There have been two times in my career when speculation ran rampant, markets got frothy, and financial bubbles formed. One was the Tech Bubble and the other was the Housing Bubble. The current environment seems very much the same as those two periods, if not bigger.

That may sound like a warning but for long-term investors it’s actually a reason to be optimistic. Just as past bubbles ultimately gave way to powerful investment opportunities, we believe this one will too.

For every action, there is an equal and opposite reaction. Speculators’ extreme risk taking morphed into extreme conservatism after the bubbles deflated as surprisingly large losses spurred equally disproportionate fear.

One can never convince speculators that they are being imprudent during a bubble. After all, recklessness, not rationality and not sound fundamental analysis, is the life blood of such frothy periods. The point of this report is not to change short-term traders’ minds, but rather to merely show evidence that speculation is running rampant, and how that presents huge opportunities for more patient investors.

10 signs of extreme speculation/bubble:

-

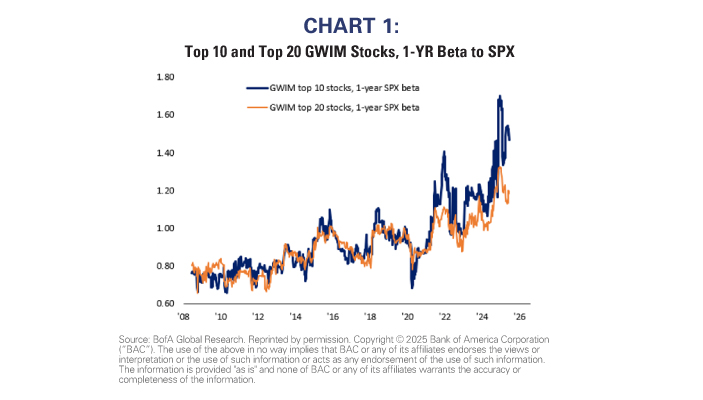

We have pointed out many times that private client equity beta is at all-times highs. As of the end of June, private clients’ equity beta was 1.5 for the top 10 holdings and 1.2 for the top 20 holdings. Both remain near the record levels of a few months ago.

2. Fund managers’ risk appetite has increased by the most in history during the last 3 months[1].

3. As of July 28th, 35% of average daily volume is now in stocks with prices less than $5[2].

4. Cryptocurrencies and meme coins continue to attract disproportionate capital despite that most will never have any economic purpose.

5. An increasing number of companies are abandoning their basic business models to hoard cryptocurrencies (they prefer to be called cryptocurrency “reserves”). It has become acceptable to borrow to facilitate hoarding.

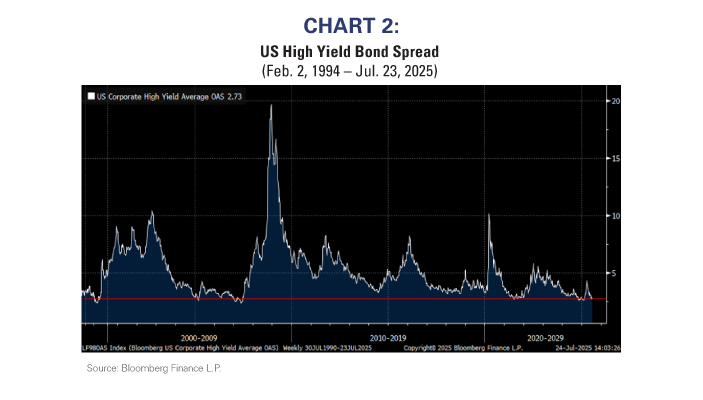

6. Credit spreads remain close to 20-year lows despite that the profits cycle appears poised to decelerate. The only time spreads were this narrow was prior to the Great Financial Crisis.

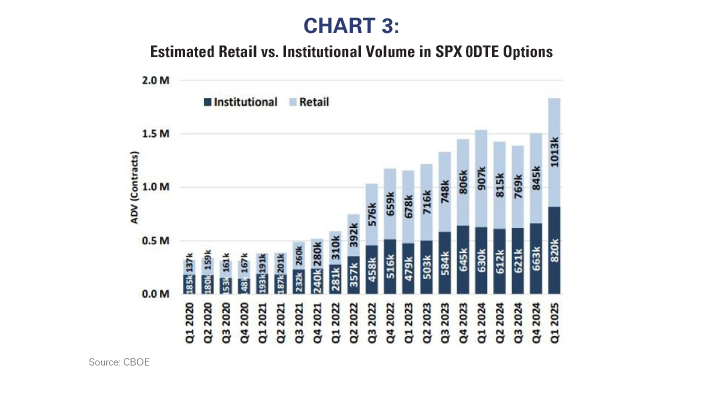

7. Individual investors’ use of zero-day options is at all-time highs and about 75% of levered ETFs market capitalization is held by individual investors[3].

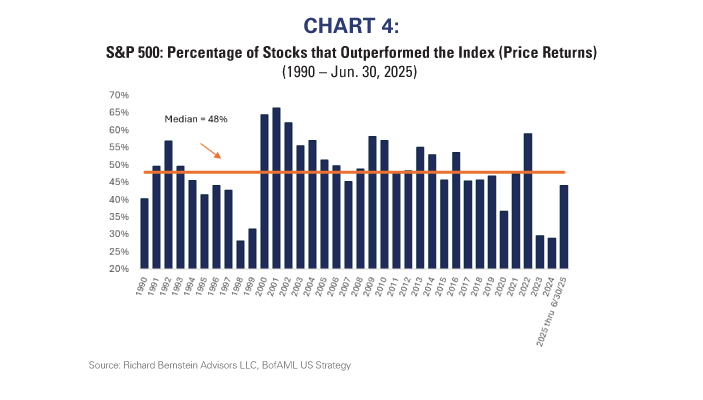

8. Narrow breadth is back in vogue. Goldman Sachs pointed out 2024 was the narrowest year in the US stock market since the Great Depression. Narrow leadership makes economic sense during a depression because companies are trying to survive let alone grow, and the few companies that can indeed grow lead the stock market. US economic growth has been healthy over the past several years, so the extraordinarily narrow leadership likely reflects speculation rather than historically weak fundamentals.

9. 70% of long-only fund managers now own 6 of the Magnificent 7 stocks, which represents an all- time high[4].

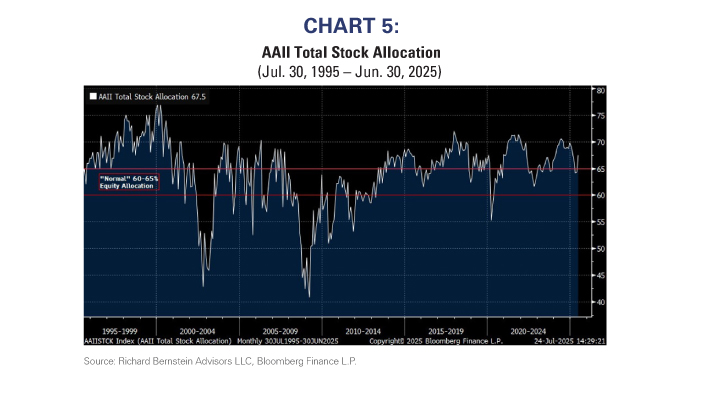

10. Although not extreme, individual investors’ stock allocations are above what is considered a “normal” allocation. History suggests some of the best times to overweight equities is when their allocations are well below normal. (Source: AAII)

What deflates the bubble?

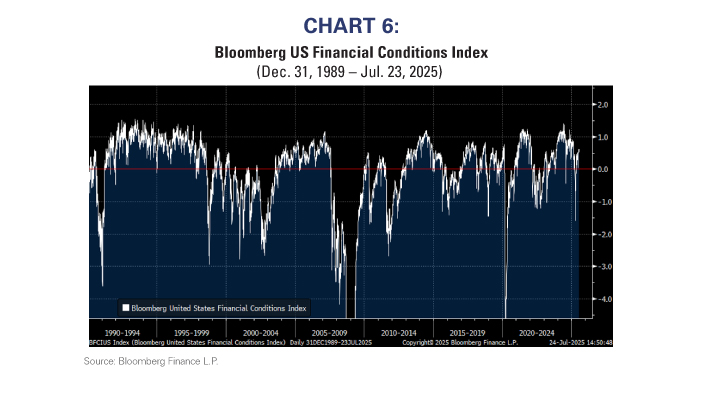

Bubbles often end when financial conditions tighten, economic growth slows, and liquidity flows from speculation to necessities. Instead of day-trading, households are forced to use their cash flow to pay their mortgages, buy groceries, and buy gasoline for their cars.

Financial conditions currently remain generous. However, if inflation proves more stubborn or growth slows more than is current consensus, history suggests that financial conditions could quickly change, and speculation accordingly stop.

Although seemingly forgotten, 2022’s stock market faced significant headwinds when the Fed was forced to tighten because of unanticipated inflation, and March 2025’s tariff-related inflation fears quickly tightened financial conditions and sent speculators scurrying.

Popular sectors, like Technology, Consumer Discretionary, and Communication Services were down between 25% and 40% during 2022, and they were all down more than 8% in a single month during March 2025.

So, it’s not a bad guess that any tightening of financial conditions, whether it is the Fed responding to higher inflation or growth slowing more than is expected, might cause speculation to reverse.

Investors versus speculators

This is not a bearish report. We believe investors are being presented with tremendous opportunities that are being overlooked by speculative, shorter-term traders. Opportunities, in sectors like dividend-paying stocks and non-US quality, present tremendous investment potential and currently dominate our portfolios.

Speculators should be wary, but investors should be licking their chops.

Originally published July 30, 2025

For more news, information, and strategy, visit the ETF Strategist Content Hub.

Mag 7: The Bloomberg Magnificent 7 Total Return Index. The Bloomberg Magnificent 7 Total Return Index is an equal-dollar weighted equity benchmark consisting of a fixed basket of 7 widely-traded companies classified in the United States and representing the Communications, Consumer Discretionary and Technology sectors as defined by Bloomberg Industry Classification System (BICS). These consist of AAPL, AMZN, GOOGL, META, MSFT, NVDA and TSLA. International Quality: The MSCI World Ex USA Sector Neutral Quality Index. The MSCI World Ex USA Sector Neutral Quality Index measures the performance of international developed large and mid capitalization stocks exhibiting relatively higher quality characteristics as identified through the fundamental variables: ROE, earnings variability & debt-to-equity. US Stable Dividend Growth: The S&P High Yield Dividend Aristocrats Index. The index measures the performance of the highest dividend yielding S&P Composite 1500 Index constituents that have followed a managed-dividends policy consistently increasing dividends every year for at least 20 consecutive years. S&P 500®: The S&P 500® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US market. The index includes 500 leading companies covering approximately 80% of available market capitalization. Sectors: S&P 500® sectors in accordance with the Global Industry Classification Standard (GICS®) developed by MSCI Barra and Standard & Poor’s.

About Richard Bernstein Advisors

Richard Bernstein Advisors LLC is an investment manager focusing on long-only, global equity and asset allocation investment strategies. RBA runs ETF asset allocation SMA portfolios at leading wirehouses, independent broker/dealers, TAMPS and on select RIA platforms.

Additionally, RBA partners with several firms including Eaton Vance Corporation and First Trust Portfolios LP, and currently has $16.6 billion collectively under management and advisement as of June 30, 2025. RBA acts as sub‐advisor for the Eaton Vance RBA Equity

Strategy Fund, the Eaton Vance RBA All‐Asset Strategy Fund and also offers income and unique theme‐oriented unit trusts through First Trust. RBA is also the index provider for the First Trust RBA American Industrial Renaissance® ETF. RBA’s investment insights as well as further information about the firm and products can be found at www. RBAdvisors.com.

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery

to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. RBA information may include statements concerning financial market trends and/or individual stocks, and are based on current market conditions, which will fluctuate and may be superseded

by subsequent market events or for other reasons. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment which may differ materially, and should not be relied upon as such. The investment strategy and broad themes discussed herein may be inappropriate for investors depending on their specific investment objectives and financial situation. Information contained in the material has been obtained from sources believed to be reliable, but not guaranteed. You should note that the materials are provided “as is” without any express or implied warranties. Past performance is not a guarantee of future results. All investments involve a degree of risk, including the risk of loss. No part of

RBA’s materials may be reproduced in any form, or referred to in any other publication, without express written permission from RBA. Links to appearances and articles by employees of Richard Bernstein Advisors, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor’s investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment’s value. Graphs, charts,

and tables are provided for illustrative purposes only. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment’s value. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.

© Copyright 2025 Richard Bernstein Advisors LLC. All rights reserved. PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS