By DeFred Folts III, Managing Partner Chief Investment Strategist, and Eric Biegeleisen, CFA, Portfolio Manager Deputy Chief Investment Officer

Equities:

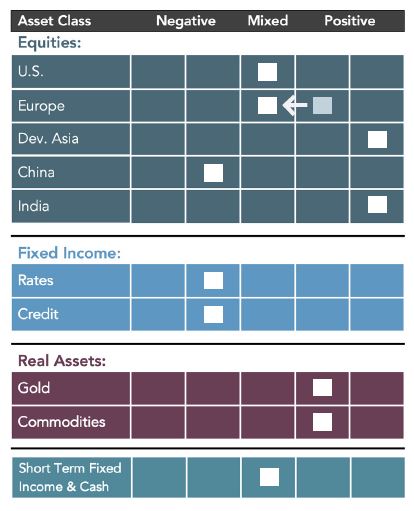

Equities:

▶ The outlook for U.S. equities has improved somewhat – though not uniformly so. Valuations continue to be near all-time highs for large-cap growth U.S. equities, which have benefitted from an extended regime of ultra-low interest rates. However, cyclical, value-oriented stocks offer more compelling valuations. In addition, should interest rates continue to rise, these stocks could prove to be less vulnerable to a somewhat higher interest rate environment and could perform well. At the next FOMC meeting in November, the Fed may announce the timing and scale of its tapering of asset purchases. For now, markets have seemingly taken the Fed’s presumed course of action somewhat in stride. However, as with prior tapering announcements, markets could still sell-off on this news. 3EDGE’s model research will focus on any signs of a regime shift driven by potential changes in inflationary expectations and monetary policy over the coming months.

▶ Japan equities enjoyed a sharp rally in September on the heels of the resignation of Prime Minister Yoshihide Suga, as market participants had been hoping for a fresh face with a different approach to handle the stalled economy and lackluster coronavirus response. Instead, in a surprise result, Fumiko Kishida, a former foreign minister, won the election and he has begun to discuss policies unfavorable to the stock market, such as higher capital gains taxes. Consequently, Japanese equities have suffered another setback. However, the new leadership may still tackle these issues more effectively, and it is also possible that the Bank of Japan may add additional stimulus measures to the Japanese economy.

▶ The outlook for European equities has softened somewhat. As Europe experiences its fastest increase in prices in over a decade, risks from increasing inflation may result in more dramatic tightening by the ECB to control inflationary pressures, thereby reducing monetary stimulus, which could negatively impact European equities. In addition, Europe could be facing a brutal winter with the potential for shortages of natural gas leading to spikes in energy costs – further exacerbating their inflation problem.

▶ India equities continue to exhibit positive investor psychology alongside favorable economics, most notably the steepening of the yield curve measure. Accommodative monetary and fiscal policies are expected to continue heading into the upcoming elections.

▶ The outlook for China equities remains unfavorable. Recent policy restrictions by the Chinese government have increased investor uncertainty. In addition, insolvency issues with the Chinese property development firm Evergrande and other Chinese real estate developers have impacted the cost of borrowing for many Chinese companies. Recently, China’s high-yield bond rates exceeded 15%, higher than during the financial crisis of 2008 and well above the U.S. high-yield rate of roughly 4%. While the Chinese government has begun to explore approaches involving asset sales and debt restructuring, the repercussions could further weaken an already slowing Chinese economy.

Fixed Income:

▶ The risk/return trade-off in U.S. Treasuries remains uncompelling as the entire Treasury yield curve continues to yield less than the expected inflation rate. The recent rise in yields underscores the risks associated with longer duration fixed-income investments. Also, any rise in the 10-year U.S. Treasury yield, possibly driven by higher inflationary expectations or Fed tapering, would result in the depreciation of bond principal.

▶ With credit spreads near all-time low levels, the yield associated with investment grade and high yield corporate debt markets present unattractive risk-return trade-offs. Not surprisingly, corporations have taken advantage of the extraordinarily low interest rate environment to issue more debt. For example, $786 billion of junk bonds have been issued in the U.S. thus far in 2021, surpassing the previous record for an entire year set in 2008. Should the global economy slow from here, corporate spreads could widen, causing painful losses.

Real Assets:

▶ Although Gold has struggled thus far in 2021, it remains relatively attractive and continues to be supported by negative real yields (nominal yields less expected inflation). In addition, concerns regarding peak growth and an uneven recovery in labor markets could delay the Fed’s plans to taper. However, should inflation prove to be more persistent than transient, the Fed will have to perform a delicate balancing act to solve for their dual mandate, i.e., monetary tightening to control rising inflation may slow growth while continued loose policy to encourage growth may raise inflationary expectations.

▶ Commodities maintain a somewhat positive outlook. Global supply shocks continue to push prices higher across the commodities complex, thereby increasing the upside risk to the global inflation outlook. The price of a barrel of oil recently reached its highest level since 2014, and surging natural gas prices have also raised the prospect of increased demand for oil products as winter approaches. At the same time, a potential slowdown in China may somewhat counteract this surge as China’s demand for raw materials has been a significant growth engine for the global economy.

DISCLOSURES: This commentary and analysis is intended for information purposes only and is as of October 8, 2021. This commentary does not constitute an offer to sell or solicitation of an offer to buy any securities. The opinions expressed in View From the EDGE® are those of Mr. Folts and Mr. Biegeleisen and are subject to change without notice in reaction to shifting market conditions. This commentary is not intended to provide personal investment advice and does not take into account the unique investment objectives and financial situation of the reader. Investors should only seek investment advice from their individual financial adviser. These observations include information from sources 3EDGE believes to be reliable, but the accuracy of such information cannot be guaranteed. Investments including common stocks, fixed income, commodities, ETNs and ETFs involve the risk of loss that investors should be prepared to bear. Investment in the 3EDGE investment strategies entails substantial risks and there can be no assurance that the strategies’ investment objectives will be achieved. Real Assets (Gold & Commodities) includes precious metals such as gold as well as investments that operate and derive much of their revenue in real assets, e.g., MLPs, metals and mining corporations, etc. Intermediate-Term Fixed Income includes fixed income funds with an average duration of greater than 2 years and less than 10 years. Short-Term Fixed Income and Cash includes cash, cash equivalents, money market funds, and fixed income funds with an average duration of 2 years or less. Past performance is not indicative of future results.

View from the EDGE is a registered trademark of 3EDGE Asset Management, LP.

About 3EDGE

3EDGE Asset Management, LP, is a multi-asset investment management firm serving institutional investors and private clients. 3EDGE strategies act as tactical diversifiers, seeking to generate consis-tent, long-term investment returns, regardless of market conditions, while managing downside risks.

The primary investment vehicles utilized in portfo-lio construction are index Exchange Traded Funds (ETFs). The investment research process is driven by the firm’s proprietary global capital markets mod-el. The model is stress-tested over 150 years of market history and translates decades of research and investment experience into a system of causal rules and algorithms to describe global capital mar-ket behavior. 3EDGE offers a full suite of solutions, each with a target rate of return and risk parame-ters, to meet investors’ different objectives.