It’s midsummer, and U.S. small-caps have finally showed up in a big way. You could say it’s been a long time coming. If we look at the iShares Russell 2000 ETF (IWM) versus the iShares Russell 1000 ETF (IWB) as proxies for the small-cap versus large-cap segments, respectively, we are reminded of why small-caps had been out of favor for so long.

As a segment, they had been persistently underperforming their large-cap peers across several time frames, including year-to-date, in the past one year, in the past two-, three-, four-, and five-year periods, VettaFi PRO data shows.

Then, suddenly, small-caps emerged as the blockbuster hit of the summer, delivering a dizzying rally in a matter of days.

How dizzying?

Consider this great chart (below) that plots the Russell 2000 index (small-caps) relative to the Russell 1000 index (large-caps) over the years, courtesy of Jim Bianco, of Bianco Research. To quote Bianco, who shared his views on X this week (July 17), the move we just witnessed was the biggest small-cap outperformance relative to large-caps in a five-day period ever. (If we look at the S&P 600 as measured by the SPDR S&P 600 Small Cap ETF (SPSM), results are similar.)

By Bianco’s assessment, it’s been a historic move. And he’s not alone. Macro strategists and market experts have all been chiming in, looking to make sense of the rally, tying it to economic conditions, to the rate outlook, to a cyclical rotation, to a valuation play, to data, to technicals, to politics — you name it. Explanations run the gamut.

We seem to lack a consensus view on the drivers of this rally, and we’re all wondering how far it will run. But we are all captivated by it nonetheless. And many of us are now looking to revisit the opportunity set in small-caps.

ETFs Fit for Purpose

This is where U.S. small-cap ETFs come in. There are many ways to access this space with ETFs, each fit for a different purpose and outcome. Let’s consider a few examples.

For starters, you can take the “just-own-the-market” approach with a broad, low-cost passive ETF such as IWM and SPSM. One is tied to the Russell view of the world; the other tracks the S&P 600. These “easy-button” choices hit all the right notes. They are large funds with ample liquidity, they trade efficiently and often, they are transparent, tax efficient, broadly diversified, and cheap. There are others like it from many providers.

But you could take a different approach. For example, you could explore the small-cap segment beyond plain market beta and lean into factors, sectors, or strategies that deliver something else.

- Value vs. Growth

The recent move higher in small-cap equities has benefited value, growth, and blended approaches alike. But value has offered a slight edge over its counterparts in the month of July.

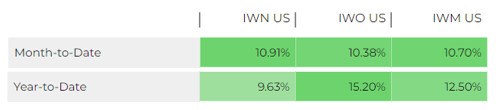

Consider the iShares Russell 2000 Value ETF (IWN) versus the iShares Russell 2000 Growth ETF (IWO) versus IWM, the broader benchmark. Here’s how July-to-date and 2024-to-date returns stack up for the value versus growth versus broad market portfolios:

Perhaps not surprisingly, value has led the rally right out of the gate. And sector differences here are big. IWN has an allocation to financials that’s almost 4x that of IWO in percentage of the overall portfolio, snagging about 26% of the mix. That tilt is notably higher than IWM’s too, which has the sector representing about 17%.

IWN also has almost 10x as much real estate and 2x the allocation to energy versus its growth counterpart. The flip side is that IWO allocates much more heavily into tech at 20% and healthcare at 25%. These are much larger allocations to these sectors than in IWN and IWM alike.

Factor tilts make a big difference. Sector weightings matter. All of these portfolio decisions will come into sharp focus if the move in small-caps is part of a broader rotation into cyclicals, which could continue to benefit value-oriented portfolios.

- Fundamental Quality

Small-cap stocks are often seen as riskier fare relative to larger-cap names. That’s because they are more sensitive to economic conditions, to interest rates, the cost of capital, and so on. If risk management in small-caps is on your mind, focusing on companies with strong fundamental quality relative to their peers could help you stomach the ride.

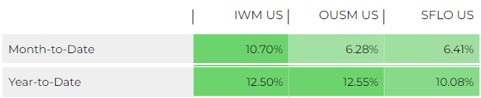

There are a few ways to achieve that. A fund like the ALPS O’Shares US Small-Cap Quality Dividend ETF (OUSM), for example, sets out to capture the opportunity set in small-caps with a keen eye for quality as measured by a track record in dividends. WisdomTree and ProShares also have ETFs in this category.

Another way to think about quality is through a company’s free cash flow yield. That can be both a valuation metric as well as a measure of a business’ financial health. Funds like the VictoryShares Small Cap Free Cash Flow ETF (SFLO) and the Pacer US Small Cap Cash Cows 100 ETF (CALF) navigate this space. The former looks at forward projections of free cash flow yield with a tilt toward quality growth. The latter looks at trailing 12-month yield numbers. (My colleague Todd Rosenbluth recently covered those differences here.)

To be sure, in this recent market move, a tilt toward quality has lagged the broader IWM. That isn’t surprising given that quality stocks, by definition, tend to be more stable and less volatile than their counterparts. So they are slower to burn hot in the early days of a big rally, but they burn hot they most likely will if the rally expands.

- Protection and Income

Covered call strategies and buffer-type strategies can offer some upside participation and some downside protection. That’s something that may appeal to investors nervous about small-cap risk.

The Global X Russell 2000 Covered Call & Growth ETF (RYLG) is an example of this type of approach. The fund offers some upside capture on the Russell 2000 and some protection in the form of a monthly distribution. RYLG is up 6% in the month of July, lagging IWM by about 4 points. But that’s a strong result considering the fund has a distribution yield of about 5.5%.

Another big provider in this space is Innovator ETFs. The issuer has a lineup of month-specific defined outcome strategies targeting upside capture with downside buffers. These include the Innovator U.S. Small Cap Power Buffer ETF – July (KJUL) and the Innovator U.S. Small Cap Power Buffer ETF – October (KOCT).

- Active Management

A few active portfolio managers offer solutions in the small-cap space that have resonated with investors looking for a hands-on approach.

One of the most popular small-cap active ETFs today is the Avantis US Small Cap Value ETF (AVUV). It looks for small-cap stocks offering attractive valuations relative to their profitability. The ETF, which is not even five years old yet, already commands almost $13 billion in assets.

Dimensional, too, has a pair of active small-cap funds: the Dimensional US Small Cap ETF (DFAS) and the Dimensional US Small Cap Value ETF (DFSV).They offer the firm’s management expertise in these corelike portfolios. DFSV has grown to a $3.4 billion fund in little over two years, while DFAS is an $8.8 billion fund.

Finding The Right ETF

These ETFs are just some examples of ways to think about accessing the universe of U.S. small-cap stocks. There are plenty of strategies to choose from, and we’d be happy to help you with our due diligence efforts.

Our ETF Screener can get you started, narrowing down the opportunity set for you. Our VettaFi PRO data platform can help you deepen your research with various tools and charting functionality (all in PDF-ready exportable reports) until you find the one that fits your and/or your clients’ investment goals. If we can be a resource, just holler.

For more news, information, and analysis, visit VettaFi | ETF Trends.

VettaFi LLC (“VettaFi”) is the index provider for OUSM, for which it receives an index licensing fee. However, OUSM is not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of OUSM.