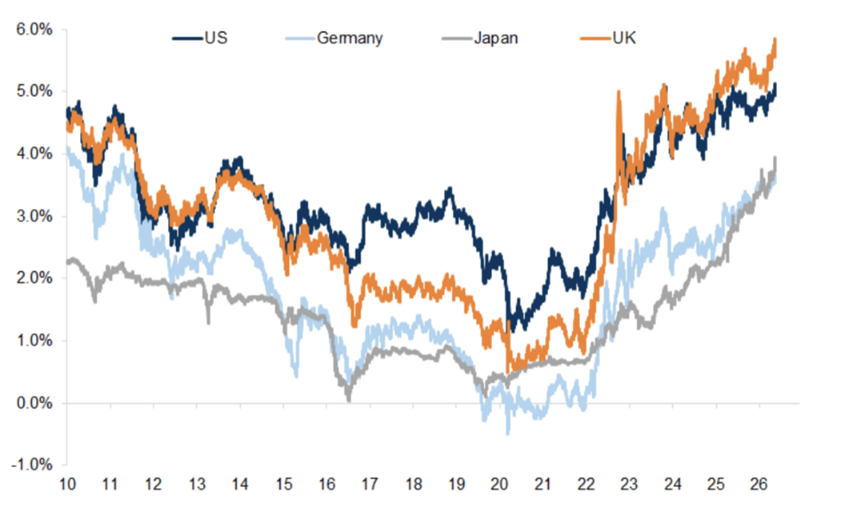

The Federal Reserve’s policy outlook just underwent one of its most dramatic reversals in recent years. Bond yields are rising at an alarming rate in response, and the sudden acceleration has sent shockwaves throughout global markets. The year began with markets comfortably pricing in multiple rate cuts, but the pendulum has swung completely, and ETF flows are responding in kind.

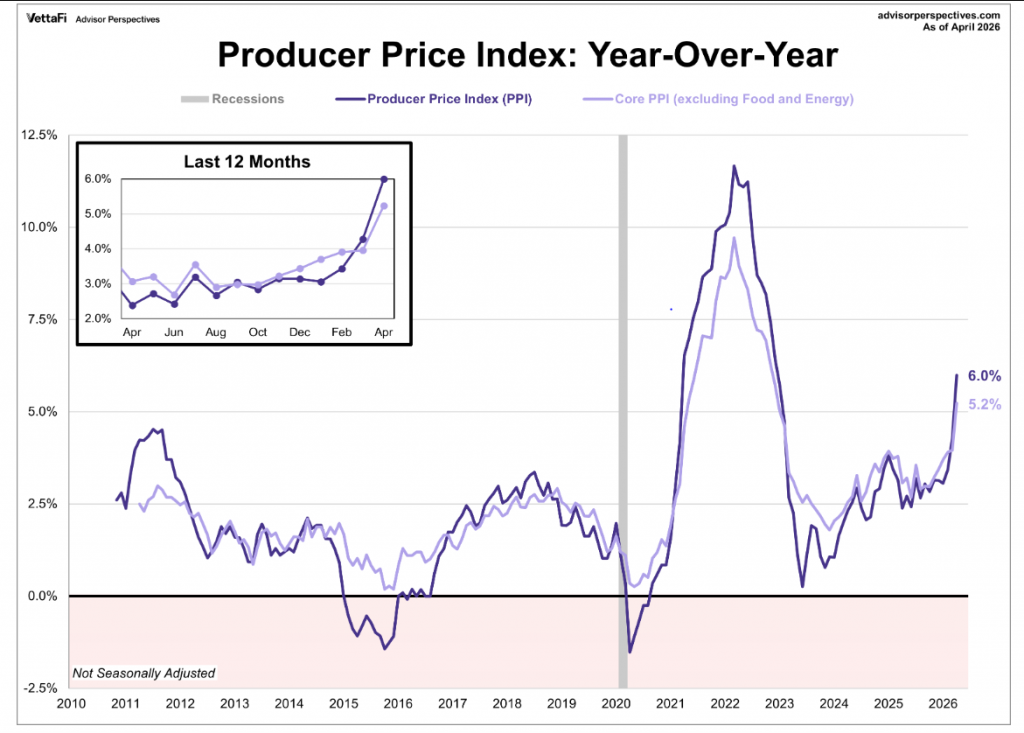

Blame it on surging crude prices and a series of stubborn inflation reports. A hotter-than-expected April CPI print, followed by PPI running hot at 6% year-over-year — the fastest wholesale price increase since 2022 — has sent global bond markets reeling in tandem with U.S. Treasury yields. The Fed held rates steady at its April meeting in a historically contentious vote, with three regional presidents openly calling for a hawkish pivot. Now, Fed Chair Kevin Warsh faces the unique challenge of managing a global energy shock and five-year above-target inflation without upending a resilient labor market.

Blame it on surging crude prices and a series of stubborn inflation reports. A hotter-than-expected April CPI print, followed by PPI running hot at 6% year-over-year — the fastest wholesale price increase since 2022 — has sent global bond markets reeling in tandem with U.S. Treasury yields. The Fed held rates steady at its April meeting in a historically contentious vote, with three regional presidents openly calling for a hawkish pivot. Now, Fed Chair Kevin Warsh faces the unique challenge of managing a global energy shock and five-year above-target inflation without upending a resilient labor market.

“We hit a multi-year high for inflation in April, largely driven by energy price spikes from the Middle East conflict,” said Jen Nash, economic and market research analyst at VettaFi. “The real red flag here is the wholesale surge, which signals that inflationary pressures to the consumer aren’t cooling down anytime soon. Because of this, the Federal Reserve is in a tight spot and the momentum has officially shifted away from rate cuts, putting a rate hike back on the table.”

“We hit a multi-year high for inflation in April, largely driven by energy price spikes from the Middle East conflict,” said Jen Nash, economic and market research analyst at VettaFi. “The real red flag here is the wholesale surge, which signals that inflationary pressures to the consumer aren’t cooling down anytime soon. Because of this, the Federal Reserve is in a tight spot and the momentum has officially shifted away from rate cuts, putting a rate hike back on the table.”

The Fed Funds futures market is currently pegging the odds of a rate hike by December at roughly 60% — with cuts fully priced out through 2027.

Rate-Sensitive ETF Rotation

Investors have wasted no time in redirecting capital out of rate-sensitive sectors. Utilities ETFs have seen nearly half a billion dollars in outflows this month, abruptly reversing a multi-quarter boom driven by AI power demand. Real estate ETFs have similarly hit a wall, thanks to technical resistance and higher borrowing costs creating stiff headwinds for the commercial property market. And financials, including regional banking ETFs, have suffered outflows of $1.4 billion in the face of a “higher-for-longer” regime.

Long-duration bond ETFs have fared even worse. The iShares 20+ Treasury ETF (TLT) experienced its largest two-week outflow since the 2022 hiking cycle as yields marched higher. Instead, investors have aggressively favored shorter-duration fixed income ETFs as they prioritize high cash yields and safety over duration risk. For the moment, several intermediate-duration bonds, such as the Schwab 5-10 Year Corporate Bond ETF (SCHI), have also seen inflows at the expense of longer-duration bond ETFs.

Equity sectors that are more insulated from inflation woes have benefited. Energy ETFs and commodity-linked funds remain dominant magnets for new capital, alongside defense strategies and infrastructure plays. High dividend-focused ETFs continue to absorb steady net inflows from investors seeking cash-rich balance sheets. The Schwab U.S. Large Cap ETF (SCHX) and Schwab U.S. Dividend Equity ETF (SCHD) took in more than $700 million in net inflows each.

The “AI Shield”: Taking Refuge From Rates in Tech

Tech stocks have historically been viewed as high-duration assets, but the “AI factor” has completely rewritten the playbook. AI-linked tech has grown less rate-sensitive lately, with investors increasingly treating AI-linked sectors as long-term strategic infrastructure plays rather than traditional cyclical trades. Massive corporate spending on AI infrastructure is considered highly resilient, shielding mega-cap tech from the worst of the recent interest rate volatility.

Momentum plays like Cathie Wood’s ARK Innovation ETF (ARKK) have been among the biggest winners this past week, along with the red-hot Roundhill Memory ETF (DRAM), as the global memory chip shortage continues to run rampant. Two quality growth titans, the Invesco QQQ Trust (QQQ) and the Invesco NASDAQ 100 ETF (QQQM), have dominated ETF flows, bringing in close to $6 billion and $2 billion, respectively. Another quality-focused ETF, the Schwab U.S. Large-Cap Growth ETF (SCHG), has also seen success — taking in $2.5 billion last week.

See more: ETF of the Week: DRAM

The Bottom Line

Despite the recent action, investors would be wise not to treat this pivot as a permanent structural shift. Even with recent outflows, defensive sectors like utilities remain supported by robust long-term earnings forecasts tied to the grid modernization and AI power demand. Headlines surrounding the Strait of Hormuz and the stability of global crude oil flows could change on a dime. While there is a sharp tactical rotation into cash proxies and less rate sensitive sectors, history suggests these flows can pivot just as fast as the macro narrative changes. For now, investors are playing defense — but keeping their running shoes on.