Ever since tensions ratcheted up in the Middle East earlier this year, inflation has resurfaced as a primary concern for advisors and investors alike. As such, every monthly Consumer Price Index (CPI) report is highly anticipated, serving as the ultimate benchmark for tracking inflation.

Key Takeaways:

- The June 2026 CPI report findings are significantly better than analyst expectations.

- However, although energy prices temporarily dropped during the potential Iran War ceasefire, the recent rebound suggests inflation may not be behind us just yet.

- While there are different approaches to navigating this current fixed income market, short-duration bonds could offer a compelling path forward.

The June 2026 CPI report was recently released by the Bureau of Labor Statistics (BLS), and interestingly, U.S. consumer prices fell well below analyst expectations. Monthly inflation slowed by 0.4%, outperforming analyst forecasts by 0.2% and marking the largest single-month decline since April 2020.

Currently, the annual rate of inflation sits at 3.5%, falling below analyst expectations of 3.8%.

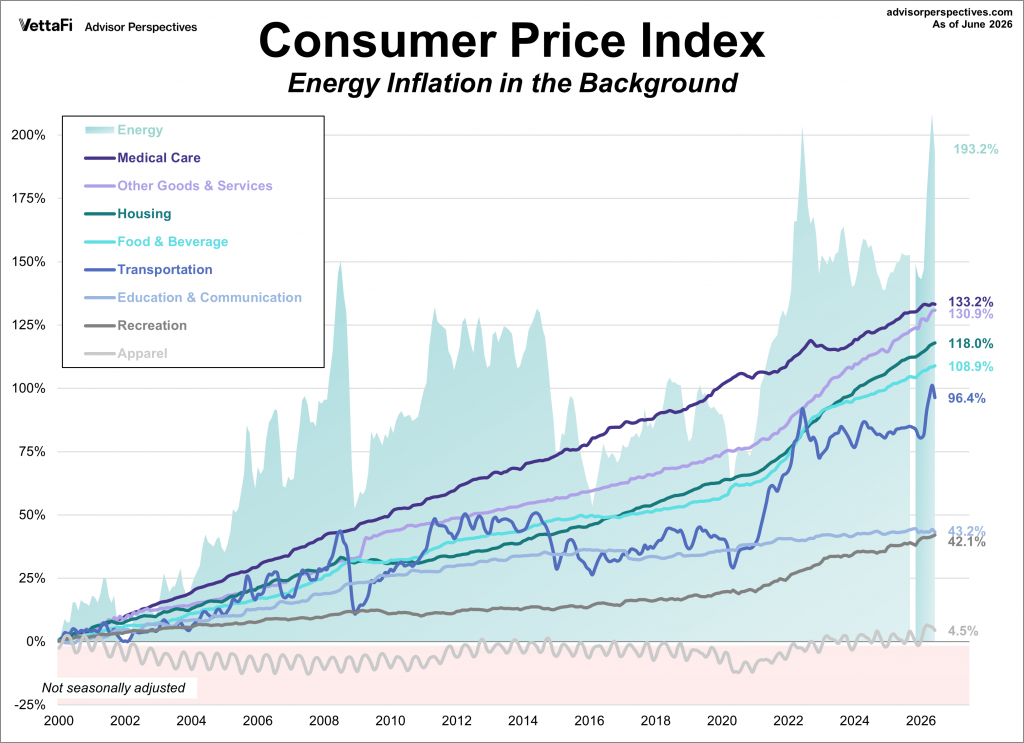

The Energy Factor

Not surprisingly, energy was the key factor driving the report. Gasoline prices dropped 9.7% in June compared to May’s report. This was due in part to the temporary cease-fire in the Middle East. However, July is shaping up to be a different month entirely; Tensions have escalated once more, and prices are back on the rise.

Energy can have a crucial effect on the different expenditure categories of the CPI. The following chart from Jennifer Nash, VettaFi economic and market research analyst, shows how energy inflation adversely challenges the other expenditure categories.

See More: Inside the Consumer Price Index: June 2026

The Investment-Grade Corporate Opportunity Set

This scenario creates tricky terrain for advisors and investors. Normally, a cooling CPI would indicate that rate cuts are on the horizon, but today’s broader macroeconomic picture shows that inflation may be sticking around for a while longer.

While there are several ways to approach the fixed income landscape, short-duration bonds currently stand out as a premier route. To start, ultra-short fixed income could provide lower exposure to interest rate shifts. Given the Federal Reserve’s uncertain path forward, this is a highly valuable benefit and a critical tactical buffer that may prove to be useful for the months ahead.

Furthermore, shorter duration allows advisors and investors to recover capital more quickly. This can help folks redeploy their assets as the economic environment begins to shift.

The Guggenheim Ultra short Income ETF (GCSH) offers access to ultra-short fixed income combined with the flexible benefits of active management. Its active portfolio team targets compelling yields through complexity premiums, all while keeping capital preservation at the forefront.

Ultimately, this tactical approach helps equip advisors and investors to navigate today’s shifting fixed income environment. Having a fund that can potentially outperform the short-duration bond market, while being nimble enough to protect one’s capital, could pay dividends regardless of what inflationary conditions the market faces.

For more news, information, and strategy, visit the Fixed Income Content Hub.