By Canterbury Investment Management

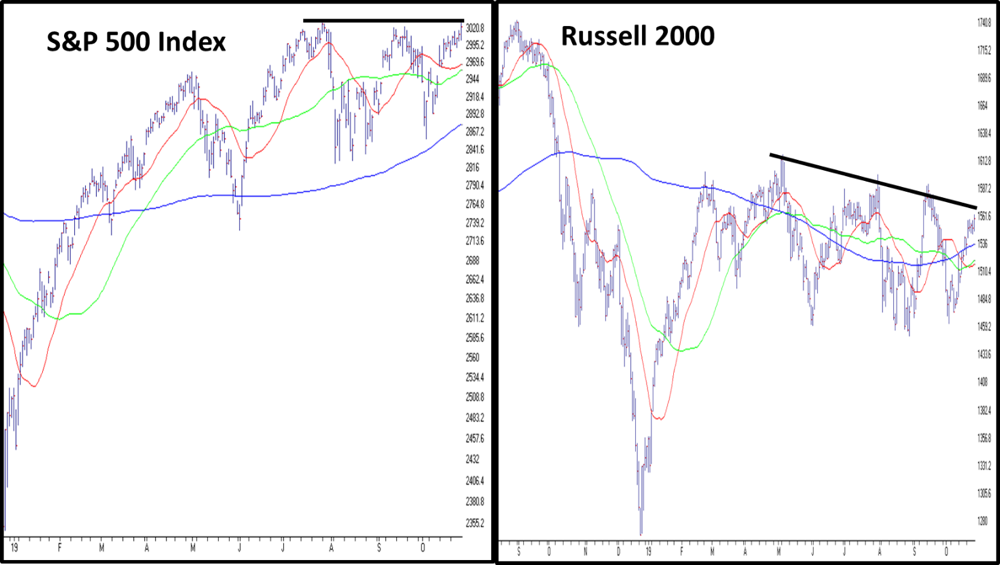

Market State 2: The S&P 500 remains in Market State 2, following a small advance in the market last week. If you turn on the news, you will be flooded with headlines telling you that the S&P 500 is at a new high. While this point might be true, the S&P 500 is still at basically the same level it was back in July.

Watch: Canterbury Weekly Update 10.29.2019

Meanwhile, the Dow Jones is not at a new high, while the Russell 2000 (small cap stocks) continues to put in lower highs. Additionally, international large caps (EAFE) and the emerging markets are far off their old highs.

Canterbury Volatility Index (CVI)- CVI 68: Volatility continues to fall slightly. In fact, short-term volatility (a 10-day CVI) is now at an extreme low level. Since July, the short-term volatility of the S&P 500 has entered an extreme low level 2 other times. Both times, we saw the market have volatility spikes, with a few negative outlier days. With the S&P 500 sitting at relatively the same spot as it was during those two other spikes, it could be expected to have another volatility spike here in the short-term future.

Comment

While the S&P 500 sits at a new high, last week’s movement was predominately driven by the weaker S&P sectors. For all of this year, the market has mainly been driven by Technology, Staples, Utilities, and Real Estate. Notice, that three out of those four sectors mentioned are typically thought to be more “conservative.” Last week’s movement was led by some of the weaker S&P sectors. In fact, the worst ranked S&P sector, both outright and on a risk-adjusted basis, has been energy. Last week, energy was the best performer and was up more than 4%.

Looking at Canterbury’s risk-adjusted rankings, Volatility-Weighted-Relative-Strength (VWRS), the bottom 5 performing sectors have been energy, discretionary, industrials, basic materials, and financials. Last week, 4 of the 5 top performers for the week were ranked in the bottom half of the risk-adjusted rankings (energy, industrials, financials, and basic materials).

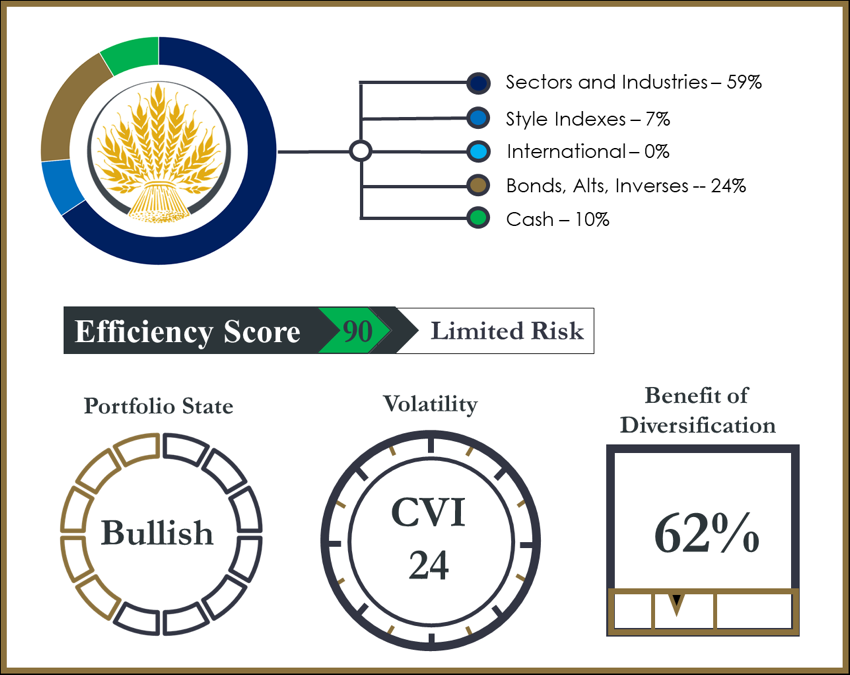

Portfolio Thermostat

The Canterbury Portfolio Thermostat does not aim to compete against any individual index or blended benchmark. We know that portfolio efficiency is a moving target, and all asset classes will go in and out of favor. The Portfolio Thermostat is an Adaptive Portfolio Strategy designed to navigate various markets and create an efficient portfolio for today’s environment- Bull or Bear.

Canterbury benchmarks its portfolio against key “internal” metrics, in order to measure portfolio efficiency. These metrics are Portfolio State, Portfolio Volatility, and Portfolio Benefit of Diversification. Together, these internal benchmarks create the Portfolio Efficiency Score.

The Portfolio Thermostat remains efficient for the current market environment. Short-term volatility has entered extreme low territory. When this occurs, outliers are more likely to happen. The Thermostat should remain stable regardless if volatility increases in the markets.

Bottom Line

While the news will talk about the S&P hitting new highs, the market was mostly driven by the bottom performing sectors last week. In addition, the Dow, Russell 2000, and many international markets have not seen the same level of success as the S&P 500. Most S&P sectors, aside from the defensive sectors that have led the market plus technology, are not at new highs. In addition, short-term volatility is in extreme low territory and we may see a volatility spike soon.

Canterbury Weekly Update 10.29.2019

This article was submitted by Canterbury Investment Management, a participant in the ETF Strategist Channel.