Stock Market is a Barometer of Uncertainty, not Economic Prosperity

In the tech rally of the late 90’s and early 2000’s, we looked to our companies and institutions to provide us with guidance and protection. The government supported its constituents, the Federal Reserve protected the economy for the average American, and the news was a trusted source. We believed the government had our best interest in mind. Fast forward 20 years, and the freedom of information brought by the age of social media has ruined most trust in the establishment. We won’t go into great detail of how we got here, we’ll just comment that political contributions and the Federal Reserve’s actions have equal influence.

Every time there is volatility, there is inevitably some portion of the Fortune 500’s and the 1%’s that get even better access to credit than they did before, through lower interest rates. Banks are eager to lend at unheard of rates, giving these entities and individuals ample cash to deploy right when fear and volatility peaks. It’s ironic that when we spent so much time restricting which individuals and entities have access to credit in an effort to protect the “little guy,” we unintentionally put that same group at a significant disadvantage when credit is most useful: in times of market volatility, not at market highs. When volatility spikes, the only loans that appear safe are to the 1% and Fortune 500’s. There goes another layer of the middle class.

None of this was done intentionally. In theory, Quantitative Easing (QE) does help the entire pie grow, but on a micro level, it can have significant unintended consequences. What do we mean by that? QE was supposed to keep the economic system humming. Instead, it causes asset prices to shave off a layer of the middle class with each round of volatility. The practice of economic theory often results in unintended consequences that directly conflict its intended purpose.

In truth, neither democrats nor republicans have proven to really support the average American. As we’ve said in past commentaries, there’s no bigger oligopoly in the world than the democrats and republicans in the United States.

Enter Wall Street Bets – Distributed, Decentralized Echo Chambers

For decades people have wondered if a third party may result in a political system. If Bitcoin is to be considered a potential end to paper currencies, Wall Street Bets (WSB) is attempting to be the same to Wall Street, and maybe even political parties. That comment might surprise you, as currently WSB appears to have its sights fixed on Wall Street (or rather the 1% of the 1% of Wall Street – one of the entities given unmatched access to leverage), but we believe this is the beginning of what will ultimately be the next generation of political activism.

What is a hedge fund or political party other than a group of individuals working for one specific goal? Is a distributed decentralized Reddit group really anything different if they truly believe in the ideal of the group?

Social media has democratized the hive effect, for better or for worse. We believe the next stage of WSB could extend beyond stocks. What about a Reddit impromptu labor union by way of strike? We are less than 6 months away from French rioters setting their central bank on fire. What happens if the hive switches focus to politics? What about if they strike by way of consumption? Is there a world where WSB decides to not use Amazon for a quarter? Or decide to not use a specific airline due to misaligned political view with its shareholders? Do WSB and the ESG movement coincide into one massive force? Considering many participants in WSB are not actually working for the betterment of the group (example 1 – not collecting interest and loaning shares of GME), truly anything is possible.

We’ve written about the book Sapiens a number of times in our commentaries over the last 2 years. This is due to the importance of storytelling in markets. Storytelling is why we felt comfortable getting aggressive in March 2020, and why we have serious market concerns today. Mid-March 2020, Pre QE, there was nothing but unknowns. We had no idea what the virus was, what it would do to our economy, or what our Federal Reserve’s response would be. In a world where value is attributed more and more to the potential of what your entity could be in the future, storytelling is more important than ever. Where would Tesla be today without Elon Musk’s storytelling? In reality, Tesla’s rise is really a shift in the story, from a car company to maybe the world leader in Artificial Intelligence and advanced battery storage.

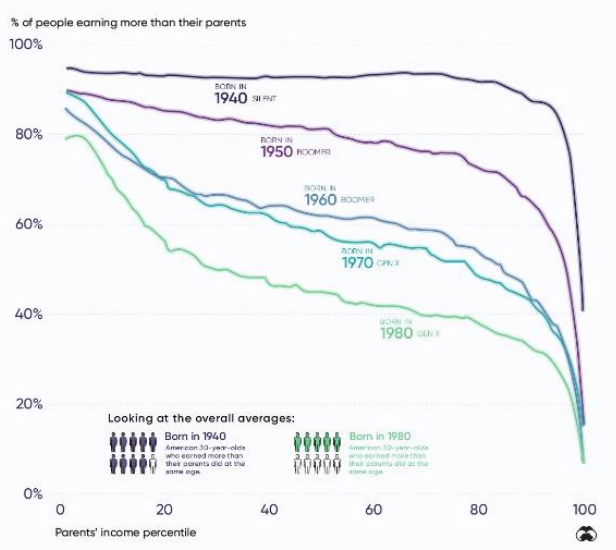

The turnover of the rich in the developed world has plummeted, and the odds of outperforming your parents looks like an upside-down Bitcoin chart. People under 30 own the smallest percentage of assets compared to any point in history. Some WSB members go as far as claiming their mission is payback for what the Great Financial Crisis did to their parents, their homes, and their families.

2020 – The Year “Buy the Dip” was Crowned King

In 2020, everyone finally realized the market and economy are two separate things. Millennials were once categorized as the “fear investor,” having grown up through the dot com bust and financial crisis. The once considered “fear investor” is now a “buy the dip” staunch believer. How did we get here? The answer is momentum and all things tech. Amazon, Google, Facebook, Tesla, Netflix, Alibaba, Bidu and Bitcoin are just some of the prime examples. How did this happen? QE allowed it to happen. If you have perceived future growth and a promise of an almost monopolistic market share over a particular industry, you are rewarded with extravagant multiples on future expected earnings and access to credit unmatched by historic norm. Before QE, profits used to matter. Not Wall Street adjusted EBITDA or 1999-like forecasting, but actual, taxable profit.

Built to be Acquired

A conservative approach is one that simply lacks funding and focus. The next wave of unicornlike companies continue to be ones essentially founded just to be acquired by one of the Global Internet of Things titans. We saw this with Slack and Salesforce. Musical chairs work like this – I lose a ton of money on disruptive technology so you do not have to, and so long as I do not run out of money, my dream can become your dream. The few industries with potential of surpassing the Global Internet of Things tech giants really only fall in a industries like artificial intelligence, genomics space, and the blockchain/crypto space. Tesla is a great example. Is Tesla really a pure AI company? Does their valuation make sense in any other world?

How this all Affected 2020

In March 2020, we wrote that the easiest trade out there was to avoid the zombie companies that needed to be propped up by the government, and focus on the Internet of Things (OGIG, EMQQ), genomics (ARKG), gig economy (GIGE), and crypto (BLOK). These companies benefited from never-before-seen levels of fiscal and monetary policy, and a supercharged adoption curve on multiple innovation fronts. Unfortunately, picking market segments with significant growth prospects is much more difficult in 2021. Many of the stories told in the great innovation shift of 2020 will not meet market expectations, while a select few will likely soar past them.

If 2020 was the Year that all Things Worked, what will 2021 Bring?

2020 was the year of innovative disruption in the face of a global pandemic. With so much fiscal and monetary stimulus in the economy, the massive innovation and adoption uptick might be the only thing keeping inflation in check. Those remaining few who believed the market and economy were meant to walk in unison were finally proven wrong in 2020. We all know the economy and market are two different things now. What if a “re-opened” economy actually kills productivity and tanks the market, even if it actually helps increase employment and general daily satisfaction of its market participants through vaccination? Or, a return to some sort of normalized life?

At some point, Buy the Dip will get burned. If we have any market expectations for 2021, it’s that it will be a year of many different market environments. We could see two drawdowns over 20% in 2021 with a strong Buy the Dip rally in between, but ultimately the range of outcomes is truly infinite – and that can be planned for.

Hope for the Future

Social Media has democratized information. As individuals in the economy, we know details about the owners of companies we use. The hive mentality of Wall Street Bets may seem adolescent, but in reality, it may be the first step towards purposeful wealth creation. With so much information, it’s not unlikely that consumers and small shareholders can actually choose where the margins go. What if hives decide that chefs or bus boys deserve a bigger piece of the pie, or retail clothing workers deserve a minimum wage of $20, and those agendas are pushed as shareholders and consumers? More than ever, individuals have the power to decide where to spend and invest their capital, with the closest thing to some sort of transparent democratized information available more than any time in history. it’s almost as if that’s the ultimate purpose of social media.

How We Invest in these Markets

As our very own ETF Professor likes to say, “structure matters.” There may be 5 ETFs for every thematic category, and though a dart board selection process worked in 2020, it will not work in 2021. Poorly constructed index products and overly concentrated active products should be allocated to with caution. Instead, seek unique construction with a thoughtful index methodology, or less concentration. Take SPDR S&P Retail ETF (XRT) for example. It peaked at just under a 20% allocation to GameStop on January 27th. This is an equally weighted indexed ETF with 95 names, with a next highest allocation of 1.7%. There is no world in which this vehicle should wait for quarter end to rebalance.

Overall, we are quite proud that our approach to these markets has been pretty much consistent since fall 2019. We continue to avoid broad market cap indexes in both equity and fixed income markets. We barbell risks in equities, fixed income, and alts. We are equally invested in the thematic innovation space as we are in negatively correlated alternative assets, and we rebalance religiously. If anything, we are seeking lower volatility, well constructed, more diversified (or smaller allocation to thinly sliced) thematic investments, paired with some deep value concentrated portfolios, while continuing to rebalance into negatively correlated alternatives as markets move. 2021 volatility will continue.

US Equities

US equity markets were up 18.37% percent for 2020 after an eye-popping 12.14% in Q4 measured by iShares Core S&P 500 ETF (IVV). Small caps, measured by the iShares S&P Small Cap ETF (IJR), returned just 0.91% for 2020, but 21.54% in Q4. 2020 was defined by the yin and yang between Invesco Nasdaq 100 ETF (QQQ) and small cap value. When one worked, the other didn’t, with QQQ’s taking the lead for most of the year. That is, until the fourth quarter, when everything went up. This is most likely due to investor fear dropping post-election. The most prominent difference of late is the change in expected earnings over the next year or so. If you recall, pre-Covid, margins had already begun to erode. With so much focus on the ESG movement, we think margin pressure is a real issue for a lot of companies, so to match this type of growth, we would need significant revenue growth. We think expectations are set too high at the moment. There’s a very real possibility that an opened economy actually hurts productivity via an unwind of the productivity growth created by the Covid innovation spikes, which would either mean inflation or a stalled economy. We continue to focus on narrowly sliced thematic ETFs, now with a focus on active management and diversification, paired with deep value managers providing diversification to the higher growth names in our portfolio.

International Developed Equities

MSCI ACWI ex US, measured by the iShares MSCI ACWI ex US ETF (ACWX), was up 10.48% percent for 2020, returning 16.95% for the 4th quarter. iShares MSCI EAFE (EFA) was up just 7.92% for the year as most of the returns came from emerging markets. EFA was also up an eye-popping 16.27% in Q4 alongside pretty much all other equity asset classes. International developed equities are the value play of all value plays, or a perpetual value trap lead by an unhealthy banking system hooked on the ECB. We believe there are definitely opportunities here but would limit market cap beta exposure if possible.

Emerging Market Equities

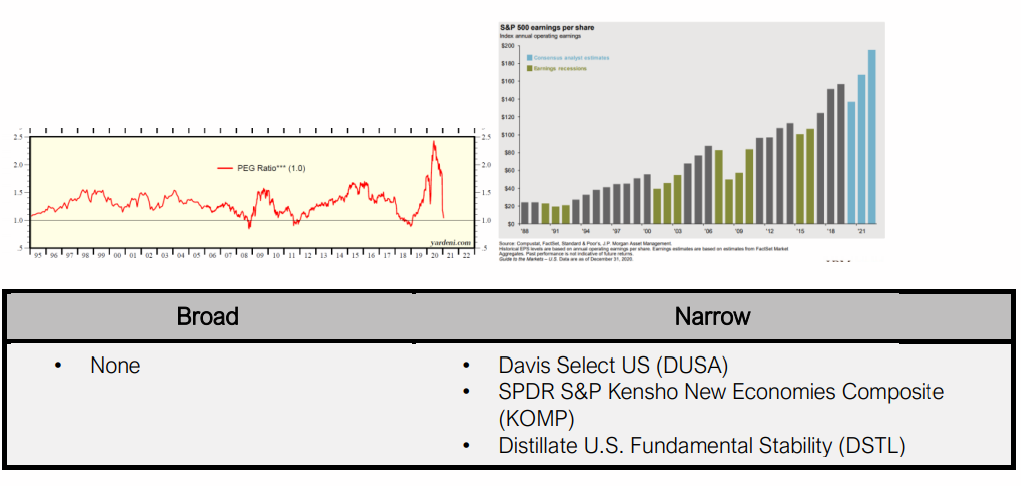

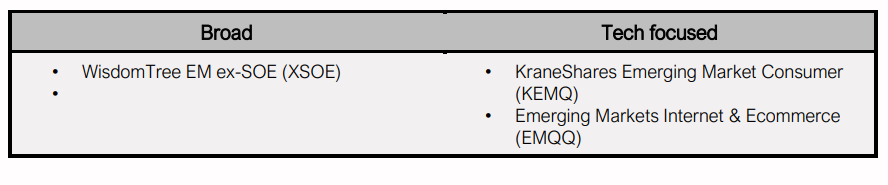

Emerging market Internet of Things (IOT) and ex-state-owned enterprise funds in this space continue to add alpha over broad benchmarks. Many of the IOT funds avoid state-owned enterprises all together. As a whole, emerging markets, measured by the iShares MSCI Emerging Markets ETF (EEM), was up 17.56% for 2020 and 19.43% for Q4. EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ) returned 81.13% for 2020 and 22.95% for Q4. Despite another year of outperformance, these names and many other growth themes still have PEG ratios more attractive than broad equities. Anti-trust issues with FAANG names only increase the likelihood of success in EM IOT, but recent announcements about Alibaba’s Ant potential IPO are encouraging.

Fixed Income

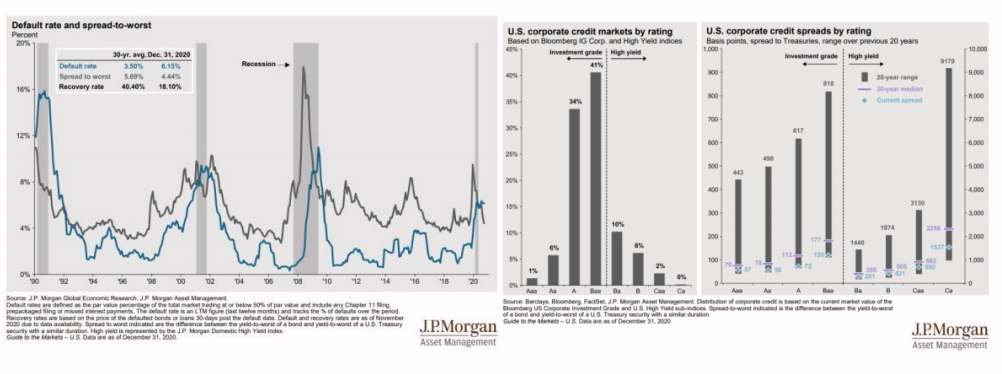

The Fed officially became co-investors in at least the bond side of a 60/40 portfolio in 2020 (the equity side may come in future market disruptions a la Japan). The Federal Reserve stepped in and bought shares of iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD) and iShares iBoxx $ High Yield Corporate Bond ETF (HYG), and US bond markets may never be the same again. iShares Core US Aggregate Bond ETF (AGG) returned 7.42% for the year, and long-term treasuries measured by the iShares 20+ Year Treasury Bond ETF (TLT) returned 17.92%. That return understates what a powerful investment long-term treasuries can be in a portfolio, as at the peak, those returns were closer to 40-50% when markets were at their lows. This continues to be an excellent trading vehicle for diversification. Overall, we continue to avoid market cap weighted products and successfully rebalanced through the turmoil of 2020 with our barbell approach to risk in this space. Default rates (as seen below) have somewhat stabilized, but at current levels, historically will either rise or fall from here.

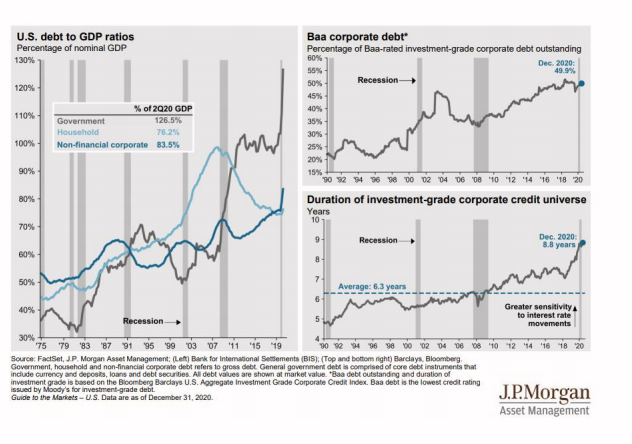

41% of US corporate credit falls into the BAA category, which is conveniently just above the category of high yield. This seems like a future behavioral finance experiment playing out in real time as there really is no rhyme or reason for just a skewed distribution here.

The duration uptick of investment grade credit will have consequences down the road, and US debt to GDP ratios on a government level are through the roof.

Alternatives

We continue to recommend a mixed alternative bucket consisting of long-term treasuries, gold, and AGFiQ US Market Neutral Anti-Beta Fund (BTAL). This year, we were able to rebalance between our alternatives and equities at market dislocations, which was very beneficial for YTD returns.

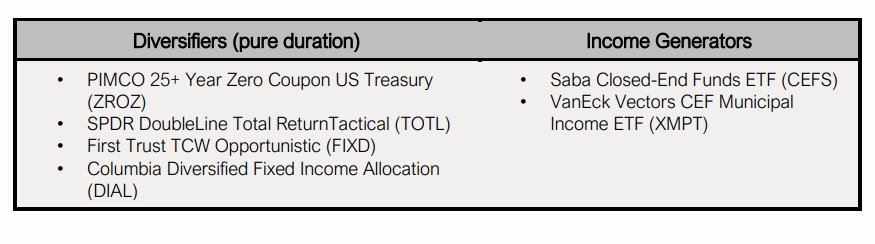

A hypothetical high-active-share reconstruction of a traditional 60/40:

• 10% Cash

• 5% PIMCO 25+ Year Zero Coupon US Treasury Index ETF (ZROZ)

• 5% Saba Closed-End Funds ETF (CEFS)

• 10% AGFiQ US Market Neutral Anti-Beta (BTAL)

• 10% SPDR Gold MiniShares Trust (GLDM)

• 10% Davis Select Worldwide ETF (DWLD)

• 10% ARK Innovation ETF (ARKK)

• 7.5% Emerging Markets Internet & Ecommerce (EMQQ)

• 7.5% SPDR S&P Kensho New Economies Comps (KOMP)

• 5% Distillate US Fundamental Stability & Value ETF (DSTL)

• 5% Roundhill BITKRAFT Eports & Digital Entertainment (NERD)

• 5% Roundhill Sports Betting & iGaming ETF (BETZ)

• 5% Amplify Transformational Data Sharing ETF (BLOK)

• 5% Sofi Gig Economy ETF (GIGE)

O’Shares Global Internet Giants ETF (OGIG) – removed

Conclusion

The Idea of Zero Interest Rates in the US is Causing this Bitcoin Rally

The United States is not Europe. European interest rates went negative, the ECB started propping up their banking industry as one of the sole buyers left of their debt, and the United States was ready to follow suit. However, Europe was only able to get away with this because there still existed a dominant market player with some resemblance of market normalcy in the United States, where the idea of rates going negative (pre-Covid) was considered as much of a black swan as bitcoin at $100k. The faith in the US dollar was still very strong around the globe. In 2020, the divergence between the highly correlated and ever-growing US debt and US GDP broke, in a bad way. The idea of negative short-term interest rates in all developed markets across the world now almost seems like a forgone conclusion if the pandemic morphs – even despite a steepening in the yield curve.

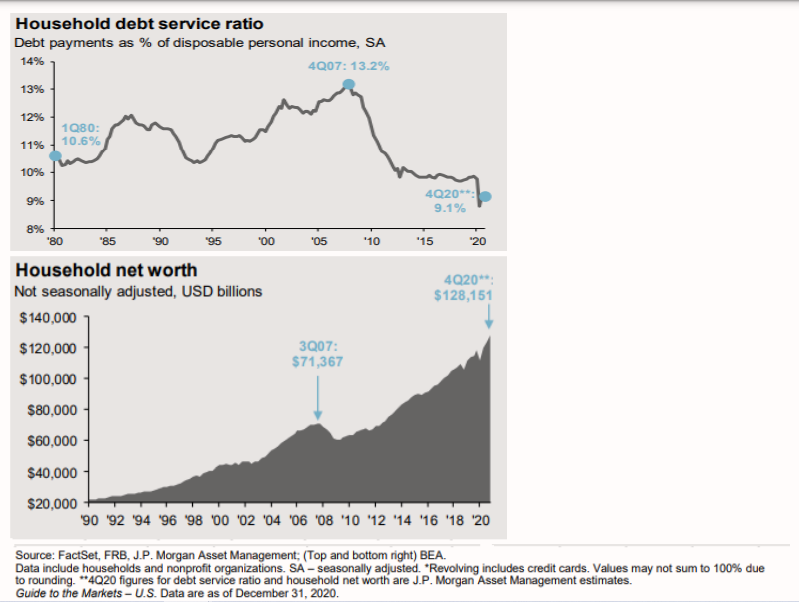

The K shaped recovery has left us in a vulnerable place in society. Households have more wealth and less debt payments than ever as a whole, in most part due to exceptionally low interest rates and unmatched federal reserve support.

Originally published by Toroso Investments, 2/10/21