China’s economic ascent over the past four decades has been a remarkable story of growth driven by rapid industrialization, export expansion, and large-scale infrastructure investment. However, as the country navigates its transition from an emerging market to a global economic powerhouse, it faces two significant challenges that threaten to reshape its growth trajectory: (1) demographic shifts and (2) an escalating private sector debt burden. Understanding these factors is crucial for evaluating China’s future economic growth potential as they are likely to exert profound influence on both short-term stability and long-term sustainability.

Adding complexity to the picture, the economic consequences of the COVID-19 pandemic have underscored and amplified these existing challenges by slowing China’s growth further and intensifying the need for policy responses.

Demographic Challenges: The Aging Population

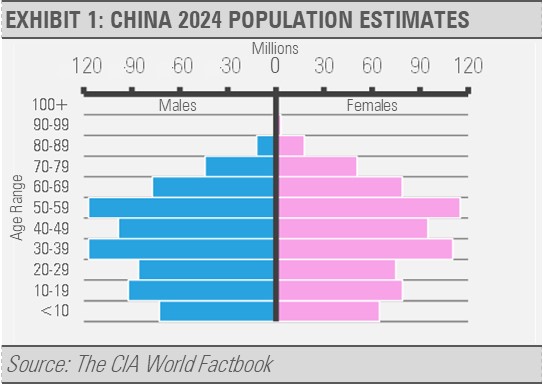

One of the most pressing demographic challenges facing China is its rapidly aging population. According to the National Bureau of Statistics, China’s fertility rate has fallen to around 1.3 children per woman, which is well below the replacement rate of 2.1, a trend that is exacerbated by the one-child policy that was in place from 1979 to 2015. As a result, the working-age population (defined as those aged 16-59) has been shrinking, while the number of elderly citizens (aged 60 and over) is growing at an alarming pace. By 2030, it is projected that one in four Chinese people will be over the age of 60.

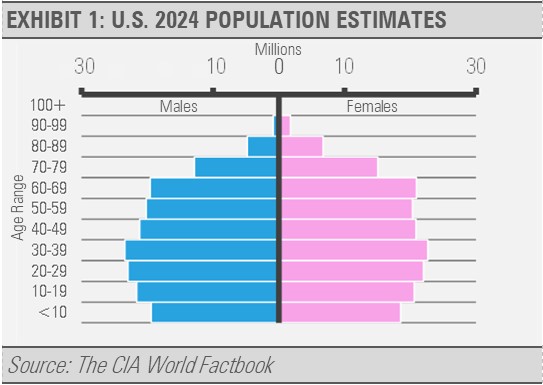

Comparing China’s demographics to the U.S. demographics below shows a stark contrast. The younger age brackets in China have shrunk significantly compared to in the U.S. where the age groups are much more stable. Worsening this issue for China is the lack of females relative to males. In fact, China has almost 29 million more males than females. That is nearly the entire population of Texas all male who may never have children or a family.

This demographic shift has several important implications for economic growth. First, a smaller workforce means lower labor force participation, which potentially leads to reduced productivity and slower economic expansion. A declining pool of young workers will also place additional pressure on wages, particularly in labor-intensive sectors, further eroding China’s competitive advantage in manufacturing. With fewer workers, the burden of supporting the elderly population through healthcare, pensions, and social services will increase significantly, putting strain on both the public and private sectors.

Moreover, an aging population often leads to lower levels of consumption, as older people tend to save more and spend less. This shift in consumption patterns can dampen domestic demand and make it harder for China to transition from an export-driven economy to one more reliant on domestic consumption. While the government has implemented policies to encourage higher fertility rates and to extend the retirement age, these measures are unlikely to provide an immediate remedy to the demographic challenges China faces.

Private Sector Debt: A Growing Burden

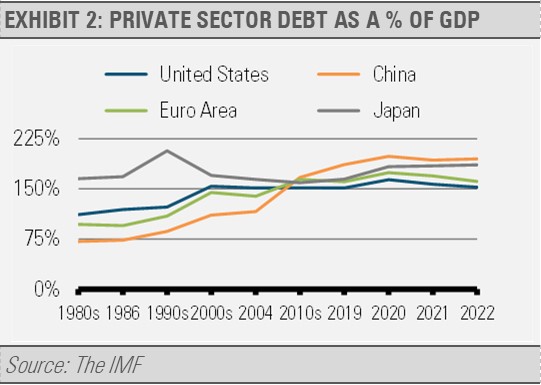

The second major challenge China faces is its growing private sector debt, which has reached alarming levels in recent years. According to the International Monetary Fund, China’s total debt (public and private) is close to 300% of GDP with the private sector accounting for a significant portion of this. Corporate debt, in particular, has ballooned in recent years as Chinese firms have increasingly relied on borrowing to fund expansion and leverage speculative investments in real estate, infrastructure, and other sectors.

China’s private sector debt has ballooned even as economic growth has stagnated. Relative to the size of their respective economies, China’s private sector is more indebted than even Japan’s private sector. Meanwhile, in the U.S and in the Eurozone, private sector debt to GDP has actually decreased since the post-COVID economic recoveries took hold.

The high levels of private debt are concerning for several reasons. First, much of this debt is concentrated in the real estate sector, which has faced a series of crises, such as the collapse of major property developers like Evergrande. The collapse of the real estate market could lead to a systemic financial crisis as property developers are unable to service their debts, which in turn impacts banks, bondholders, and other financial institutions. If the real estate sector continues to falter, it will drag down economic growth, especially since construction and real estate account for a significant portion of China’s GDP.

Second, the rising debt burden places constraints on future economic growth. As companies struggle to manage high levels of debt, they are less likely to invest in new projects or innovation, which can lead to slower productivity gains. The increasing cost of servicing debt, especially as interest rates rise, can lead to a vicious cycle where businesses and households reduce spending that further stifles growth. This scenario is particularly problematic in a context where global trade growth is slowing, and the prospects for China’s traditional growth engines, such as exports and infrastructure investment, are diminishing.

The Impact of COVID-19 on China’s Economic Growth

The COVID-19 pandemic exacerbated the challenges China already faced and further slowed economic growth, which amplified both demographic and debt-related risks. When the pandemic struck in early 2020, China’s economy was forced into a sharp contraction due to lockdowns, disrupted supply chains, and plummeting consumer demand. The economic recovery from the pandemic has been uneven with growth decelerating more than expected.

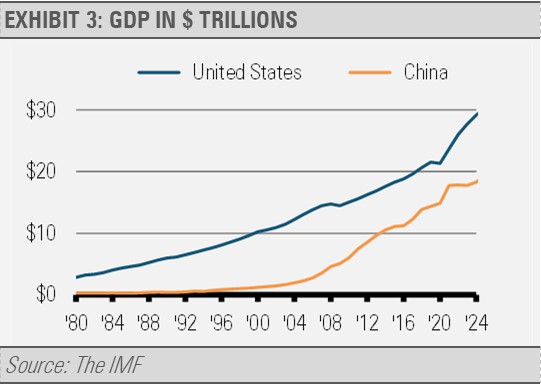

Since the pandemic, U.S. economic growth accelerated while China’s GDP growth has slowed significantly, marking a break from the blistering growth rates that characterized the previous decades.

In 2020, China managed to rebound quickly, being one of the few major economies to post positive growth, but subsequent years have seen a deceleration. In 2022, GDP growth dropped to just 3%, far below the government’s target of around 5.5%, and well under the pre-pandemic trend. While there was a recovery in 2023, growth remained below expectations with the real estate sector still in turmoil, youth unemployment rising, and consumer confidence remaining weak. The “zero-COVID” policy, while initially effective in controlling the virus, led to prolonged economic stagnation including severe disruptions to domestic consumption and production.

The pandemic underscored the vulnerability of China’s growth model, which had been heavily reliant on global supply chains, export-driven demand, and real estate investments. With the pandemic reducing both domestic and international consumption, these growth drivers were severely impacted. As the global economy slowed in response to the pandemic, China’s export sector, once a major engine of growth, found itself facing headwinds that further exacerbated the country’s economic challenges. The combination of a slowing global economy, weaker domestic consumption, and a stressed real estate sector has made it harder for China to return to pre-pandemic growth levels.

The Interaction of Demographics, Debt, and COVID

The intersection of aging demographics, private sector debt, and economic headwinds creates a particularly challenging environment for China’s future economic growth. The pandemic highlighted the structural weaknesses in China’s economy and accelerated the challenges of an aging population and growing debt burden. With a shrinking workforce and a heavier debt load, China’s growth potential has been significantly constrained. The pandemic’s lingering effects on both supply and demand further reduce the scope for a robust recovery.

Moreover, the demographic crisis, accelerated by the economic consequences of COVID, compounds these issues. With fewer working-age individuals and an aging society, there is less capacity for domestic demand-driven growth, which might have helped offset some of the negative impacts of external shocks like the pandemic. The debt crisis in real estate has also added to the economic stress, limiting both the ability of businesses to expand and the government’s fiscal flexibility to stimulate demand.

Policy Responses and Future Outlook

China’s government is acutely aware of these challenges and has introduced a series of policy measures to address them. On the demographic front, efforts to encourage higher birth rates and extend working lives are ongoing, but demographic shifts take decades to reverse, and the impact of these policies will not be immediate. China needs many more thirty-somethings, twenty-somethings, teenagers, and children. The workers of tomorrow needed to be born decades ago.

On the debt front, the Chinese government has signaled a shift toward deleveraging with tighter credit conditions for highly indebted firms. More recently, China has announced a set of policies to help address local municipality debt issues, but these measures seem to be far smaller than what would be necessary to change the course of these economic trends.

We think that China’s future economic path has already been laid. The only questions in our minds are when the fade to irrelevance happens and whether China will go out with a whimper or a bang.

For more news, information, and strategy, visit the ETF Strategist Channel.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.