By DeFred Folts III, Managing Partner, Chief Investment Strategist, and Eric Biegeleisen, CFA, Managing Director, Research Portfolio Manager

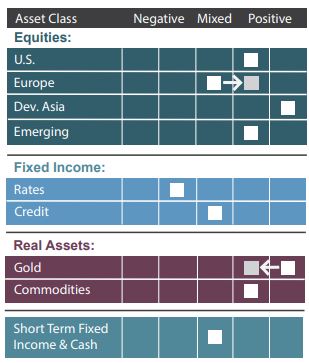

Equities:

Equities:

- U.S. Equities: Major U.S. equity market indices continue to reach all-time highs as well as record levels of overvaluation by our measure. However, even at elevated valuations, monetary and fiscal stimulus remains supportive. In addition, high-yield credit spreads remain narrow. A steepening global yield curve is also a positive development signaling higher growth prospects. U.S. equities also continue to benefit, at least in the short-term, from positive price momentum and favorable investor behavior which could be described as market euphoria. The extreme level of overvaluation of the U.S. equity markets continues to highlight their potential downside risk.

- Japanese equities remain the most attractive equity asset class in our model research. More compelling valuations, a continued narrowing of high-yield credit spreads, a steepening yield curve and sustained monetary stimulus from the Bank of Japan all contribute favorably to this outlook. Japan has dealt with the coronavirus pandemic better than many other countries, and because of its export-oriented economy is well-positioned to benefit from a rebound in global economic activity. The potential for continuing positive investor psychology could further enhance the outlook for Japanese equities as projected 2021 earnings for the companies in the Japan MSCI index are expected to increase dramatically throughout the remainder of 2021.

- European Equities: European companies should continue to benefit from the sustained and extraordinary monetary and fiscal stimulus required to support the region because of a slower recovery from the coronavirus pandemic and inconsistent progress on vaccinations. Also, the recent strength of the U.S. dollar relative to the Euro could be positive for European equities since a material percentage of companies based in Europe export their products worldwide. Lower local exchange rates can help exporters either expand market share and/or profit margins due to the price advantages a lower exchange rate provides.

- Emerging Market Equities: The positive impact of a steepening U.S. yield curve is offset by rising yields on longer-term U.S. Treasuries and a commensurate strengthening of the U.S. dollar, negatively impacting the attractiveness of EM equities. However, emerging market countries and their equity markets should continue to benefit from any additional fiscal stimulus from the U.S. government given the degree to which the U.S. imports from emerging market countries.

Fixed Income:

- In the first quarter of 2021, interest rates on longer-term U.S. Treasuries increased dramatically. Even at these higher yields, U.S. Treasuries represent an unattractive risk-return trade-off as they continue to yield less than the market’s expected inflation rate across nearly all maturities. Should interest rates continue to move higher, bond market investors would also face the prospect of further capital depreciation.

- Caused in part by investors searching for yield, expectations for economic recovery and the Fed’s continued tacit support of the credit markets (corporate bonds), credit spreads – the difference between high-yield and AAA-grade bond yields – continue to narrow. Short-term risks to credit remain as any accident in the financial markets could cause credit spreads to widen abruptly.

Real Assets:

- Although gold has struggled thus far in 2021, it continues to be supported by negative real (nominal rates minus inflation expectations) interest rates. Gold is an asset class than can serve as a critical portfolio hedge against the prospects of future central bank money printing and financial repression over the longer term. Gold could also benefit from continued fiscal stimulus from the Biden administration which could raise the prospects of future inflation, especially if the Fed also acts to further repress long-term bond yields. However, rising real long-term interest rates are currently acting as a headwind for gold in the shorter to intermediate term, and sustained downward pressure on the price of gold could encourage further selling and negatively impact the model outlook.

- Commodities remain attractive due to the longstanding relative undervaluation of real assets and the prospect of a strong global economic recovery in the second half of 2021. Other factors positively impacting real assets include; appreciation of the Chinese yuan, narrow high-yield credit spreads, a steepening of U.S. and global yield curves and positive price momentum. These positives are somewhat offset by the increase in the value of the U.S. dollar thus far in 2021

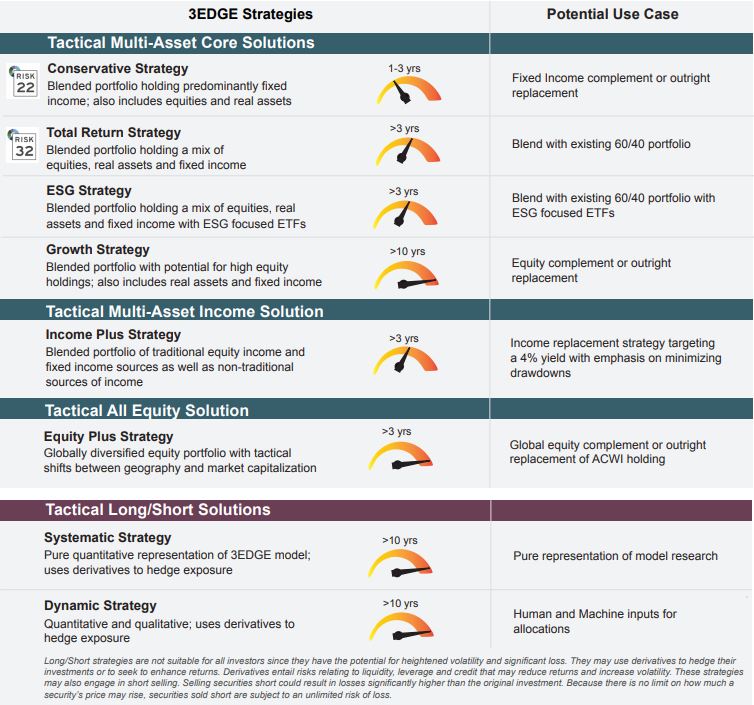

3EDGE Solutions Designed to Smooth the Ride

Seeking to manage volatility and downside risk while providing the potential to be additive to investment returns

About 3EDGE

3EDGE Asset Management, LP, is a global, multi-asset investment management firm serving institutional investors and private clients. 3EDGE strategies act as tactical diversifiers, seeking to generate consistent, long-term investment returns, regardless of market conditions, while managing downside risks.

The primary investment vehicles utilized in portfolio construction are index Exchange Traded Funds (ETFs). The investment research process is driven by the firm’s proprietary global capital markets model. The model is stress-tested over 150 years of market history and translates decades of research and investment experience into a system of causal rules and algorithms to describe global capital market behavior. 3EDGE offers a full suite of solutions, each with a target rate of return and risk parameters, to meet investors’ different objectives.

DISCLOSURES: This commentary and analysis is intended for information purposes only and is as of April 2, 2021. This commentary does not constitute an offer to sell or solicitation of an offer to buy any securities. The opinions expressed in View From the EDGE® are those of Mr. Folts and Mr. Biegeleisen and are subject to change without notice in reaction to shifting market conditions. This commentary is not intended to provide personal investment advice and does not take into account the unique investment objectives and financial situation of the reader. Investors should only seek investment advice from their individual financial adviser. These observations include information from sources 3EDGE believes to be reliable, but the accuracy of such information cannot be guaranteed. Investments including common stocks, fixed income, commodities, ETNs and ETFs involve the risk of loss that investors should be prepared to bear. Investment in the 3EDGE investment strategies entails substantial risks and there can be no assurance that the strategies’ investment objectives will be achieved. Real Assets (Gold & Commodities) includes precious metals such as gold as well as investments that operate and derive much of their revenue in real assets, e.g., MLPs, metals and mining corporations, etc. Intermediate-Term Fixed Income includes fixed income funds with an average duration of greater than 2 years and less than 10 years. Short-Term Fixed Income and Cash includes cash, cash equivalents, money market funds, and fixed income funds with an average duration of 2 years or less. Past performance may not be indicative of future results.

The Risk Number®, a proprietary scaled index developed by Riskalyze to quantify the risk of a portfolio, is calculated based on downside risk on a scale from 1- 99. The greater the potential loss, the greater the number. The Risk Number® includes analysis and proprietary information of Riskalyze. As of 3/31/21. Further information available at Riskalyze.com.

View from the EDGE is a registered trademark of 3EDGE Asset Management, LP