By David Lovell, Swan Global Investments

In a world of instant updates and daily stock market news, investors often fixate on chasing short-term returns or “beating the market.” This leads to dependency on trailing returns to determine “how well” an investment is performing.

But for investors with long-term goals, their focus should be, “Will I achieve my long-term goal on time?” Because of this, advisors should use rolling returns rather than trailing returns when choosing or evaluating investments and managers.

The Problem with Trailing Returns

The most common way of looking at returns in the investment industry is by using trailing returns. Trailing returns, or point-to-point returns, are a snapshot of the past, going back over a chosen period of time from a chosen anchor date, such as the latest quarter, 1-year, 3-year, or 5-year returns.

The problem with this approach is that It only measures a specified block of time. This can lead investors to expect future performance will mimic recent results, a phenomenon known as recency bias. With this late-stage bull market, what could investors expect going forward?

Misguided Expectations

If an investment or strategy just posted a really good quarter or year, that recent performance shines in the trailing return analysis of that period. This is known as end-period dependency. However, if you were to move that anchor date, and reviewed the same specific time frame, you may find a very different return for that period.

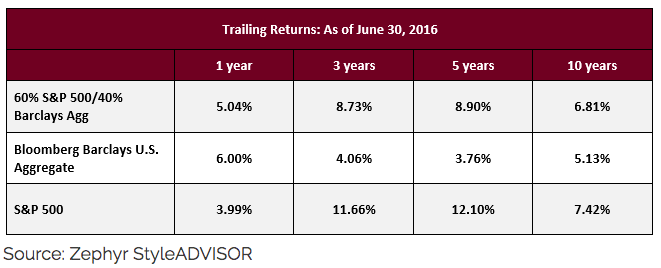

The following tables show the trailing returns for the S&P 500 Index, the Bloomberg Barclays U.S. Aggregate, and a combination of the two in a traditional 60% S&P and 40% Barclays. To illustrate the point, we looked back at snapshots of trailing returns going back 3 years from June of this year, 2019.

If you’re a financial planner basing decisions on these returns, it might be difficult to know what kind of expectations to set for your plan and how to frame the conversation with your clients. The difference among the S&P 500 returns is quite vast. With the one year at 3.99% and then nearly quadrupling for the 3- and 5-year before going back down to 7.42% for the trailing 10-year is far from being consistent.For portfolios heavily tilted toward equities, this inconsistency could threaten financial plans and expectations.

What a Difference a Year Makes

If we take a look at the returns one year later, the jump of the 1-year return for the S&P 500 to 17.90% is astounding. Just one year before it was at 3.99%. The variation is concerning, but even more problematic would be the anchoring of expectations on the new 1-year. The 3- and 5-year returns from the previous year (June 2016) are also significantly changed by June 30, 2017.

Another point to notice is the difference between the Bloomberg Barclays U.S. Aggregate from 2016 to 2017. Expectations went from a decent range of 4% to 6% in 2016 to returns below 5%… even negative on a trailing 1-year basis in 2017.

Three Years Later: 2016 vs 2019

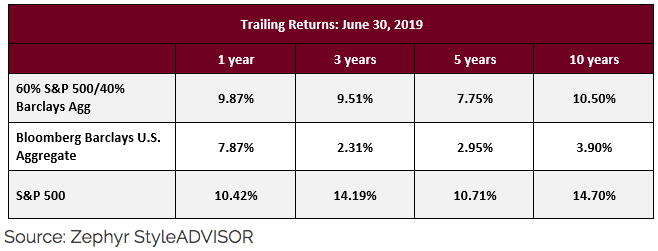

We see a similar difference even with three years of difference in our snapshots. Taking a look at the S&P 500 again, in 2016 the 1-year return was 3.99%.

Here in June 2019 that figure has more than tripled to 10.42%. While advisors may not base their long-term plan decisions on 1-year numbers, investors can often anchor their expectations to these numbers, causing them to regularly check in to make sure they’re reaching or “beating” the benchmark. Those are some high expectations to meet.

The 10-year doubled in 2019, mainly because 2008 has fallen off the trailing 10-year. With this in mind, 10-year returns going forward in this long bull market will look quite high from a larger historical perspective.

When the performance conversation arises, framing the evaluation around short-term trailing returns can lead to defining success or portfolio changes based on too short a time frame. Whether we’re looking at 1-year trailing returns one year apart or at the 1-, 3-, or 5- year returns in any given snapshot, the numbers are often vastly disparate and inconsistent, potentially skewing the returns expectations of investors and complicating long-term financial plan construction.

Couple that with short-term market noise and commentary, and investors can become all too eager to jump from one investment to another, chasing higher returns based on trailing 1, 3, and 5-year numbers.

Further, investment or manager selection based on short-term trailing numbers can lead to disappointment or worse, unmet financial plans and goals.

Timing Woes

The other problem with trailing returns is they don’t reflect the real investor experience or the real advisory experience. The reality is that investors do not start and stop their investment journeys at the same time (like, January 1st or December 31st of a given year, perhaps?). Two investors who begin with the same investment a quarter or two apart, much less a year or two apart, could have a very different experience. Evaluating recent trailing returns alone would not reflect this reality.

Instead of fixating on trailing returns or focusing on beating the market in such short time frames, it may be better to redefine the conversation on returns to a more holistic measurement: rolling returns.

Redefining Returns: Rolling Returns

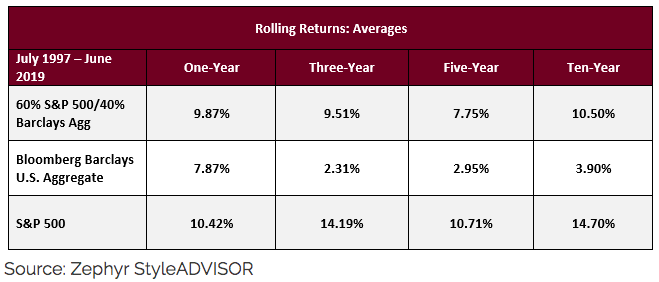

Rolling returns offer a more comprehensive view of returns: they consider returns over a fixed time period based on different start dates. Examining the average three-year rolling returns for a given investment can show you the return, or experience, investors would have had over any three-year period, even if they began investing at different times.

Performance Consistency

Unlike trailing returns, rolling returns reveal periods of bad performance or provide insight into the consistency of a manager’s strategy. A strategy that has consistent rolling returns, over various lengths or rolling periods, such as three, five, ten, fifteen, and even twenty-year periods, is a strategy that may have a higher probability of offering investors a more predictable set of future returns.

Where trailing returns can change each year, rolling returns show how consistent an investment is over time. Return disparity from year to year, or fixed period to fixed period, can make long-term financial planning difficult to implement and to maintain. If a given investment or strategy has generated consistent rolling returns across a range of longer periods, it may prove to be a dependable and reliable investment to include in a portfolio.

Reflects the Investor Experience

Trailing returns assumes an investment at the beginning of the year held through the end of the same year or one of the following years.

Realistically, though, investors invest at any point of the year and get out of an investment at any point.

Rolling returns give a snapshot of what the investor experience would look like from any month within the time frame specified. If rolling returns are consistent, investment timing risk is reduced.

Better Expectations

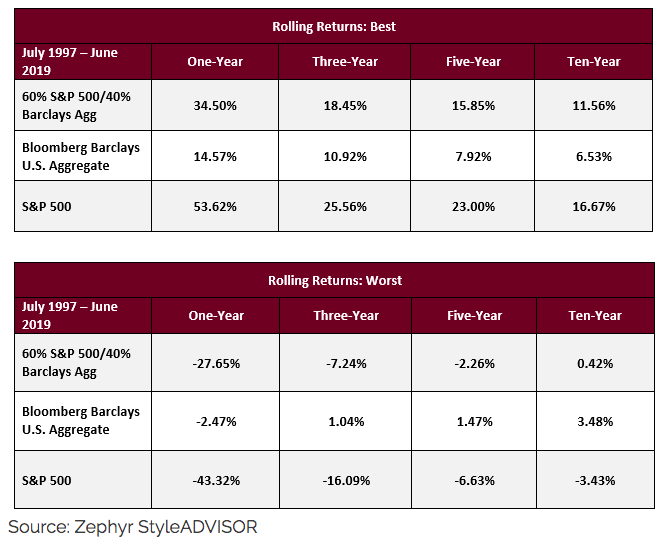

Rolling returns also reveal the best and worst return of a particular investment so investors can manage their expectations for better or worse. Seeing the best and the worst rolling returns over various time periods can give them a better sense of the fluctuations of their investments and whether they can stomach the potentiality of the worse.

While the best rolling period returns for the S&P 500 are impressive, the worst returns can be frightening. Whether an investor is okay with that loss potential may be an important factor to consider when creating plans and considering investor behavior.

Looking at these measures will provide better expectations for manager performance and result in better management of investor expectations. A large part of advising clients is managing their expectations and their emotions during stressful times. Using rolling returns may help advisors keep investors on track with their financial plans for longer.

Rolling Returns for the Long-Term

Advisors should help investors take longer view of their investments’ performance and consider looking at different measurements of returns or benchmarks. Investing should be about achieving long-term goals, not beating the market in the short term.

Rolling returns over longer-term periods (5, 10, 15, 20 years or more) can help advisors redefine the discussion around performance with client and frame a longer-term view. This may lead to improved investor expectations, keeping them on track with financial plans, and maintaining a better client relationship.

Important Notes and Disclosures:

Swan Global Investments, LLC is a SEC registered Investment Advisor that specializes in managing money using the proprietary Defined Risk Strategy (“DRS”). SEC registration does not denote any special training or qualification conferred by the SEC. Swan offers and manages the DRS for investors including individuals, institutions and other investment advisor firms. Any historical numbers, awards and recognitions presented are based on the performance of a (GIPS®) composite, Swan’s DRS Select Composite, which includes non-qualified discretionary accounts invested in since inception, July 1997, and are net of fees and expenses. Swan claims compliance with the Global Investment Performance Standards (GIPS®).

All Swan products utilize the Defined Risk Strategy (“DRS”), but may vary by asset class, regulatory offering type, etc. Accordingly, all Swan DRS product offerings will have different performance results due to offering differences and comparing results among the Swan products and composites may be of limited use. All data used herein; including the statistical information, verification and performance reports are available upon request. The S&P 500 Index is a market cap weighted index of 500 widely held stocks often used as a proxy for the overall U.S. equity market. Indexes are unmanaged and have no fees or expenses. An investment cannot be made directly in an index. Swan’s investments may consist of securities which vary significantly from those in the benchmark indexes listed above and performance calculation methods may not be entirely comparable. Accordingly, comparing results shown to those of such indexes may be of limited use. The adviser’s dependence on its DRS process and judgments about the attractiveness, value and potential appreciation of particular ETFs and options in which the adviser invests or writes may prove to be incorrect and may not produce the desired results. There is no guarantee any investment or the DRS will meet its objectives. All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is not a guarantee of future results and there can be no assurance, and investors should not assume, that future performance will be comparable to past performance. All investment strategies have the potential for profit or loss. Further information is available upon request by contacting the company directly at 970-382-8901 or www.swanglobalinvestments.com. 325-SGI-082819