By Chris Konstantinos, CFA

SUMMARY

- The US has hiked tariff rates to their highest level in over a century.

- We believe this risks a global trade war, with negative implications for both inflation and growth.

- Ideology over pragmatism makes resolution unlikely in the near-term.

- In the absence of a policy course correction, we see further downside in stocks.

Last week, just ahead of April 2’s widespread tariff announcements due from the White House, we wrote the following:

“The credible threat of tariffs – especially directed at serial trade abusers such as China – can be an effective bargaining chip to force unfair actors to level the playing field. However, if applied too broadly and rolled out in a haphazard fashion, tariff policy can become the ultimate ‘cut off your nose to spite your face’ scenario. We view a trade war marked by escalating ‘tit for tat’ retaliatory tariffs as ultimately a tax that US consumers and businesses will be forced to bear.”

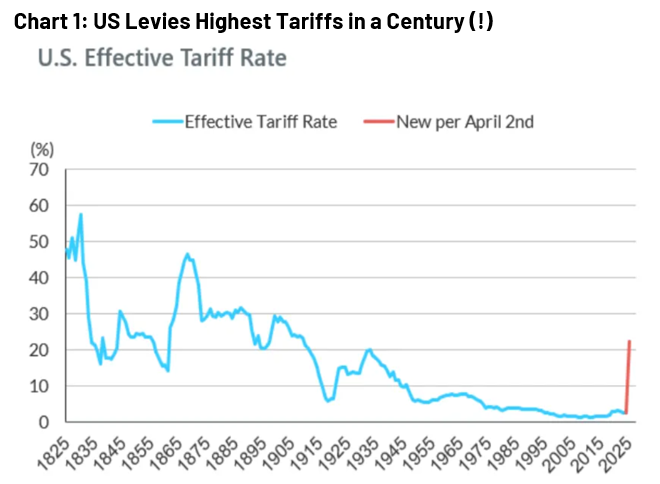

Unfortunately, April 2’s announcements were much ‘broader’ and more ‘haphazard’ than we expected, both in depth and breadth of tariffs… meaningfully increasing the probability of a global trade war, in our view. The announcement set a ‘baseline’ tariff at 10% for the entire world, but many countries – including most of the US’ largest trading partners in Europe and Asia- will be subject to much higher tariffs seemingly based on a simple calculation of a country’s relative net trade position to the US, rather than on relative tariff levels. As such, the US’ effective global tariff rate, which prior to the announcement was among the lowest in the world, will now skyrocket to its’ highest in more than a century if fully implemented as proposed (See Chart 1 below, reprinted from a 4/3/25 Bloomberg article).

We believe this outcome reflects not a ‘let’s make a deal’ negotiating tactic, as we hoped, but rather the possibility of an ideological stance that any trade deficit with another country is unacceptable. This ideology rejects the widely held view that, regardless of relative trade surplus or deficit, both parties in a free trade agreement can benefit from the opportunity cost associated with ‘comparative advantage.’ In doing so, the Trump Administration’s announcement differentiated little between economic ‘friends’ and ‘foes’. For instance, America’s allies in Asia, such as Japan, Vietnam, Taiwan, and India – all important to US technology design and manufacturing supply chains– were treated similarly as harshly as adversary China – and we believe that this approach is clarifying the strategy of the administration.

Trumponomics 2.0 Strategy Becomes Clearer – the Problem with ‘USolationism’

The news of the last week has given us a clearer sense of Trumponomics 2.0’s ambitious, even revolutionary playbook: a combination of 1880s-style isolationism (what we call ‘USolationism’), an attempt at deficit reduction (via targeted government expense reductions and tariff revenue), plus wide-ranging tax cuts and deregulation. These final stimulative measures are to help compensate low earners and corporations for any economic hardship caused by these policies’ forced reshoring of industries and jobs, and to spur investment in domestic manufacturing.

Ambitious though it may be, this strategy is problematic for US stocks in the near term for a number of reasons. First, many investors (us included) are skeptical that a global trade war will generate more US revenue than it destroys. Furthermore, raising prices and then offsetting them by giving money to consumers is one of the factors that exacerbated the recurring inflation of the 1970s, in our view.

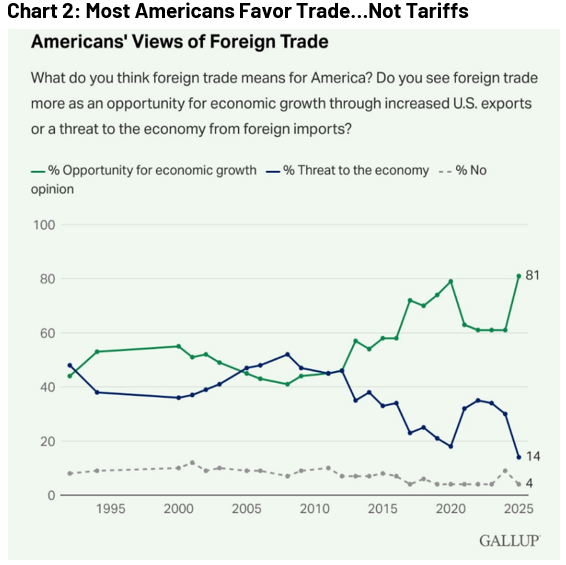

Another problem is that in Trump’s first few days in office, investors have only witnessed restrictive, market-unfriendly policy, with little meaningful movement on market-friendlier tax cuts or deregulation. This will hopefully change over time…but it is not a given that the administration has the sway in Congress to meet these campaign promises. Any blowback from his tariff announcement might prevent some of these stimulative measures from taking shape – after all, past tariff policies led to losses of majorities in the McKinley and Hoover administrations. We will be watching closely to see if public polling starts suffering alongside the stock market. A major loss of popular support is possible; according to a recent Gallup poll posted on X, 81% of Americans tend to view foreign trade positively as an opportunity for economic growth, not as a threat (see Chart 2, above).

A third problem is thus far, Trump 2.0 seems primarily interested in lowering interest rates and oil prices to offset inflation. For now, the Administration appears to be accepting stock market weakness as short-term ‘collateral damage’ weighed against their long-term ambitions.

Last, because a global trade war is likely to be inflationary, as Fed chair Jay Powell said on Friday, the Fed is not ready to choose between growth and inflation right now. Thus, it will be harder for Fed intervention to ‘ride to the rescue’ unless employment falls apart. In other words, things will likely have to get worse in the economy – and thus for corporate earnings – before they get ‘better’ as it relates to monetary stimulus. All these factors work against uncertainty clearing up soon, and thus lowers the probability of a quick stock market rebound.

Hoping for Negotiations…But Little Hope for Near-Term Resolution

It will likely be a matter of days or weeks before any sort of comprehensive response can be expected from Europe, Asia, and the rest of the world. However, the probability of ‘tit for tat’ retaliation – the early stages of a full-on ‘trade war’ – are just as likely now as concessions, in our view. China was the first major economy to strike back on Friday, announcing 34% tariffs on the US. US Commerce Secretary Howard Lutnick was quoted in Bloomberg as saying President Trump is open to negotiation but added that deals are possible “only if these countries can change everything about themselves, which I doubt they will.”

This statement from one of Trump’s highest ranking trade czars suggests a high bar for any negotiation breakthroughs. Thus, there is little hope in our mind of immediate resolution, because simply reducing tariffs on American goods would not settle the grievances in trade outlined in the announcement. Instead, if this plays out as proposed, the US is essentially turning its back on decades of free trade and becoming more of an ‘economic island’ unto itself. While it is possible that this is part of a longer-term negotiation, we recognize that the negotiation will now require time, and this time will come at a cost to investors and in levels of economic activity.

While trade barriers may eventually result in more manufacturing ‘reshoring’ back to the US over the long-run, in the short-to-intermediate term the result is likely detrimental for US economic growth simply due to uncertainty. Unfortunately, it also likely places additional upward pressure on inflation due to the higher cost of US production, unless a recession does take hold. It also exacerbates downward pressure on the US dollar, especially if the Fed has to step in and lower rates, something they have declined to do thus far. While we remain steadfast in our belief in American ‘Economic Exceptionalism’ long-term, the short-term challenges will likely require cost cutting and thus rising unemployment.

What Now? An Investor Risk Management Playbook for a Global Trade War

Last week, we laid out our view that ill-conceived tariff policy can affect the US economy – and thus stocks – via three distinct channels: inflation, economic growth, and access to capital. The news from April 2 is forcing us to have to reevaluate our stance on all three channels … and thus our overarching market view. Recent drops in interest rates suggest the market believes that the biggest impact will be felt in the economy, increasing the probability that the US falls into recession in ’25/26. Lower economic growth combined with stubborn inflation would cause our view to trend more closely to our ‘Inflationary Bear Scare’ scenario for US stocks that we laid out in our 2025 Outlook. This suggests to us further potential downside in markets even after this past week’s sell-off.

Investor sentiment – which was pessimistic even before April 2, as we have previously discussed– is now likely to hit historic extremes in pessimism in the aftermath of this announcement. Our research suggests this condition generally represents good entry points for longer-term investors. However, given the level of uncertainty, it is important to understand that the ‘condition’ of extreme pessimism does not necessarily represent a near-term ‘catalyst’ for a lasting market rebound, especially now with meaningful technical damage inflicted (see below for more on this). This suggests that tactical asset allocators may desire to reduce US equity exposure, even if their longer-term views remain constructive. The fluid situation calls for investor humility and flexibility, as we discussed last week.

Importantly, we would strongly recommend any tactical investor engaging in risk management also concurrently formulate a plan for ‘getting back in’ to stocks as well. As we stated in our Outlook, corporate America is unbelievably adept at quickly adjusting to unexpected macro impacts. We suspect that corporate managers will be quick to respond …which may mean corporate profits in certain sectors may be protected at the expense of job creation.

Technical View: US Stocks Definitively Break Bottom End of ‘Decision Box’

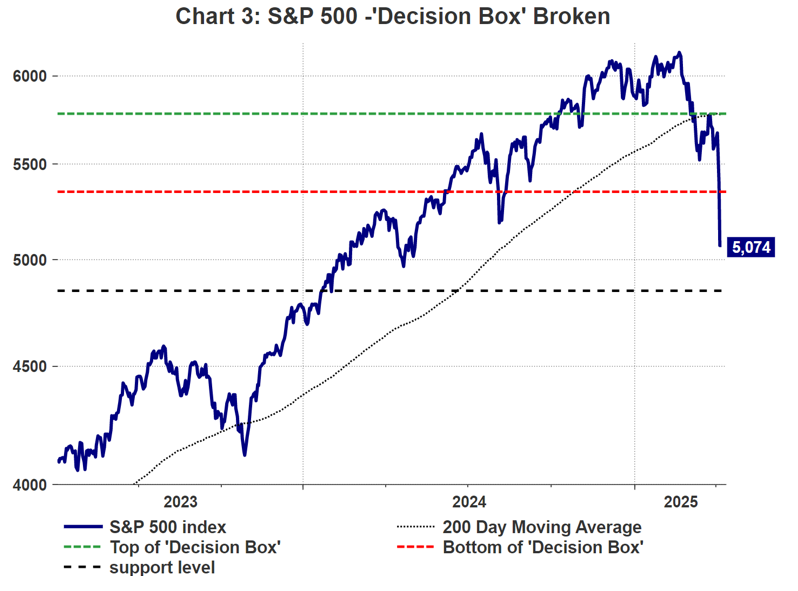

Technically, as we mentioned last week we were monitoring the lower end of our ‘decision box’ at 5350. Unfortunately, Friday’s price action has definitively breached the bottom of the box (see Chart 2, above), a warning signal to us to expect further weakness in the near term and a more prolonged bottoming process. When markets fall this quickly, counter trend rallies can be significant amid high levels of volatility. For any such rally, we now expect 5350 to be an important resistance level. A meaningful break above 5350 could be a signal that the market is healing. Next levels of potential market support exist in our view at 4850, the 50% retracement of the bull market beginning in October 2023.

Opportunities Amid the Rubble: Tech, Alternative Yield Strategies Look Attractive to Us

Source: LSEG Datastream, RiverFront; data daily as of April 7, 2025. Shown for illustrative purposes only. Past performance is not indicative of future results.

Technology stocks could continue to suffer in the near term, as they are highly liquid and comprise the biggest part of most US portfolios… and therefore remain in the crosshairs in an indiscriminate selloff like what we have seen over the last few days. However, a global trade war and reshoring could support tech spending cycles -particularly on automation and other productivity-enhancing tech – likely at the expense of hiring personnel. We also think highly profitable tech could potentially be seen as a bit of a ‘safe haven’ asset– both because they have “fortresses” of cash and “wide moats” of high profitability.

We think alternative yield strategies that use derivatives to generate higher yield from stocks may also be a useful strategy in an uncertain environment where volatility is likely to remain high. We would note these strategies gained popularity in the stagflationary 1970s…a playbook worth dusting off, in our view.

If the dollar continues to weaken, there’s potential for international stock returns to continue to look attractive on a relative basis to US-domiciled investors…particularly as valuations are lower there than in the US. We are intrigued… but not convinced that the ‘new world trade order’ will be beneficial to European and emerging market economies or corporate earnings, and would not suggest investors get overly optimistic on the ‘international trade’ before definitive signs of improved relative earnings become apparent.

Conclusion: US ‘Economic Exceptionalism’ Not Dead…But Flexibility and Humility Called for in the Near-Term

In tough markets, it is often hard to remain unemotional and to sustain a sense of perspective. We would urge investors face the new market reality clear-eyed, but also open to the historical fact that stock markets eventually recover from turmoil, often when you least expect it– we suspect this time will be no different. A couple strongly held RiverFront views for these kinds of times:

- American ‘Economic Exceptionalism’ is NOT Dead. We believe the US’ productivity advantage is structural and ‘bigger’ than any one president or political administration. It has proven itself over the past half-century, during a lot of different political and market backdrops. What is lost in the current market turmoil is our belief that the US is still an island nation that is rich in natural resources and the best run, most profitable companies in the world. We believe the US is the best place in the world to start a company and to innovate, with deep commitment to R&D spending and IP protection. Corporate America is among the best in the world at adapting to unexpected conditions…we believe the resiliency of the US economy in 2020 and 2022 aptly demonstrates this.

- Markets typically bottom long before economic news gets better. Our guess is that policymaker stimulus will be the turning point, just as it was in 2020 and 2008. We will stay vigilant in monitoring signs that either fiscal or monetary stimulus – or both- may mark the turning point of this downdraft.

- In great turmoil, there are opportunities if you are willing to take a longer-term view. See our ‘Opportunities Amid the Rubble’ section above.

- Last, US political history suggests that unpopular or controversial policy rarely survives long-term. For more on this subject, see our Weekly View from 2/11/25.

Originally published on RiverFront Investment Group.

For more news, information, and strategy, visit the ETF Strategist Channel.

Risk Discussion:

All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

The comments above are subject to change and are not intended as investment recommendations. There is no representation that an investor will or is likely to achieve positive returns, avoid losses or experience returns as discussed for various market classes.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

All charts shown for illustrative purposes only. Technical analysis is based on the study of historical price movements and past trend patterns. There are no assurances that movements or trends can or will be duplicated in the future.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

In general, the bond market is volatile, and fixed income securities carry interest rate risk. (As interest rates rise, bond prices usually fall, and vice versa). This effect is usually more pronounced for longer-term securities). Fixed income securities also carry inflation risk, liquidity risk, call risk and credit and default risks for both issuers and counterparties. Lower-quality fixed income securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer. Foreign investments involve greater risks than U.S. investments, and can decline significantly in response to adverse issuer, political, regulatory, market, and economic risks. Any fixed-income security sold or redeemed prior to maturity may be subject to loss.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below.

Changes in the value of foreign currencies compared to the U.S. dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the U.S. dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the U.S. and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-U.S. securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Alternative equities include non-traditional equity strategies such as hedged or income enhanced strategies through the use of derivatives. Alternative investment strategies typically carry a higher risk of loss. Hedged products do not insulate a portfolio against losses and there is no guarantee that income enhanced strategies will provide the expected income.

Technology and internet-related stocks, especially of smaller, less-seasoned companies, tend to be more volatile than the overall market.

Index Definitions:

Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

Definitions:

A trade war is an economic dispute between two countries. It can occur when one country retaliates against another’s perceived unfair trading practices with restrictions, such as tariffs, on imports.

Inflation is a gradual loss of purchasing power, reflected in a broad rise in prices for goods and services over time.

Stagflation is an economic cycle characterized by slow growth and a high unemployment rate accompanied by inflation. Economic policymakers find this combination particularly difficult to handle, as attempting to correct one of the factors can exacerbate another.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at riverfrontig.com and the Form ADV, Part 2A. Copyright ©2025 RiverFront Investment Group. All Rights Reserved. ID 4384382