By Gary Stringer, Kim Escue and Chad Keller, Stringer Asset Management

As an ETF market strategist firm, we are in a constant search for specific ETF products that fill the specific needs that we identify in our Strategies. We have managed Strategies for more than a decade to target various risk levels and then use a diverse set of ETFs as building blocks. As the ETF industry has grown, the availability, depth, and breadth of products has been a wonderful evolution for the industry. Furthermore, innovation, creativity, and competition have done great things for the ETF marketplace as it has expanded the available options.

As a part of our process, we look for ETFs that have defined exposures whether those intended exposures are an asset class, region, capitalization or sector based. We also find a lot of offerings that have some level of risk management. These options often come with descriptive names like quantitative, minimum volatility, low volatility, and smart beta, just to name a few. However, names often do not tell the whole story and these types of ETFs require us to look deeper into how they are constructed to understand the composition and potential pitfalls.

It’s a good idea to analyze even plain vanilla index ETFs to avoid unintended concentrations and risks inherent to their construction. For instance, a broad market ETF that tracks the S&P 500 Index can have surprisingly heavy exposure to technology companies with its capitalization weighting in certain markets. In fact, looking at that Index today, the top five holdings, which are all technology companies, make up roughly 25% of the Index. That sector exposure may be what an investor wants or doesn’t want, but it’s critical to know that before investing.

ETFs that offer quantitative strategies beyond the basic require more attention to guard against some unintended consequences. Some of the more popular ETFs in recent years are those that are designed to limit risk by applying a risk screen to a broad index. These ETFs then allocate to those names that exhibit certain risk characteristics. Most importantly, the methodology really matters, and investors need to know how these ETFs are created.

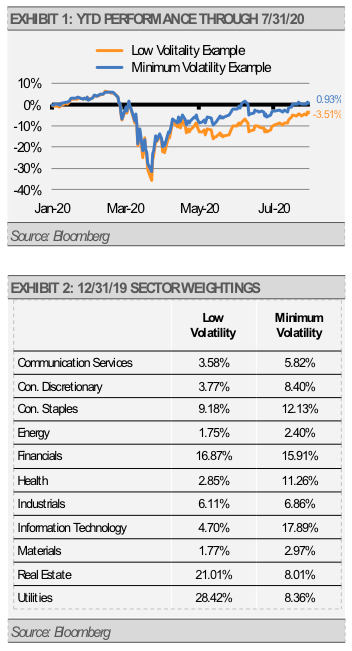

So, to answer the question, “what’s in a name?” As it turns out, naming conventions for investment products are simple descriptions and largely aspirational. Perhaps an example will help illustrate this point by looking at two domestic large cap ETFs designed for reduced volatility. Both ETFs have succeeded in generating lower volatility than the broad large cap index. One ETF defines itself as Low Volatility and the other defines itself as Minimum Volatility. Portfolio construction for both options starts with a domestic large cap index and then identifies a subset of stocks that will exhibit less risk and potentially better risk-adjusted return than the index itself. This is where all the similarities end. Unlike a basic index replication ETF, these ETFs have their own proprietary construction methodology and rebalancing schedule and it matters.

First, the low volatility ETF ranks the stocks of the S&P 500 Index by their volatility over the past 12 months and selects the least volatile 100 names each quarter. It then weights them in such a way that the least volatile stock receives the largest weighting in the portfolio and the most volatile gets the smallest weighting. In this particular ETF example, there is no consideration to how stocks in the portfolio interact with each other.

In contrast, the Minimum Volatility ETF attempts to construct the least volatile portfolio possible with stocks from the MSCI USA Index. It holds close to 200 stocks and includes both large and mid-cap names, under a set of constraints related to limiting turnover, exposure to individual names, and sector and factor tilts relative to the Index. This strategy further seeks diversification by favoring stocks with low correlations with one another. Both can be valuable tools in portfolio construction. The point here is that different methodologies have led to very different exposures, sector weightings, and results as illustrated in exhibits 1 and 2.

The key takeaway is not that one methodology is better or worse than the other. In fact, over time these two have very similar return characteristics but very different exposures and performance depending on the markets.

The key takeaway is not that one methodology is better or worse than the other. In fact, over time these two have very similar return characteristics but very different exposures and performance depending on the markets.

It’s important to recognize the ETF landscape as more than passive index investing. Understanding that a name and description is where you start before the real work. Hopefully, we were able to show that exposures from a portfolio construction standpoint can be vastly different so being familiar with the methodology is akin to knowing what you own. To take it a step further, depending on what else is owned in the portfolio, either of the above examples might provide the appropriate exposures. This means that investors need to perform some due diligence and ongoing maintenance is required and that’s a good thing. However, it has also made analysis a bit more labor intensive in that it is necessary to understand what’s under the hood and how the addition of an ETF can be effectively implemented in a portfolio to give you the results you are trying to achieve. If that’s sounds like a lot of work, consider partnering with a management team like ours.

This article was written by Gary Stringer, CIO, Kim Escue, Senior Portfolio Manager, and Chad Keller, COO and CCO at Stringer Asset Management, a participant in the ETF Strategist Channel.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant