Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

My recent article, The End of an Era for Stocks, warned that a tremendous 30-year tailwind for corporate earnings is dying. Consistent declines in corporate interest and tax rates significantly boosted stock prices and valuations. But with effective corporate interest rates near record lows and tax rates at their lowest levels ever, further reductions are improbable. Barring negative interest rates or reductions in corporate taxes, earnings growth rates in aggregate may shrink 30-50% over the coming decade.

The article’s advice is something all investors should appreciate, not just short-term portfolio managers.

Regarding long-term strategic thinking, it’s worth considering another critical factor for equity investors. There is an alternative. Investors can now lock in a long-term risk-free return of 4% or slightly more.

The question of how much to allocate to stocks versus bonds or other assets should be based on shorter-term fundamental and technical analysis. But for those inclined to set their investment strategies on long-term factors, such as many retirement account investors, the next 10 years may be vastly different than what we are accustomed to.

For those in the set-it-and-forget camp, I explain why the combination of bonds with higher yields and my longer-term earnings growth warnings present an excellent time to reconfigure your stock/bond allocations.

Valuations matter

Valuations are the prices we pay for investments. It is the most critical arbiter of future returns.

As Warren Buffett once said:

Price is what you pay. Value is what you get.

One’s economic and fundamental outlook may be horrendous, but an investment can still make a lot of sense at a cheap enough valuation. Conversely, a stock with an extremely high valuation may be predicated on an impossible earnings trajectory. Even in the best of environments, such investments tend to do poorly.

Valuations and future returns

What does our crystal ball predict based on current valuations?

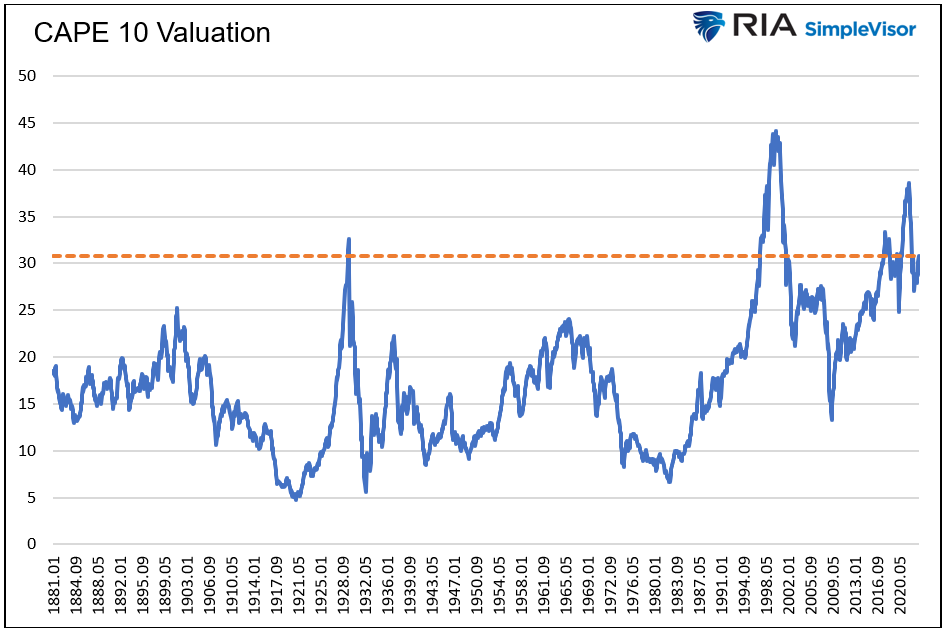

CAPE 10, a longer-term measure of price to earnings of the S&P 500, is 30.82. Going all the way back to 1871, today’s valuation has only been exceeded by a brief period leading to the Great Depression, another before the dot-com bubble crash, and varying occasions since 2017.

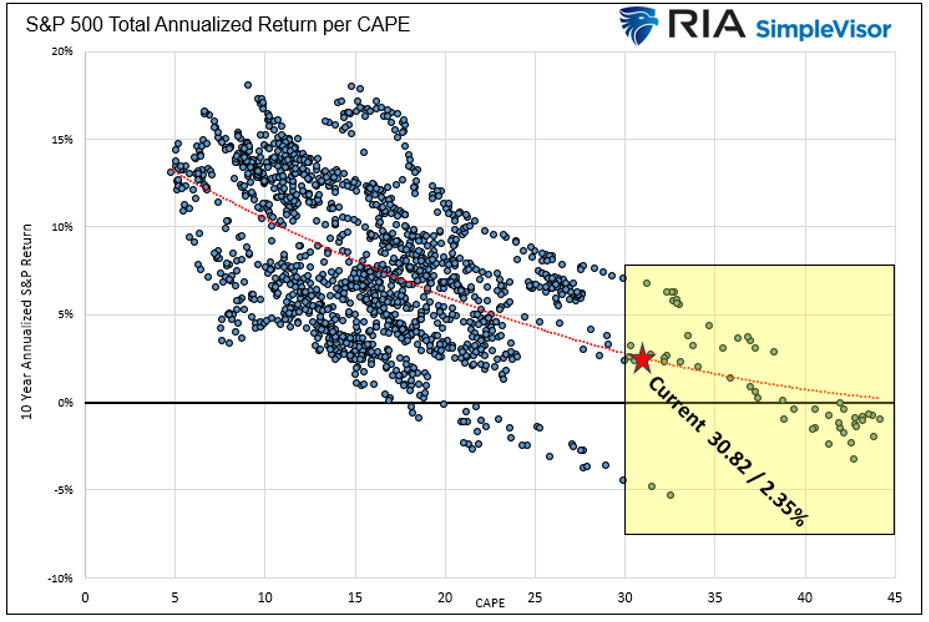

The following scatter plot compares the monthly CAPE valuations with the actual forward 10-year total returns (including dividends).

The red star marks the intersection of the trend line and the current CAPE. Based on a CAPE of 30.82 the 10-year expected total return is 2.35%. The yellow box highlights the ensuing 10-year total returns for each monthly instance CAPE was over 30.

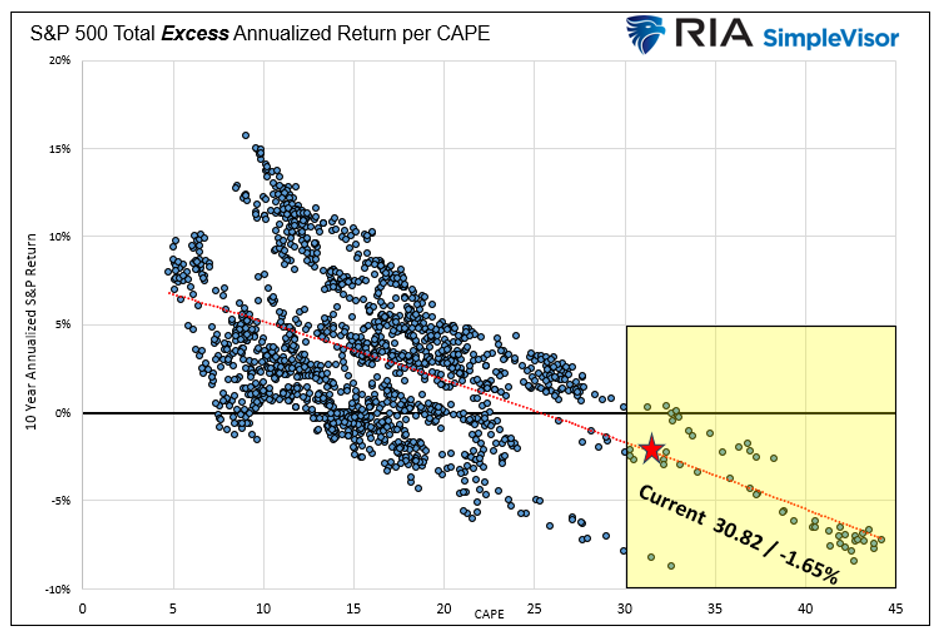

Ten-year U.S. Treasury yields are about 4%. Such a yield provides investors with an alternative that was unavailable over the last 15 years.

The following graph illustrates the tradeoff between the potential range of returns graphed above and the 10-year yields one could have locked in each time the CAPE valuation was over 30. The plot is similar to the one above, except the returns are presented in excess of 10-year U.S. Treasury returns.

Over the last 150 years, investors faced with CAPE valuations over 30, as they are, were almost always better off buying the 10-year U.S. Treasury.

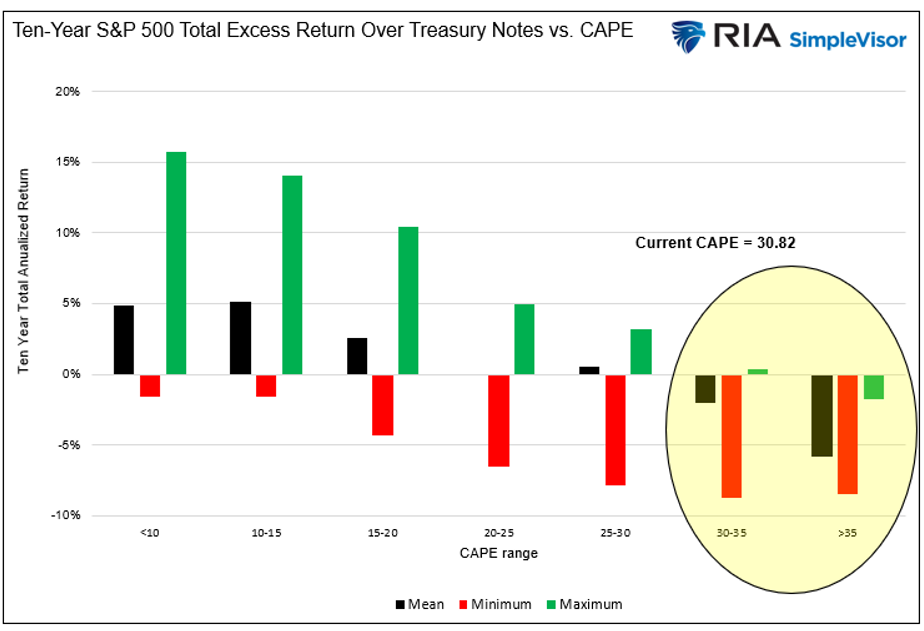

The bar chart below summarizes the scatter plot above to help highlight the point.

History says to take the bonds and run!

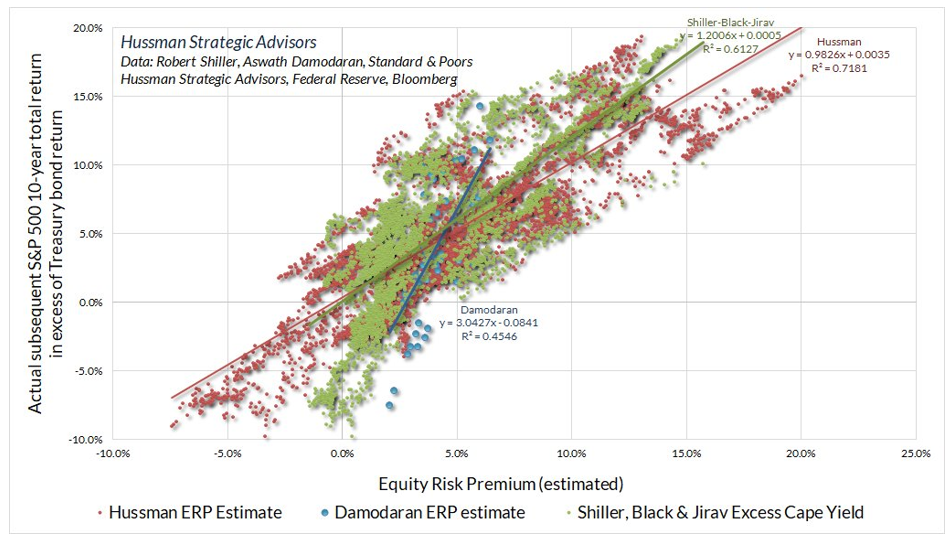

John Hussman add his two cents

John Hussman’s graph below compares three equity risk premium calculations instead of CAPE and compares them to the subsequent excess returns. His analysis is more bearish than the CAPE-based expectations.

With equity-risk premium below 1%, long-term investors best take notice.

The flaw in my analysis

After that bearish discussion, why not buy bonds and sell your stocks? Why not set it and forget it?

While the analysis is very compelling, it’s also flawed. If the market corrects over the next year by 40%, its annual returns for the remaining nine years can be over 6%, yet still attain a near-zero 10-year return. Conversely, stock investors may earn much better than average returns over the next few years only to get hit with a substantial drawdown down the road.

Timing matters. Accordingly, shorter-term technical and fundamental analysis should largely determine your stock/bond allocation unless you are willing to ignore the markets for 10 years.

Summary

History, analytical rigor, and logic argue that long-term buy-and-hold investors should shift their allocations from stocks toward bonds.

For all other investors, pay close attention to your technical, fundamental, and macroeconomic forecasts, as the outlook for stocks versus bonds over the next 10 years is troubling.

Michael Lebowitz is a portfolio manager with RIA Advisors and author for Real Investment Advice. For more information contact him at [email protected] or 301.466.1204

Originally published by Advisor Perspectives on August 3, 2023.

For more news, information, and analysis, visit the Fixed Income Channel.