe by applying profitability screens. It then selects companies with the strongest free cash flow yield that exhibit higher growth. The Index is rebalanced and reconstituted quarterly. This Index calculates free cash flow yield by dividing expected free cash flow by enterprise value. Expected free cash flow is the average of trailing 12-month FCF and next 12-month forward free cash flow. Enterprise value (EV) measures a company’s total value, often used as a more comprehensive alternative to equity market capitalization.

Distributed by Foreside Fund Services, LLC (Foreside). Foreside is not affiliated with Victory Capital Management Inc. (VCM), the Fund’s advisor. Neither Foreside nor VCM are affiliated with VettaFi.

20240809-3770123