On May 1, the United Arab Emirates (UAE) formally exited both the Organization of the Petroleum Exporting Countries (OPEC) and the broader OPEC+ grouping of major oil producers. Such exits are not unheard of. For example, Indonesia suspended its membership in OPEC in 2015. However, Indonesia left the cartel not because it wanted to produce more oil, but because it had become a net oil importer. Qatar left the cartel in 2019, but there were several factors that led to its exit, including the fact that it had become more of a natural gas producer and Saudi Arabia and the UAE had isolated the country over its fostering of the news organization Al Jazeera.

Unlike Indonesia, the UAE has excess oil production capacity that represented about 25% of the cartel’s total. Like Qatar, tensions between Saudi Arabia and the UAE are elevated. The two countries have supported opposing sides in Yemen, for example.

In the immediate term, the UAE’s decision won’t affect the oil markets significantly. That’s because the Strait of Hormuz remains mostly closed. Although the UAE does have a pipeline to the Gulf of Oman, bypassing the strait, it is currently already fully utilized. Thus, the UAE can’t increase its oil output or exports until the US-Israeli war against Iran comes to some sort of resolution. But once that occurs, there will likely be a market impact.

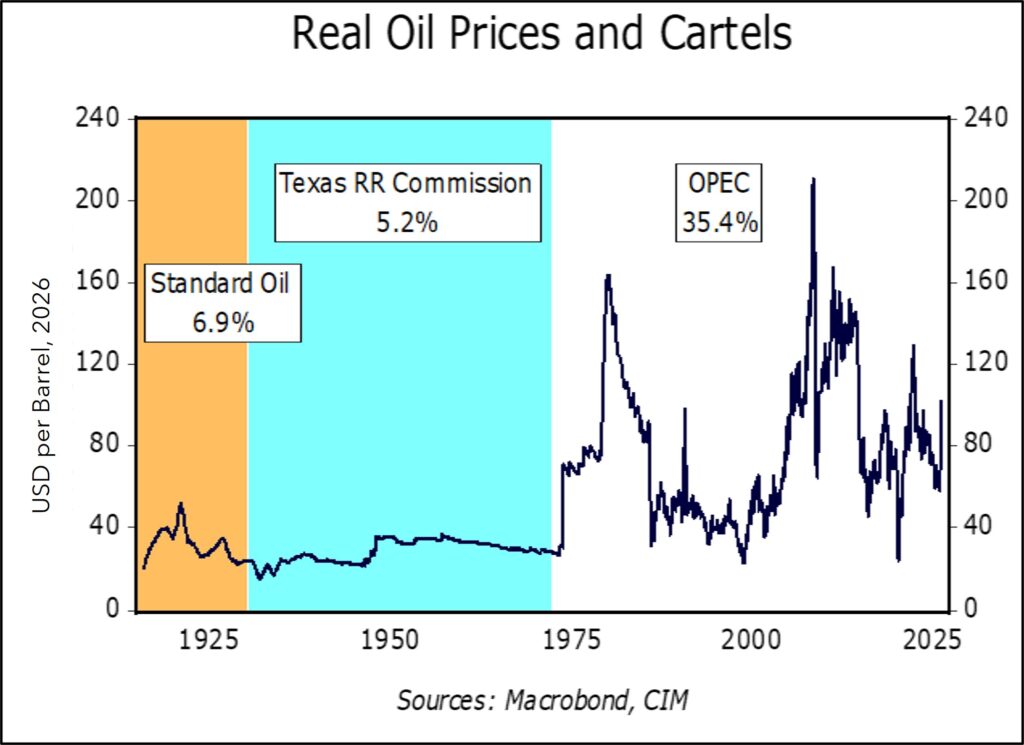

Just what sort and how much of an impact is the focus of this report. To understand why the UAE’s action is important, it’s worth examining the role of cartels in the oil market. Oil supply has a tendency to be “lumpy.” On occasion, large oil fields are discovered and developed. Once these fields begin producing, supply usually increases dramatically. Oil demand is price inelastic, which means that in the short run demand doesn’t immediately react to the increase in supply. A glut of oil occurs, which brings sharply lower prices. Usually, suppliers react to the drop in price by reducing output. However, oil fields have limited flexibility in boosting or cutting output as oftentimes it can be very costly to reopen a well once it has been shut in. Oil is also unique compared to other commodities in that there is an incentive to continue producing once a well is operational because, if a producer were to stop, there would be nothing to prevent other drillers from pulling oil from the same field.[1]

This situation can lead to collapsing prices. When the East Texas Oil Field was discovered during the Great Depression, production soared and caused prices to fall from $1.10 per barrel to $0.15 per barrel. Not only can such a glut be ruinous for producers, but the rush to generate cash flow can lead to overproduction and damaged reservoirs. In this example, the Texas Railroad Commission, which had authority to regulate oil production in the state, used the state militia to enforce production shares. The commission became the de facto cartel manager of the oil market, holding production off the market to keep the price higher than a free market would have generated, while also helping to stabilize prices. The Texas Railroad Commission held this role until 1972, when US consumption matched the state’s production capacity. From this point forward, OPEC became the cartel that manages the oil price.

These reports were prepared by Confluence Investment Management LLC and reflect the current opinion of the authors. Opinions expressed are current as of the date shown and are based upon sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change. This is not a solicitation or an offer to buy or sell any security. Past performance is no guarantee of future results. Information provided in this report is for educational and illustrative purposes only and should not be construed as individualized investment advice or a recommendation. Investments or strategies discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances.