After an unprecedented pause that started in March 2020, student loan repayments will finally resume in October 2023. For borrowers, the pause offered a temporary respite during a tumultuous period. Unemployment surged to 14.7% in April 2020, the highest since the Great Depression, as the pandemic put millions of Americans out of work.

See More: “Graduating With Debt? Here’s How to Manage Your Student Loans Like a Pro“

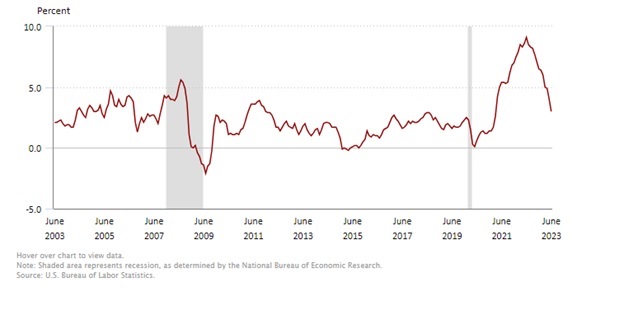

After the unemployment situation abated, a period of high inflation followed, the highest since the early 1980s. The cost of everything from rent to appliances to the most basic necessities has increased rapidly from 2021 through today. The rate has come down from its 9.1% peak last year. However, it remains well above the Federal Reserve’s 2% inflation target.

Source: U.S. Bureau of Labor Statistics, as of June 2023

The government extended student loan forbearance nine times since the pause first began. However, the debt ceiling deal passed by Congress in early June finally put an end to these extensions. Interest will now start to accrue again for student loans starting in September. The first payment is due in October, over three and a half years after the initial postponement.

Making things even more challenging, new grads were looking forward to some sort of loan forgiveness, something the current administration pledged in August 2022. President Biden’s student loan forgiveness proposal intended to forgive federal student debt of $20,000 per individual for those who received Pell Grants, and up to $10,000 for borrowers below a certain income threshold – $125,000 for single borrowers and $250,000 for married couples.

Americans Face $1.8 Trillion In Student Loan Debt

This would have benefited a majority of loanees, as three-quarters of U.S. households have annual incomes below the first threshold. Another 93% are below the second. However, the Supreme Court ruled against this plan in a 6-3 decision handed down in June. The majority opinion stated that such a plan would require congressional approval, or would otherwise be an overreach of executive power. Despite the $430 billion price tag, there is no consensus over whether the plan would have been inflationary or not.

More than 44 million Americans face repaying $1.8 trillion in loans – an average loan balance of about $41,000. Many individuals may have become accustomed to not making student loan payments during the pause. They also may have allocated those funds elsewhere, such as towards a home or discretionary nice-to-have items. The resumption of payments can cause sudden financial strain, especially for those who are still recovering from financial setbacks due to the pandemic or other reasons.

Even before the resumption of student loan repayments, borrowers are facing strains elsewhere. Recent research from the CFPB shows that 8% of student loan borrowers are more than 60 days behind on other credit products. This delinquency rate is higher than before the pandemic. Aside from this highest-risk cohort, 20% of borrowers also have risk factors suggesting they might struggle when scheduled payments resume.

The median scheduled payments on other obligations, such as credit card debt, have increased by 24 percent for those returning to repayment in October. This is due to the dramatic increase in interest rates over the period. The benchmark Federal Funds rate rose from 0% to 5.50% at the July Fed meeting.

“Not All Doom & Gloom”: Possible Solutions & Reprieves

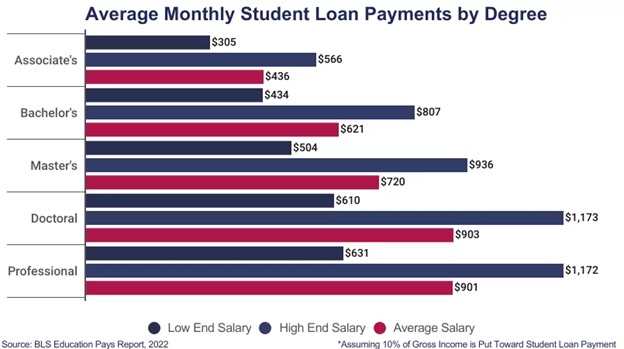

Those most affected will have to cut back on discretionary spending to make ends meet. The monthly repayment for those with Bachelor’s degrees is north of $600, while for those with Master’s, it is over $700. Individuals with average salaries that follow the basic 50-30-20 rule of budgeting may have to trim their budget for non-necessities to 15-20% of spending down from the prescribed 30%.

Source: Consumer Financial Protection Bureau

While the upcoming student loan repayments are daunting for many, it’s not all doom and gloom. Since March 2020, the average borrower has saved $15,000 as a result of the forbearance. Most loan balances are well above this amount, but if you are in the average, you hopefully have an ample cushion with which to start.

To soften the blow, the Education Department has announced that borrowers will not be reported to credit bureaus for non-payment during the first year, though interest will continue to accrue. Delinquent borrowers through the fall of 2025 will not face wage garnishment, loss of tax refunds, or other harsh penalties.

Low-income borrowers will have additional reprieve under the Biden administration’s Saving on a Valuable Education (SAVE) plan. This is an income-driven repayment (IDR) plan that has the potential to lower borrowers’ bills significantly if they qualify.

The Details Of The Biden Admin’s SAVE Plan

Before SAVE, undergraduate IDR plan payments were set at 10% of discretionary income – those eligible will pay just 5%. Those who also have graduate loans will pay somewhere between 5% and 10%, depending on their mix. Perhaps the best benefit is that the time for forgiveness has been trimmed from 20 to 25 years, to just 10 years, for those with principal loan balances below $12,000. Every $1,000 above this amount adds an extra year for forgiveness.

Single borrowers making less than $32,800 or families earning less than $67,500 would have monthly payments of zero if enrolled. The table below outlines the savings for various income levels and family sizes. For example, a family of 3 making $60,000 would pay just $34 per month, while single borrowers would pay $143 monthly, 38% less than if they had made $60,000.

Source: Department of Education, CNN

Unlike the more expansive blocked program, which would have had a large one-time cost to the government, the estimated $475 billion price tag for SAVE will be incurred over the 10-year life.

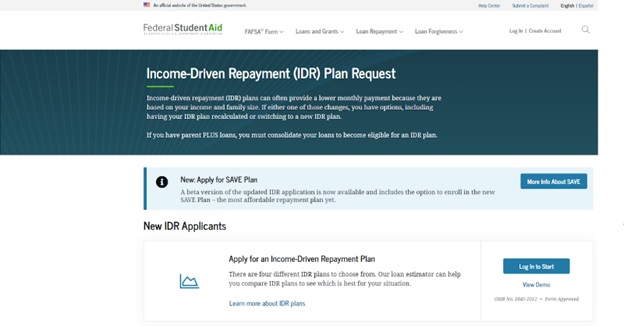

Borrowers interested in signing up can do so at the link here. There you can find out about the benefits mentioned here and various other ones as well. The projected application time is just 10 minutes. You will need a verified FSA ID, your financial information, your personal information, and your spouse’s financial information, if applicable.

Screenshot of new income-driven repayment website. Source: Federal Student Aid

How To Make A Plan To Repay Your Student Loans

If you do not qualify for these new IDR plans, or if you don’t have enough savings to feel secure, the time to make a plan is now. The level of urgency depends on two factors: your loan balance and your interest rate. For federal student loans, the standard repayment plan lasts 10 years, meaning you’ll have to make 120 payments. Rates are fixed, meaning that they won’t fluctuate with interest rates, unlike some private loans.

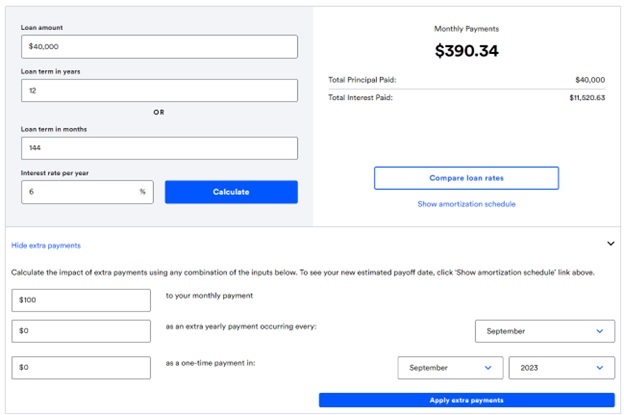

To estimate your monthly payments, you could use online resources, such as this Student Loan Calculator. This will allow you to calculate the impact extra payments will have on the total interest you’d have to pay over the loan’s life.

For example, if you owe $40,000 and have a loan term of 12 years at 6% interest, you’ll owe $390.34 every month. Over the life of the loan, you will have paid off the $40,000 in principal and an additional $16,209 in interest. However, you can add $100 to your monthly payments. Then the loan will have been paid off in 2032 rather than 2035, with $4,689 in total interest savings.

Source: Bankrate.com

Most student loan servicers break up the loans within your account into “groups.” These groups have certain characteristics in common which servicers can then package and sell as asset-backed securities to financial institutions. (Fun fact: iShares tried to make an ETF off of these securities in 2017, but it never went past the prospectus stage).

Importantly, groups likely have different interest rates, and those with higher interest rates should be paid off first, regardless of how large their balance is. This is perhaps the most crucial advice borrowers should take into consideration.

Payments Go To “Past-Due” Student Loans First

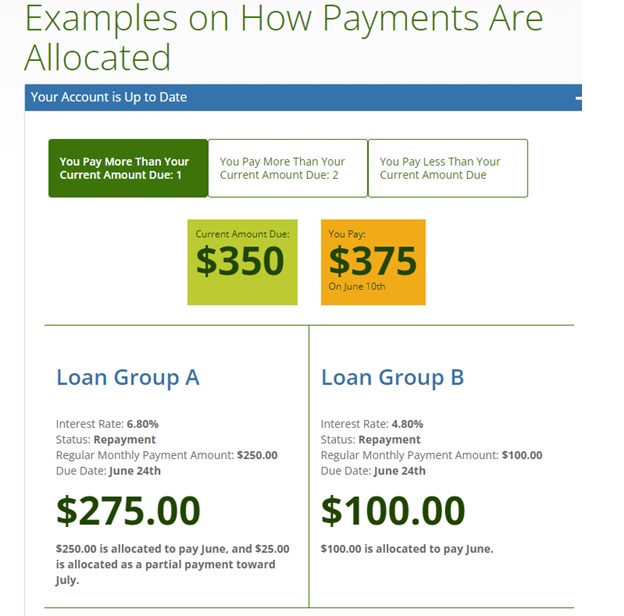

You would think this would be an automatic process, but this isn’t always the case. Student Loan servicer Nelnet uses the following methodology:

Payments are allocated first to any past-due groups. Once all groups are up to date, payments are allocated across groups in an active repayment status, in proportion to each group’s regular monthly payment amount, less any amount already paid for that month.

The first part makes sense. If you’re delinquent on a particular group, this has to get paid off first so you are current on your loan. However, the second part is the kicker: payments are then split among all other groups equally, regardless of their rate. Even if you pay more than your current amount due, this excess may not go toward the lowest interest group, as per Nelnet’s example below.

Source: Nelnet

You should target higher interest loan groups, regardless of their balance, because they are contributing disproportionately to your monthly payment. You may plan on getting forgiveness on your loans after 10 years. However, paying off part of or all of a higher interest group first will lower your interest payment over the remainder of the period. You should be able to find a way to do this online via your lender’s portal. You also can call the lender directly.

Should You Refinance Your Student Loans?

Rates right now are the highest they’ve been in many years. Refinancing, which can be done with either a private or federal loan, makes little sense today unless you took out the loan at a rate well above the prevailing one. For example, international students are unable to utilize federal borrowing and must go with a private lender.

Private loans are competitive, and in many cases carry lower interest than federal loans, but fluctuate based on creditworthiness. If you couldn’t secure a cosigner and lenders did not consider you creditworthy at the time, your rate could be way higher than the current refinancing rate. In limited cases such as these, refinancing makes sense. Note the federal government does not handle refinancing – this must be done with a private institution.

For most other borrowers, this doesn’t mean payment options are paralyzed. Understand how your overall rate compares with current savings rates. For example, if you were lucky enough to get federal direct subsidized and unsubsidized loans at 2.75% for the 2020-21 academic year, it doesn’t make sense to make any excess payments.

You can easily earn over 4% in a bank CD, or north of 5% with low-risk, short-term treasury ETFs. The difference between the two rates is effectively arbitrage, or “free money.” In other words, you owe money at a rate lower than what you can earn.

What Impact Will Rising Interest Rates Have?

However, if you were a graduate student who took out a loan earlier this year, regardless of whether it was private or federal, your rate is likely over 7%. In this scenario, you should seriously consider paying off the loan first. The only thing that can deliver more yield, even in the current environment, are securities with principal risk.

If rates fall meaningfully, it still may not make sense to refinance with a private lender. Federal loans often come with protections and benefits that could be lost if refinanced. Consider whether you’ll lose access to income-driven repayment plans, deferment options, or forgiveness programs.

Furthermore, consider any fees involved in refinancing and weigh them against potential interest savings. Some lenders might charge origination or application fees. Those fees, when added to the loan, may make it unattractive relative to what you currently have.

When It Comes to Student Loans, Don’t Panic. Plan.

Student loan repayments will resume in October 2023. The initial pause began in March 2020 due to the economic challenges of the pandemic. Over 44 million Americans, facing a total of $1.8 trillion in student loan debt, will need to adapt to this change after a period marked by high unemployment and inflation.

The Supreme Court rejected President Biden’s sweeping loan forgiveness effort. However, measures like the SAVE plan have been put in place to help low-income borrowers. Interest will start accruing on student loans from September 2023, with the first payment due in October. Those affected must be prepared for the financial strain, especially considering the rise in interest rates and existing credit delinquencies.

Strategies may include budgeting, exploring income-driven repayment options, or considering refinancing if appropriate. However, refinancing should be approached with caution. Otherwise, federal loan benefits might be lost. Current high interest rates could also make this option unappealing for most borrowers. The current situation is difficult for many and calls for careful financial planning to accommodate the resumption of student loan repayments.

For more news, information, and analysis, visit the Financial Literacy Channel.