When it comes to planning strategically for future expenses, consumers have a number of ways to use their cash. One of the ways is through bond exchange-traded funds (ETFs), particularly of the ultra-short variety.

Consumers can also invest their money until the time comes to utilize that cash. Often times, the notion of investing money is looking towards the long-term horizon in order to realize a return — this could be through the use of liquid assets like stocks or illiquid ones like real estate. In the short-term, the instruments for investment are different. They can range from money market accounts, Treasurys, certificates of deposits (CDs), or even simply just staying in cash by parking it in a savings account.

Staying in cash may seem like a zero risk proposal. However, in times of rising inflation like right now, staying on the sidelines might not be the most optimal choice. One might be missing out on the opportunity cost of earning a return.

“Holding excess cash for too long carries its own risks, including missing market rallies, failing to keep pace with inflation, and, not least, falling short of asset-accumulation goals,” noted Vanguard senior investment product manager Ian O’Brien.

This is where ultra-short bond ETFs can offer benefits. Cash is put to work earning a return.

“These ETFs are low-cost, have limited volatility, are highly liquid, and often offer more attractive yields than historically popular cash instruments, such as bank accounts, CDs, and money market funds,” O’Brien noted.

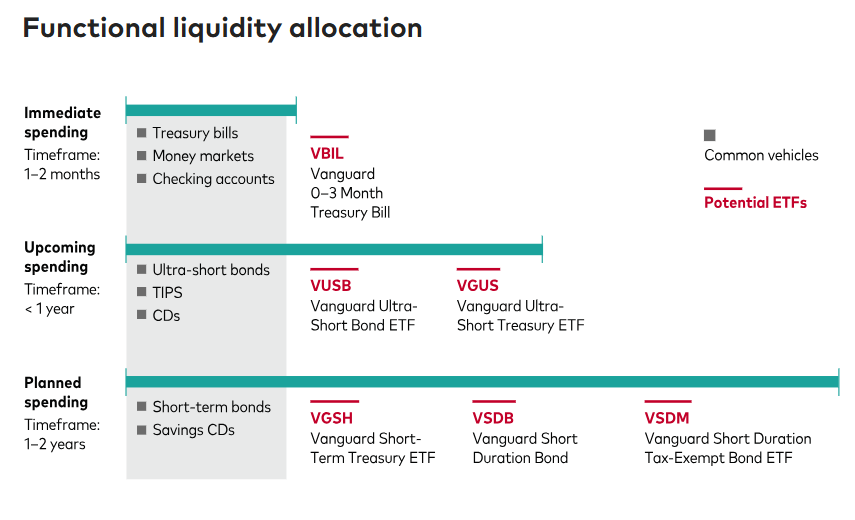

Knowing which ultra-short bond to choose will depend on the timeframe. Is the cash needed for future spending immediate (one to two months), upcoming (in less than a year) or something planned (in the next one to two years)?

2 Options to Manage Yield and Risk

The funds mentioned in the table above to help meet upcoming spending (after two months and up to a year) include the Vanguard Ultra-Short Bond ETF (VUSB) and the Vanguard 0-3 Month Treasury Bill ETF (VBIL). As noted, both offer compelling alternatives to other instruments that earn interest.

VUSB invests in a wide variety of bonds, mostly high-quality and investment-grade to limit credit risk. This includes asset-backed, government, and investment-grade corporate bonds to maximize yield. With that, it has a 30-day SEC yield of 4.51% as of August 13.

With a low 0.10% expense ratio, VUSB offers the flexibility of active management that allows portfolio managers to tailor the holdings to suit current market conditions. This adds an additional risk mitigation component for the fund.

With a low 0.07% expense ratio, VBIL tracks the Bloomberg US Treasury Bills 0-3 Months (the Index). As of August 13, it offers a 4.23% 30-day SEC yield while tracking low-risk, safe haven U.S. Treasury Bills carrying maturities of three months or less.

While they may not offer the immediate access and capital preservation characteristics of other vehicles, their low volatility, low cost, and high liquidity give investors a potentially valuable tool for managing their liquidity needs.

For more news, information, and strategy, visit the Fixed Income Content Hub.