- Astoria’s CIO, John Davi, recently attended the Delivering Alpha conference hosted by Institutional Investors and CNBC (click here). The conference featured several prominent speakers such as Leon Cooperman, Nelson Peltz, and Jim Chanos.

- It amazes us why a large portion of investors are fixated in owning growth and momentum stocks. Notable value managers such as Joel Greenblatt, Warren Buffet, Leon Cooperman, and Seth Klarman have compiled successful, long-term track records by buying stocks below their intrinsic value and selling when they become expensive (i.e. they buy low and sell high).

- Not only do momentum investors ignore the time-tested approach of these value managers, they do the opposite (they buy high with the hopes of selling higher!).[1]

- Astoria believes investors should strategically trim expensive stocks and have a more diversified portfolio both from an asset allocation and factor perspective. This involves trimming exposure to US growth stocks, US Treasuries, US corporate credit, and high yield credit. Throughout 2019, we have shifted our portfolios towards US value, US quality, and international equities. We are also utilizing alternatives such as gold, gold equities, long/short market neutral strategies, and merger arbitrage in order to further dampen our portfolio volatility.

- To be clear, we don’t believe that investors can successfully time the market or factors. We believe in allocating to a diversified portfolio of assets and factors in a low cost, tax efficient wrapper and holding for the long run.

How many ETF Strategists have produced 230 pages of investment content this summer?

- Astoria believes in being transparent with our portfolio risk characteristics (click here to read our July Investment Committee report). Some firms want to protect their “intellectual property” by saying their models or investment processes are proprietary. If we were on the other side of the table thinking about allocating to a manager, we certainly would want them to be as transparent as possible.

- We have also been very vocal about utilizing portfolio construction tools and risk models when building multi-asset portfolios (click here to read our ETF Risk Analytics report). We don’t know how many of our peers are as transparent as Astoria.

- In light of a deteriorating fundamental outlook for the global economy and earnings, we’ve strategically rebalanced our models. In this report, we present our asset allocation bands and aggregate portfolio valuations. We display our portfolios’ credit quality, interest rate risk, effective maturity, and fixed income sectors relative to their benchmarks.[2]

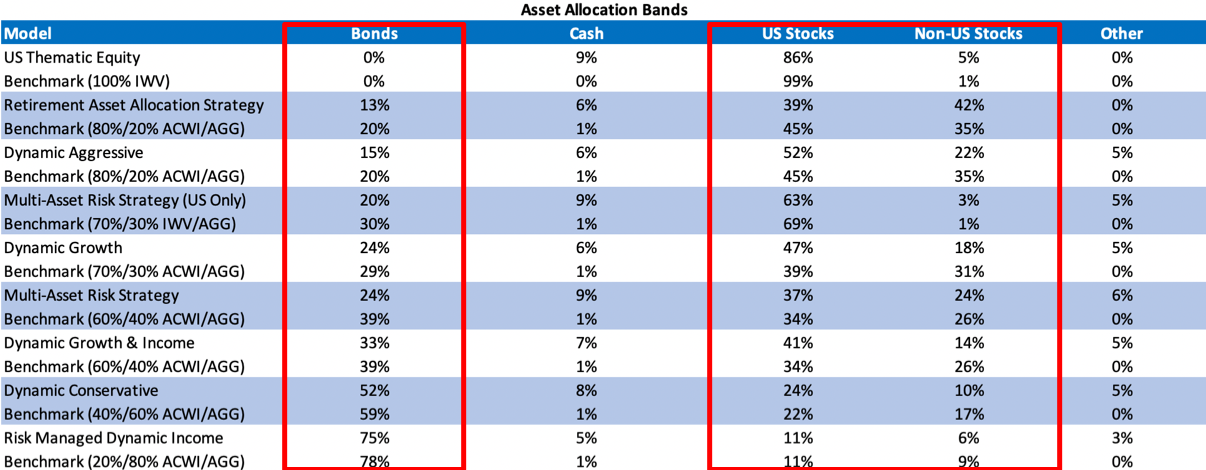

Astoria is underweight both stocks and bonds.

- Our models are underweight equities by 3-6% and underweight bonds by 5-10% relative to their benchmarks. We are utilizing alternatives to lower our portfolio volatility.

Source: Astoria Portfolio Advisors, Portfolio Visualizer, Bloomberg. ETF holdings and weights as of September 16, 2019.

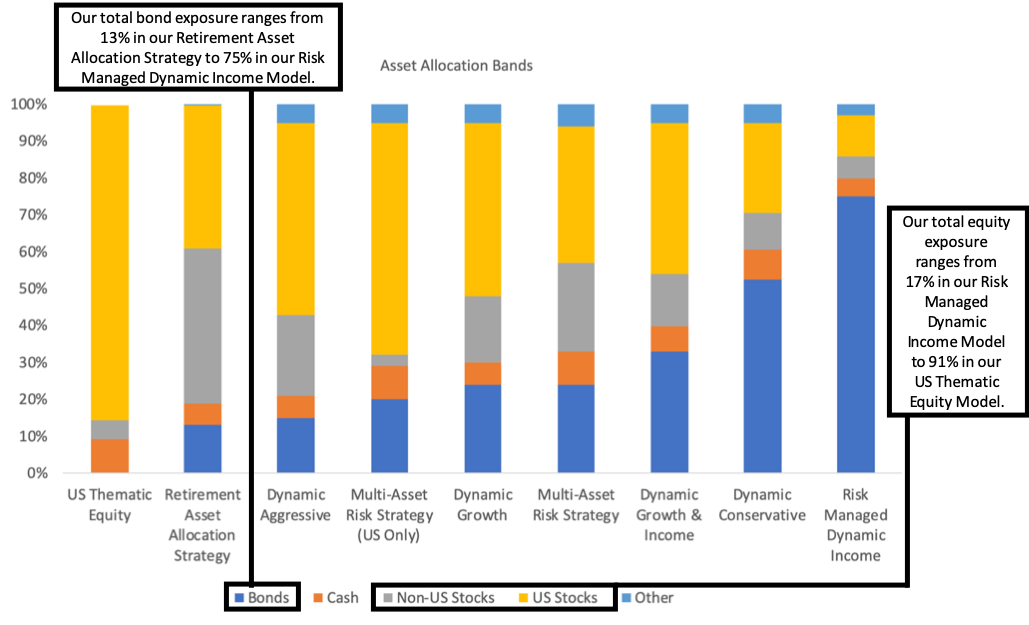

Below are our asset allocation bands in a graphical format.

Source: Astoria Portfolio Advisors, Portfolio Visualizer, Bloomberg. ETF holdings and weights as of September 16, 2019.

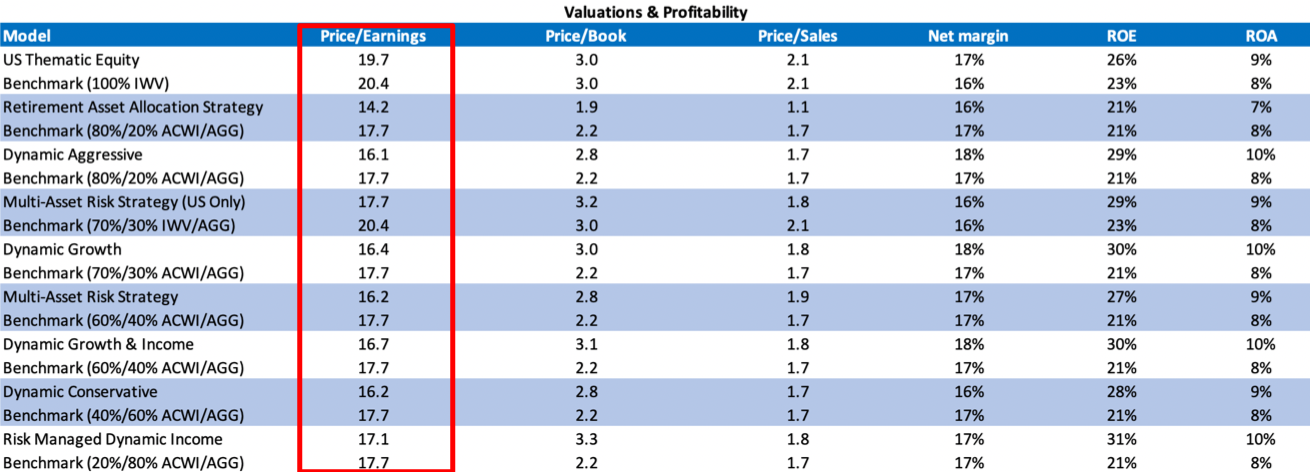

Astoria’s models are trading below their benchmarks from a PE standpoint.

- Apart from the US Thematic Equity Model (which we are mandated to hold only US equity ETFs), all our model PE ratios are cheaper than their benchmarks.

- Our US Thematic Equity Model includes significant exposure to quality stocks, explaining its high PE ratio. In a defensive market being driven by weakening fundamentals, our view is that high quality stocks will stay bid.

- We believe in allocating to international developed and emerging market equities which drives our lower valuations across all other models. We recently discussed this in a CNBC TV interview (click here).

- Investors typically suffer from a home country bias, so we continue advocate for globally diversified, cross asset portfolios. Disdain for European and Japanese banks is high, evidenced by these indices trading at 30-year lows! We believe there is enough of a margin of safety to allocate to broad-based international stocks.

- We generally have higher ROE and ROA levels compared to our benchmark given our tilt to the quality factor. We began allocating to the quality factor in Q4 2018 and further increased our exposure in Q1 2019 (click here and here to read our research on quality ETFs).

Source: Astoria Portfolio Advisors, Portfolio Visualizer, Bloomberg. ETF holdings and weights as of September 16, 2019.

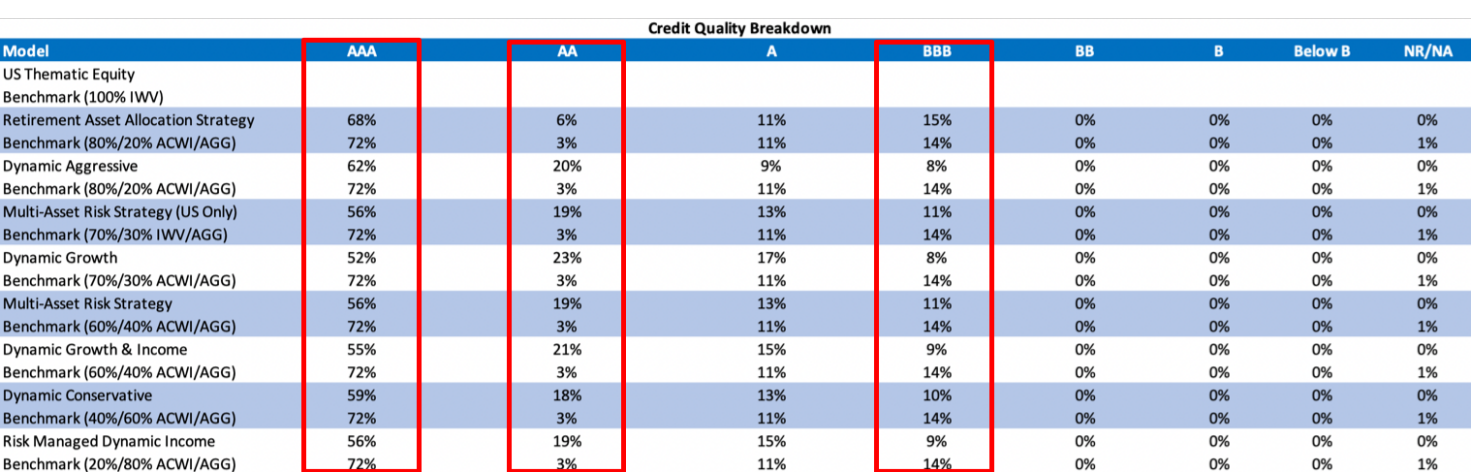

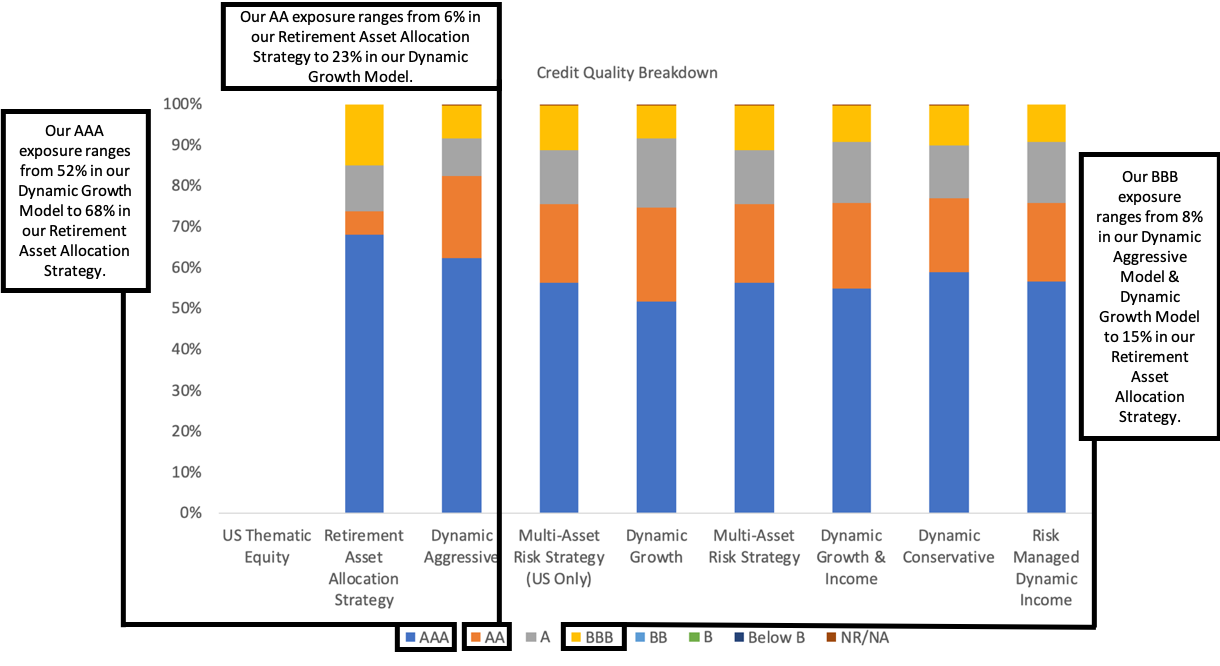

Our credit quality maintains the same bias as our equity positions – high quality.

- Relative to their benchmarks, Astoria’s models have a significant overweight to AA credits.

- We are mainly using bonds to hedge our equity risk but acknowledge that there is very little margin of safety.

- We were extreme bond bears for most of 2017 (Nov 30, 2017) and 2018 (Jan 29, 2018, Oct 9, 2018, Oct 22, 2018, & Oct 24, 2018) given poor fundamentals. We were quite concerned about liquidity declining on the margin and the impact of a rising US interest rate environment.

- Fixed income valuations aren’t overly attractive but liquidity, on the margin, is improving as Central Banks are cutting interest rates and the BOJ and ECB continue to implement their Quantitative Easing (QE) programs.

- It always amazes us how quickly markets change in a short period of time. This is the exact reason why asset allocation should be strategically rebalanced.

- We have been reducing our bond exposure throughout 2019 and envision further reductions in the future.

Source: Astoria Portfolio Advisors, Portfolio Visualizer, Bloomberg. ETF holdings and weights as of September 16, 2019.

Below are the ranges in credit quality across our models.

Source: Astoria Portfolio Advisors, Portfolio Visualizer, Bloomberg. Fundamental data as of August 31, 2019.

Buyers of negative sovereign debt might want to consider commercial property in Texas.

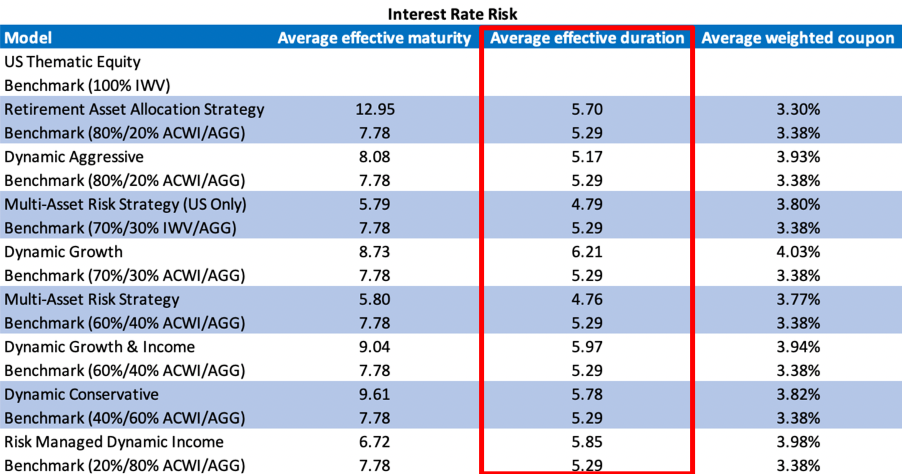

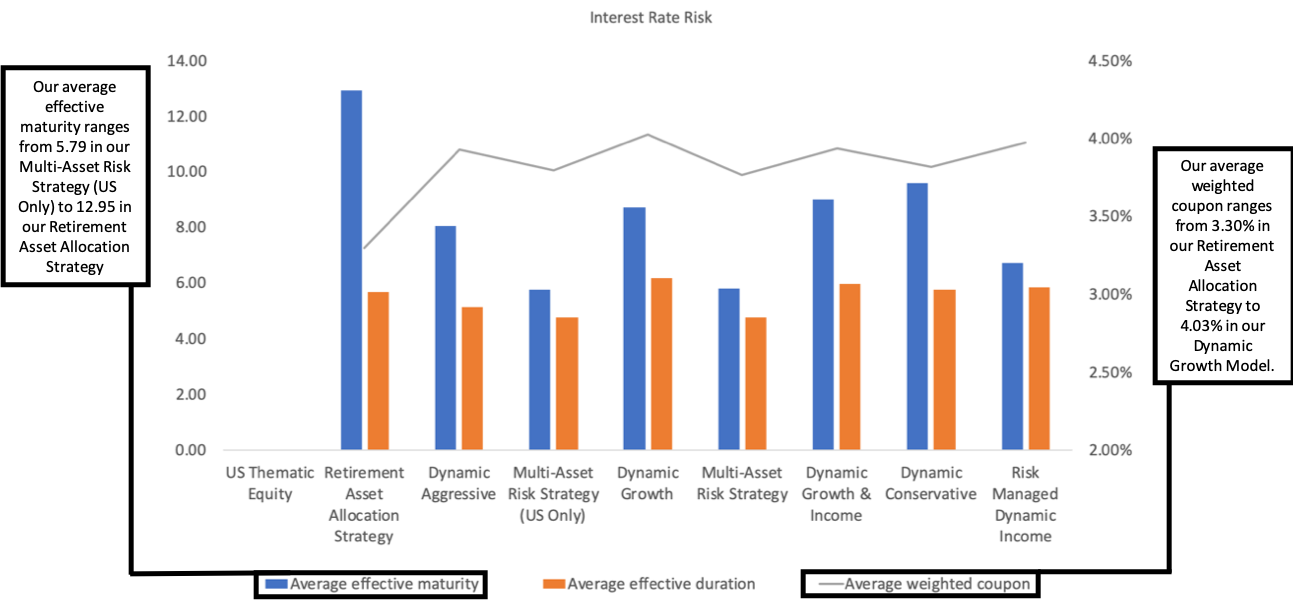

- Relative to their benchmarks, Astoria’s models are generally in line from a duration standpoint. Given the flatness (and inversion) of the yield curve, investors aren’t incentivized to go out the curve.

- We are more concerned about the impact of $15 trillion of negative sovereign debt (if you adjust for inflation, this number increases to over $25 trillion). Low levels of interest rates are punishing savers and pushing investors out the risk curve demonstrated by euphoria in the IPO market, expensive valuations in most fixed income, and private equity markets.

- Apart from US defensives and the growth cohort, stocks are still attractively priced relative to most other asset classes. In our view, this is why equities continue to rally despite their proverbial wall of worry.

- Investors holding negative yielding sovereign debt might want to consider commercial property in Texas. There are opportunities to obtain a triple net lease for a cap rate of 6-8% in a pro-business state which appears well positioned from an economic standpoint. Isn’t that a better risk/reward than paying the European government to hold your money? [3]

Source: Astoria Portfolio Advisors, Portfolio Visualizer, Bloomberg. Fundamental data as of August 31, 2019.

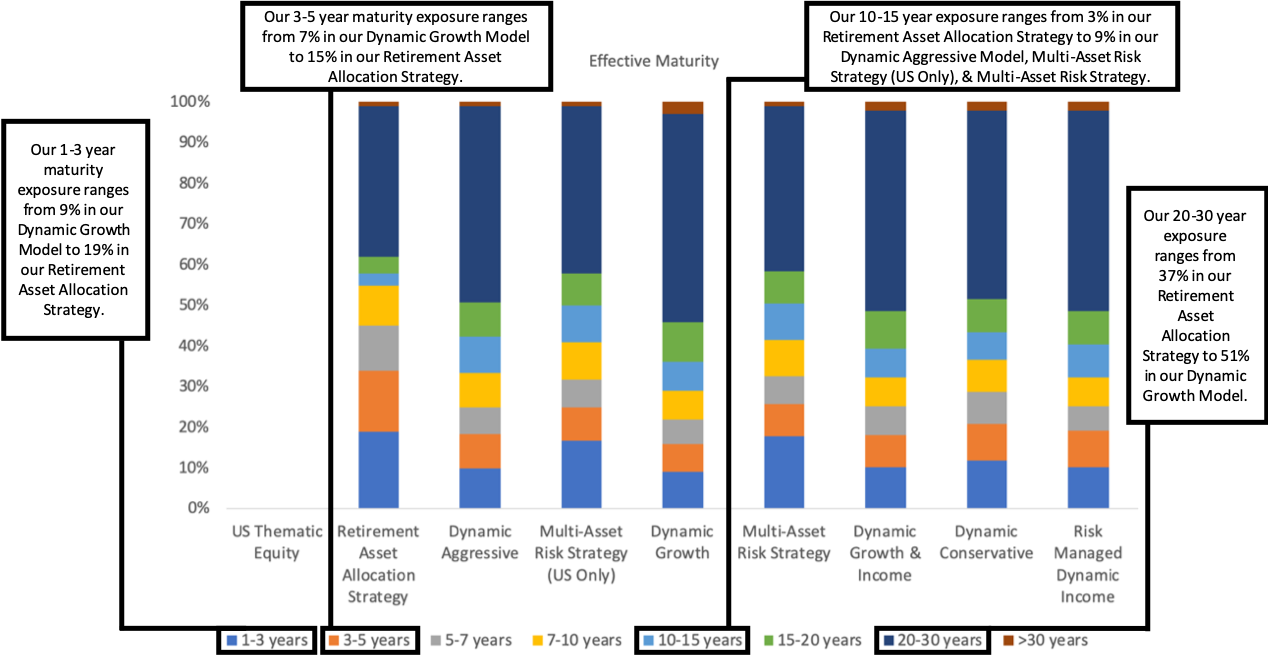

Below are the ranges in average effective maturity, average effective duration, and average weighted coupon across our models.

Source: Astoria Portfolio Advisors, Portfolio Visualizer, Bloomberg. Fundamental data as of August 31, 2019.

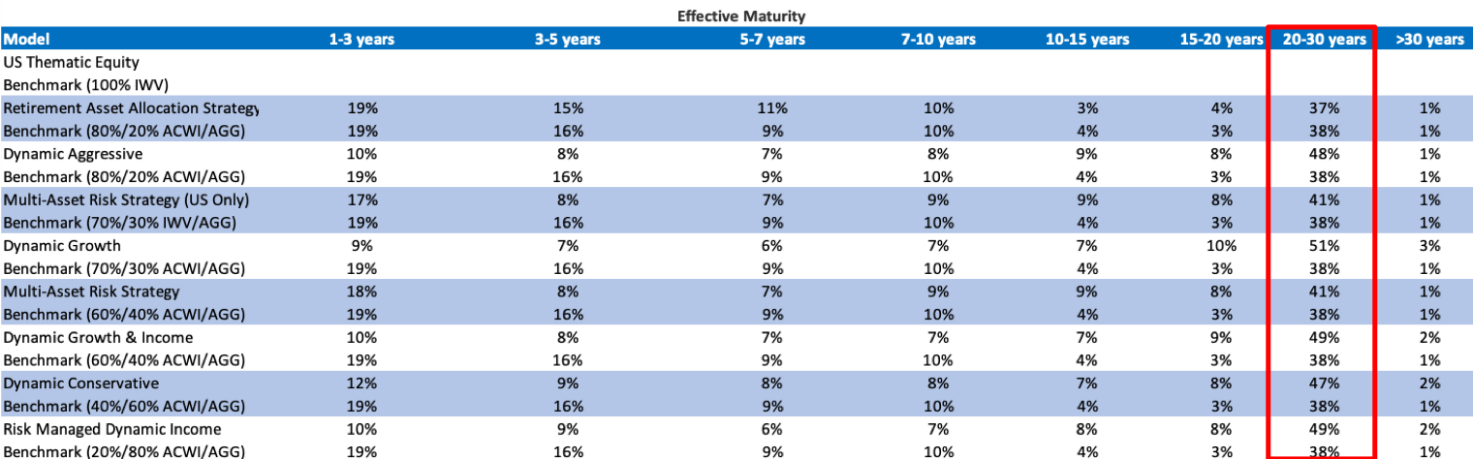

Given the flatness of the yield curve, we do not see a great risk/reward for owning long duration bonds.

- The effective maturity of our models are in-line with their benchmarks.

Source: Astoria Portfolio Advisors, Portfolio Visualizer, Bloomberg. Fundamental data as of August 31, 2019.

Below are the ranges in effective maturity across our models in graphical format.

Source: Astoria Portfolio Advisors, Portfolio Visualizer, Bloomberg. Fundamental data as of August 31, 2019.

US Treasuries are the ultimate “crash protection” hedge. However, in a “normal” market environment, they are relatively poor earnings of risk premium.

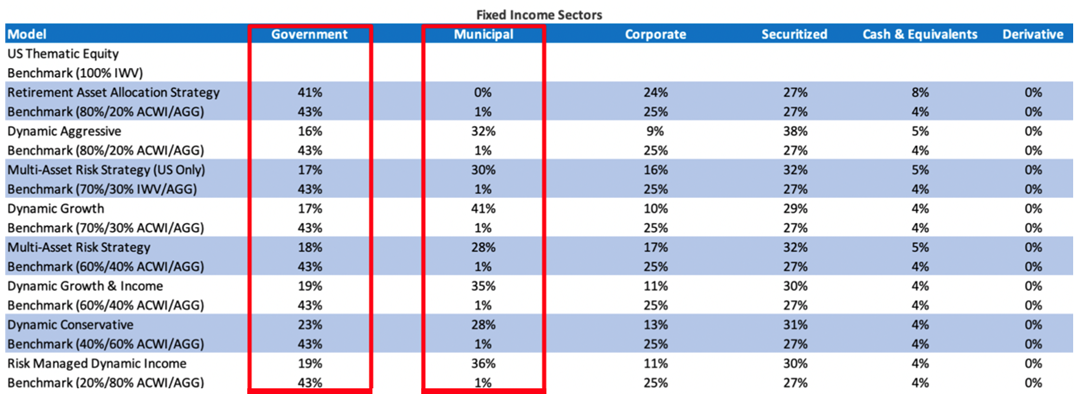

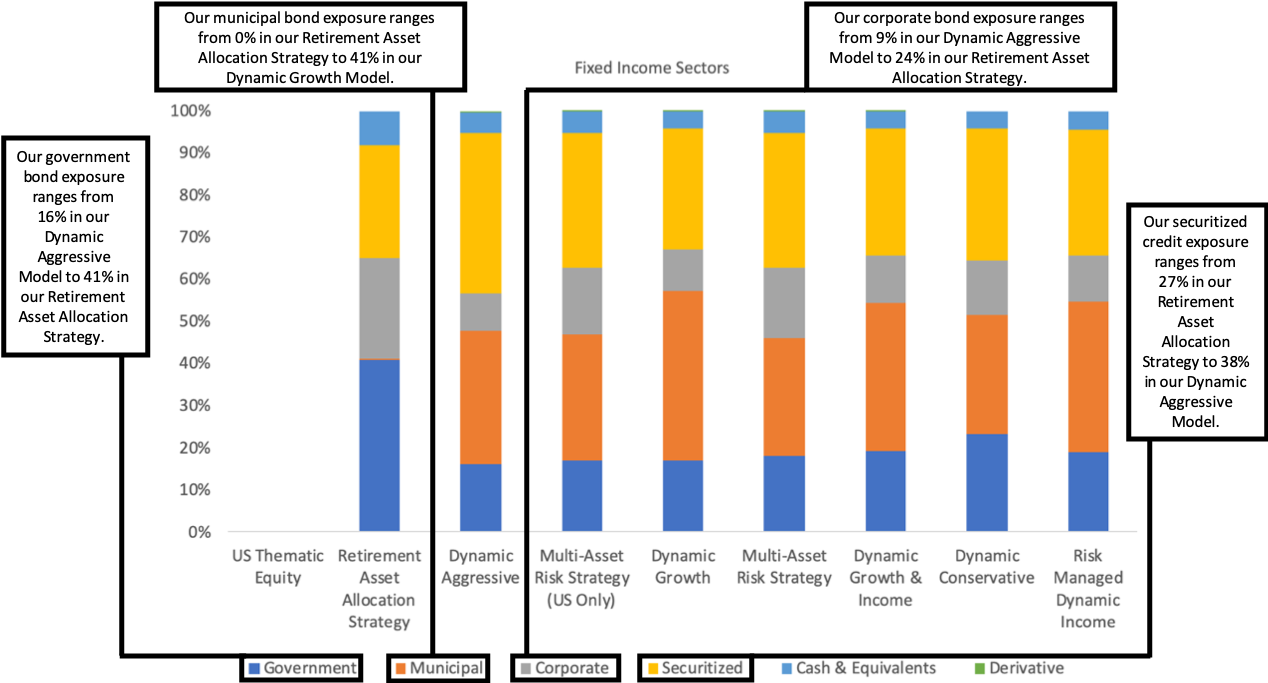

- Relative to their benchmarks, Astoria’s models are strategically overweight municipal bonds and underweight US government debt.

- There are no bargains in fixed income to say the least. With US Treasury yields hovering around all-time lows, we prefer to earn risk premium in the municipal bond market and are comfortable with the credit risk of the US.

- We prefer to own as little corporate bond risk as possible given the levels of credit spreads. We have a strategic overweight to securitized debt via our allocation to mortgage backed securities. Despite their higher durations compared to the Bloomberg Barclays US Aggregate Bond Index, we are comfortable with the AAA rated exposure of mortgage backed securities. The US housing market remains strong and the lower interest rate environment should provide a floor to the US real estate market.

Source: Astoria Portfolio Advisors, Portfolio Visualizer, Bloomberg. Fundamental data as of August 31, 2019.

Below are the ranges in fixed income sectors across our models.

Source: Astoria Portfolio Advisors, Portfolio Visualizer, Bloomberg. Fundamental data as of August 31, 2019.

Best,

Astoria Portfolio Advisors Investment Committee

To stay up to date on Astoria’s latest Investment Committee views, follow us on social media!

Facebook: https://www.facebook.com/AstoriaAdvisors/

Instagram: https://www.instagram.com/astoriaadvisors/

Twitter: https://twitter.com/astoriaadvisors

LinkedIn: https://www.linkedin.com/in/john-davi-93414510/

[1] We are obviously oversimplifying the investment process of these value managers, but the point is that they aren’t buying expensive stocks for the most part. We also acknowledge that we are generalizing the “average” investor as being fixated on momentum stocks. Some of these investors are indeed buying stocks at reasonable valuations. Also, to clarify, we aren’t opposed to momentum investing. We have utilized momentum ETFs as part of a diversified factor portfolio.

[2] Please note that these characteristics are for Astoria’s strategic Multi-Factor & Multi-Asset ETF models which we directly manage. We have a model delivery service and outsourced CIO business whereby those portfolios may have different risk tolerances and ETFs.

[3] Note that the author isn’t making a recommendation to purchase real estate and cap rates will vary depending on the actual property in Texas. Please consult with your financial advisor, tax consultant, and a lawyer before considering or purchasing real estate.

Photo Source: Pixabay.com

For full disclosure, please refer to our website: https://www.astoriaadvisors.com/disclaimer.