It’s no surprise that the growth of ETFs has raised some questions about their size, mechanics, and role in financial markets. Here, we look to answer some of the most popular questions we receive about ETFs and index investing.

Typically, no. In fact, ETFs globally have acted as “shock absorbers” during many volatile trading sessions as buyers and sellers transacted on the exchange, at real-time prices, without having to trade the underlying stocks and bonds.(1)

What’s more, since ETF shares are traded directly by buyers and sellers on-exchange, an ETF can circumvent “forced selling,” something a mutual fund may need to do when investors want to sell their shares. This means that most ETF trading occurs without transactions taking place in the underlying securities.

2. DO ETFs DRIVE THE DIRECTION OF MARKETS?

Given the size of some of the largest ETFs, one might think that buying and selling within those funds significantly moves market prices. However, it is asset allocation decisions made by asset owners, such as pension funds and individuals, that drive flows into different asset classes, sectors, and geographies.

These allocation decisions are generally guided by factors such as macroeconomic developments (like global interest rate policy), risk preferences, and investment horizon.

ETFs are just one way for investors to express their views about the market. If ETFs didn’t exist, investors could use other tools, like single stocks, mutual funds, and derivatives.

3. HOW DO ETFs IMPACT MARKET LIQUIDITY?

Exchange-traded funds (ETFs) are unique; they provide exposure to a diversified collection of assets, like a mutual fund, but trade on exchange, like a stock. This structure makes the liquidity of ETFs unique, too.

Liquidity refers to the ease of buying or selling a security. ETFs have two layers of liquidity: primary market liquidity, which is provided by the underlying securities or instruments of the ETF, and secondary market liquidity, which is provided by the ability to trade ETFs on exchange.

This means that ETFs are net contributors to market liquidity. At a minimum, an ETF will be as liquid as its underlying securities or instruments; however, many ETFs can provide even greater market liquidity than their underlying instruments.

For example, as of December 2022, the iShares iBoxx $ High Yield Corporate Bond ETF (HYG) had a 20-day average bid-ask spread (a component of trading costs for investors) of $0.01 while its underlying portfolio of bonds had an average bid-ask spread of $0.37, reflecting greater liquidity in the ETF versus its underlying securities.(2)

4. HOW BIG IS THE INDEX MARKET?

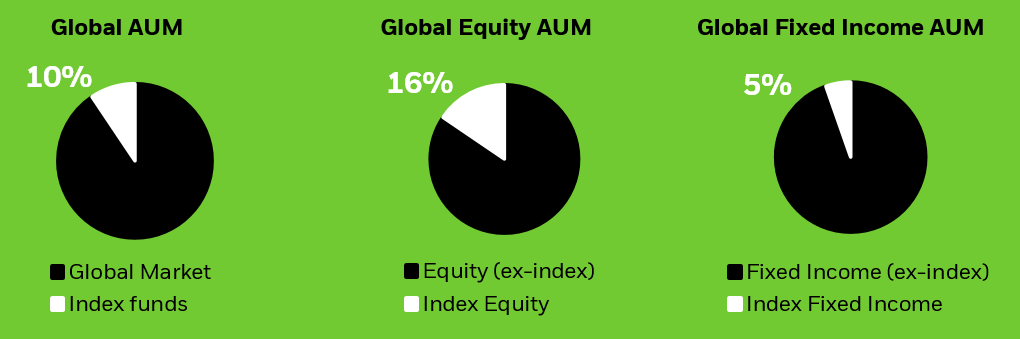

There are roughly $26.1 trillion of index assets worldwide ($19.3 in equity and $6.8 in fixed income).3 This means that index assets, including ETFs and mutual funds, represent just 10% of the global market capitalization, or dollar value of the global market.

Even within the United States — the largest index market — index assets are a fraction of the total financial market. Approximately 25% of the total assets invested in U.S. equities are in U.S.-listed equity index products.4 In fixed income, just 6% of the total U.S. bond market is in indexed assets (Figure 1).

Figure 1: Index funds as a percentage of the market⁵

Chart description: Pie chart 1 shows the assets under management of global index funds as percentage of total equity and fixed income assets. Pie chart 2 shows the assets under management of global equity index funds as a percentage of total equity assets. Pie chart 3 shows the assets under management of global fixed income index funds as a percentage of total fixed income assets. While index funds represent over $26 trillion of assets under management, they still only represent a fraction of total equity and fixed income assets.

5. ARE ALL EXCHANGE-TRADED PRODUCTS (ETPs) THE SAME?

While all ETPs share certain characteristics, like the ability to trade shares on exchange, some have more complex risks and structural features. Examples of these products include defined outcome ETFs and those that seek to provide a leveraged or inverse return of their benchmark.

As the number of ETPs has increased, so too has the number of more structurally complex products, including ETPs with different risk profiles and more narrowly tailored investment objectives.

BlackRock is supportive of efforts to increase awareness and transparency around the risks and structural features of complex products and we have long advocated for a clear categorization of ETPs that may have differing risks and complexities.6

6. DO INDEX REBALANCES MAKE INDEX INVESTING LESS EFFICIENT?

Index providers periodically make changes to, or rebalance, their indexes. This includes adding, deleting, and making changes to the weights of securities in the indexes they manage. Because index funds seek to track the performance an index, they also adjust their holdings when index rebalances happen.

There are a multitude of decisions that must be made leading up to and during index rebalances. At BlackRock, professional index fund managers take a disciplined approach to managing rebalances as they seek to deliver fund performance outcomes that align with index performance.7

Some actively managed funds, like hedge funds, may use knowledge of the indexing process to seek to generate returns by capturing price movements in names added or removed from the index during rebalances, or by predicting index inclusions and deletions before these changes are announced. Even so, this has had minimal impact on index funds.8

7. HOW DOES BLACKROCK MEASURE INVESTMENT PERFORMANCE FOR INDEX ETFs?

At iShares, we measure ETF investment performance not only by how well our ETFs track their indexes, but also by how we deliver the performance our investors expect in a cost- and tax-efficient way. This includes paying close attention to the market quality of our products, or their ability to offer liquidity and efficient access to markets in varying market conditions.9

The first component of our investment performance framework is precision. One of the most important criteria in measuring the performance of index products is how well they deliver or track index returns — and their ability to do so consistently over time. This also includes assessing how efficiently the funds manage index rebalances to optimize outcomes for investors.

For ETFs, iShares uses a second component to measure investment performance: market quality or their ability to offer liquidity, price discovery, and efficient access to markets in varying market conditions. To measure the market quality of an ETF, it is important to consider metrics that span both primary and secondary market activity. Importantly, these metrics must be studied holistically; when reviewed in isolation, one metric may not tell the whole story.

8. HOW DO ETFs IMPACT STOCK PRICES?

Questions sometimes arise about whether ETFs influence the prices of the stocks they hold. In short, the majority of ETF activity doesn’t affect the market prices of underlying stocks.

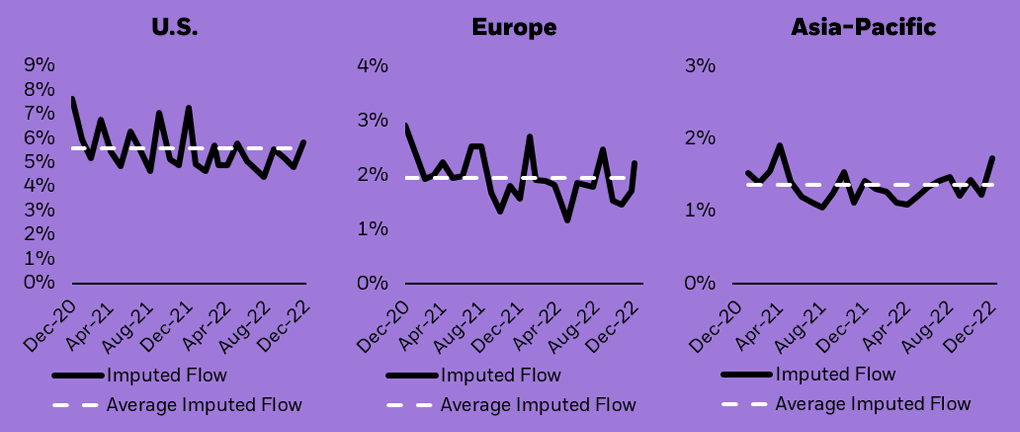

From the period of December 2020 through December 2022, approximately 5.6% of trading volume in U.S. equities has been attributable to ETF activity, while in Europe, just 1.9% of trading in individual European stocks has been attributable to ETF flows. In Asia-Pacific, this figure is 1.4% (Figure 2).

Roughly 80% of U.S. ETF activity takes place on-exchange between buyers and sellers of ETF shares, which means that, most of the time, shares of underlying stocks do not need to be bought or sold to adjust for changes in investor demand.10

Chart description: Line charts showing both the total and average imputed flow in the U.S., Europe, and Asia-Pacific. Imputed flow is an estimation of how stock trading is generated by ETF inflows and outflows. The charts show that imputed flow is below 5.7%, on average, in all regions.

9. WHAT WOULD HAPPEN IF AN AUTHORIZED PARTICIPANT OR MARKET MAKER WITHDREW FROM THE ETF MARKET?

An authorized participant (AP) is a financial institution that manages the creation and redemption of ETF shares in the primary market. Each AP has an agreement with an ETF sponsor that gives it the right (but not the obligation) to create and redeem ETF shares. APs may act on their own, or on behalf of market participants.

Market makers are broker-dealers that regularly provide two-sided (buy and sell) quotes to clients. In some instances, an ETF’s market makers may also be APs.

APs and market makers operate in a highly competitive environment, and are economically incentivized to take part in making or trading ETF shares. Historically, if an AP has withdrawn from the ETF market, other APs have stepped in to facilitate the creation and redemption of ETF shares, particularly if there was a significant premium or discount to its net asset value (NAV), or difference between the price of the ETF and its underlying holdings. This is because APs generally seek to take advantage of economic arbitrage opportunities arising from that difference (for example, if an ETF is trading at a price above its NAV, an AP could buy the underlying securities and exchange them with the ETF issuer for newly created ETF shares, which may then be sold in the market for a profit).

That same incentive holds true for market makers as well.

Ultimately it is this “arbitrage mechanism” that helps keep the ETF’s market price close to the value of its underlying holdings each day.

10. WHAT ROLE DO ETFs PLAY IN PRICE DISCOVERY?

Price discovery helps investors identify the proper market price of securities or other instruments based on factors like supply and demand. The on-exchange trading of ETFs plays an important role in price discovery across markets, sectors and individual stocks. For example, international ETFs traded during U.S. market hours help investors set prices daily when non-U.S. markets are closed. Additionally, during suspensions of international stocks or markets, U.S.-domiciled ETFs may be the primary source of pricing information available to market participants.

ETF flows provide crucial information. As greater numbers of investors use ETFs to express their views, flows from one asset to another can serve as indicators of investor sentiment about potential risk and return. Note that ETFs don’t set prices or drive volatility. They hold up a mirror to what investors are thinking.

11. WHO USES ETFs?

A fast growing segment of ETF users is retail investors. In 2019, U.S. retail investors accounted for 11% of ETF trading volumes; by 2022, this number grew to over 16%.12 We believe the growth in retail investors’ use of ETFs has been driven by a few key factors, including an industry shift to commission-free trading, improved digital experiences on direct platforms, and investor empowerment stemming from greater access to financial education through social media and other forums.

ETFs can be used for a variety of reasons, such as a financial instrument for a tactical decision or as a tool for efficient market access in an investor’s portfolio. With a multitude of use cases, it’s not surprising that ETFs are used by all types of investors.

12. WHY DO FIXED INCOME ETFs ONLY HOLD A SUBSET OF INDEX CONSTITUENTS?

Unlike the U.S. equity market, the U.S. bond market is highly fragmented and opaque. There are hundreds of thousands of unique fixed income securities. Furthermore, unlike equity securities, most bonds don’t trade on a given day.13 These attributes of the bond market can make it challenging for a bond fund to attempt full replication of bond indexes which can include thousands of securities.14

Accordingly, ETFs tracking such indexes are generally “sampled” (i.e., they hold a subset of securities that meet the risk profile and characteristics of the parent index to seek the index exposure). iShares Portfolio Managers evaluate which bonds to select for fixed income ETF portfolios through a systematic process that includes evaluating multiple risk and liquidity factors while seeking to match the risk and characteristics of the benchmark index.

The creation and redemption baskets — the securities delivered by an AP to the ETF for a creation of ETF shares, and vice versa for a redemption of ETF shares — generally aim to be representative of the broader index to maintain the ETF’s investment objective of tracking the index. Sampled baskets lead to a reduced security count relative to the reference index, but the presence of fewer securities does not automatically translate into concentration of risk.

By Samara Cohen

This article was originally published on iShares.com on May 3, 2023.

1 Source: International Organization of Securities Commission “Exchange Traded Funds Thematic Note – Findings and Observations during COVID-19 induced market stresses” (August 2021).

2 Source: Bloomberg, Bank of America, TRACE. As of December 30, 2022. There can be no assurance that an active trading market for shares of ETFs will develop or be maintained.

3 Source: World Federation of Exchanges, Bank for International Settlements (BIS). As of December 31, 2021.

4 Source: Simfund/Broadridge, McKinsey, Markit, World Federation of Exchanges. As of December 31, 2021.

5 Source: Bank for International Settlements, Simfund/Broadridge, McKinsey, Markit. As of December 31, 2021.

6 See BlackRock’s comment letter on FINRA‘s March 2022 Regulatory Notice 22-08 on Complex Products and Options here.

7 For more information on equity index rebalances, see iShares Investigates: Market indexes and index investing | Part 2: Equity index rebalances.

8 For more information on the cost of equity index rebalances, see iShares Investigates: the cost of equity index rebalances.

9 For more information on how iShares measures investment performance, see Take a closer look: ETF and index fund investment performance.

10 Source: BlackRock, Form N-CEN. As of March 31, 2022.

11 Source: Bloomberg, Markit, BlackRock. Derived from the collective weight of flows into all ETFs holding all U.S. stocks on a monthly basis from 2020 through 2022. As of December 30, 2022.

12 Source: SEC Rule 605 Data, Bloomberg. Rule 605 data requires wholesale market makers to provide transparency into their orders and executions. As of December 30, 2022.

13 For more information on bond market and fixed income ETF liquidity, see By the numbers: New data behind the bond ETF primary process.

14 Source: Bloomberg, BlackRock. The Bloomberg U.S. Aggregate Bond Index held 13,133 securities and the iShares Core U.S. Aggregate Bond ETF (AGG) held 9,260 securities. As of December 30, 2022.

Carefully consider the Funds’ investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds’ prospectuses or, if available, the summary prospectuses, which may be obtained by visiting the iShares Fund and BlackRock Fund prospectus pages. Read the prospectus carefully before investing.

Investing involves risk, including possible loss of principal.

Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in the value of debt securities. Credit risk refers to the possibility that the debt issuer will not be able to make principal and interest payments.

Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities.

This material represents an assessment of the market environment as of the date indicated; is subject to change; and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any issuer or security in particular.

This material is provided for educational purposes only and does not constitute investment advice. The information contained herein is based on current tax laws, which may change in the future. BlackRock cannot be held responsible for any direct or incidental loss resulting from applying any of the information provided in this publication or from any other source mentioned. The information provided in this material does not constitute any specific legal, tax or accounting advice. Please consult with qualified professionals for this type of advice.

Shares of ETFs may be bought and sold throughout the day on the exchange through any brokerage account. Shares are not individually redeemable from an ETF, however, shares may be redeemed directly from an ETF by Authorized Participants, in very large creation/redemption units.

There can be no assurance that an active trading market for shares of an ETF will develop or be maintained.

Buying and selling shares of ETFs may result in brokerage commissions.

The Funds are distributed by BlackRock Investments, LLC (together with its affiliates, “BlackRock”).

The iShares Funds are not sponsored, endorsed, issued, sold or promoted by Bloomberg, BlackRock Index Services, LLC, Cboe Global Indices, LLC, Cohen & Steers, European Public Real Estate Association (“EPRA® ”), FTSE International Limited (“FTSE”), ICE Data Indices, LLC, NSE Indices Ltd, JPMorgan, JPX Group, London Stock Exchange Group (“LSEG”), MSCI Inc., Markit Indices Limited, Morningstar, Inc., Nasdaq, Inc., National Association of Real Estate Investment Trusts (“NAREIT”), Nikkei, Inc., Russell, S&P Dow Jones Indices LLC or STOXX Ltd. None of these companies make any representation regarding the advisability of investing in the Funds. With the exception of BlackRock Index Services, LLC, who is an affiliate, BlackRock Investments, LLC is not affiliated with the companies listed above.

Neither FTSE, LSEG, nor NAREIT makes any warranty regarding the FTSE Nareit Equity REITS Index, FTSE Nareit All Residential Capped Index or FTSE Nareit All Mortgage Capped Index. Neither FTSE, EPRA, LSEG, nor NAREIT makes any warranty regarding the FTSE EPRA Nareit Developed ex-U.S. Index, FTSE EPRA Nareit Developed Green Target Index or FTSE EPRA Nareit Global REITs Index. “FTSE®” is a trademark of London Stock Exchange Group companies and is used by FTSE under license.

©2023 BlackRock, Inc or its affiliates. All Rights Reserved. BLACKROCK, iSHARES, iBONDS, ALADDIN and the iShares Core Graphic are trademarks of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

iCRMH0523U/S-2856338