By Matthew J. Krajna

With the reopening of the U.S. economy fully underway, pent-up demand has far outstripped COVID-related supply shortages of most major goods causing prices to surge in nearly all categories. Couple that with a labor shortage that remains stubbornly persistent and consumers are facing price increases from multiple fronts. Record low-interest rates and high levels of personal savings have created a backdrop that clearly stokes fears of an inflation problem.

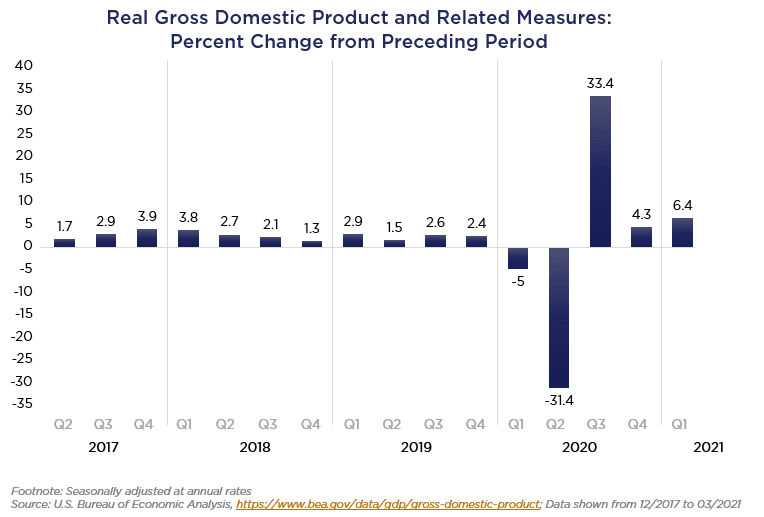

Last week’s Federal Open Market Committee (FOMC) meeting press conference Fed Chair Jay Powel upgraded the Committee’s view of the economy. Gross Domestic Product (GDP) in the U.S. is now expected to rise +7.0% this year, up from +6.5% prior.

Inflation, as measured by the Personal Consumption Expenditure (PCE) Index is now set to rise 3.0% in 2021, up from 2.4% prior. Even as FOMC projections see the unemployment rate falling, it’s likely going to be impacted by an estimated 2.6 million retirements during the pandemic, which is more than one-third of the 7.6 million jobs that were lost. Put differently, as the Federal Reserve sees the unemployment rate falling to 4.5% by year-end (down from 5.8% last month) wage pressures may persist, adding fuel to the inflationary fire impacting consumers. The median dot projects that FOMC members see the benchmark interest rate to rise to 0.60% from 0.00% by the end of 2023, on the back of above-trend inflation and the economic output gap closing.

For clients and advisors looking for an inflation hedge, there are various tilts that one can make to their investment portfolio: adding commodities, inflation-protected bonds, real assets, etc. For those looking for a one-stop-shop, consider the Nottingham Advisors Real Return strategy.

Nottingham’s Real Return strategy seeks to deliver positive real returns over a business cycle, targeting +300bps above the Consumer Price Index (CPI) through dedicated exposures to Equities, Commodities, Fixed Income, and Alternatives via exchange-traded funds (ETFs). This four-quadrant approach incorporates both strategic and tactical allocations to assets that may hedge inflation, provide a pass-through mechanism, or have historically performed well during bouts of rising prices. Nottingham’s Investment Policy Committee (IPC) is tasked with over or underweighting each of the four quadrants, and selecting the appropriate allocations within each.

- Equities – From a strategic standpoint, stocks have traditionally served as an ideal inflation hedge, with companies able to pass on price increases to consumers. Companies growing dividends at a rate above inflation have historically been attractive, as have value-oriented sectors that tend to perform well when the economic backdrop is favorable and interest rates are rising. Tactically speaking, companies that are able to pass along price increases to consumers while maintaining or expanding margins may also perform well (i.e. Homebuilders), and represent a timely example of a case in which the builders themselves see costs being pushed to buyers while their profit margins expand.

- Commodities – Intuitively, commodities tend to perform well in inflationary environments as prices are increasing due to demand and a weaker base currency. For most commodities, their base price is in U.S. Dollars, and as inflation erodes the value of the base currency, prices tend to adjust accordingly.

- In the current boom economy, both a surge in demand and expectations for inflation to climb further have led to a surge in all types of commodities, from agriculture to energy and precious and industrial metals. Investors can gain exposure to commodities primarily in two ways: to the commodity directly (most ETFs hold futures contracts offering exposure to broad commodities) or through select equities (i.e. miners, pipelines, agribusinesses, upstream natural resource producers, etc.).

- Fixed Income – Historically speaking, floating rate bonds with resetting coupons are the ideal type of bond to own when rates are going up (price and yield move inversely with each other) whereas an investor would otherwise be stuck with a fixed rate bond whose value may erode with rising rates. Treasury inflation-protected securities (TIPS) have also been a go-to source of purchasing power protection in lieu of their fixed-rate counterparts.

- Alternatives – These types of investments come in many shapes and sizes, and Nottingham’s IPC primarily focuses on traditional alternatives (as opposed to alternative strategies) such as Real Estate that tends to have inflation escalators built into long-term contracts with tenants. Tactically, the IPC has favored growth REITs such as Industrial REIT companies involved in warehousing and logistics that both benefit from a secular trend towards e-commerce and a built-in inflation pass-through.

Nottingham’s Real Return strategy can be thought of as an all-weather type strategy fit for a standalone portfolio allocation or as a “sleeve” in a larger allocation where the underlying assets are fixed (i.e. traditional bond portfolio). Given its unique four-quadrant approach and strategic-tactical construct, the Real Return strategy is both dynamic and flexible enough to adapt to current market conditions and prepare for any coming inflation spikes.

Nottingham Advisors offers both institutional and individual clients experience, sophistication, and professionalism when helping them achieve their goals. With over 40 years of serving Western New York and clients in more than 30 states, Nottingham tailors each solution to fit the specific needs of each client.

For more information about Nottingham’s offerings, visit www.nottinghamadvisors.com or call 716-633-3800.

Nottingham Advisors, Inc. (“Nottingham”) is an SEC registered investment adviser with its principal place of business in the State of New York. Registration does not imply a certain level of skill or training. For information pertaining to the registration status of Nottingham, as well as its fees and services, please refer to our disclosure statement as asset forth on Form ADV, available upon request or via the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). The information contained herein should not be construed as personalized investment advice or a solicitation to buy or sell any security. Investing in the stock market involves the risk of loss, including loss of principal invested, and may not be suitable for all investors. Past performance is no guarantee of future results. This material contains certain forward-looking statements which indicate future possibilities. Actual results may differ materially from the expectations portrayed in such forward-looking statements. As such, there is no guarantee that any views and opinions expressed in this material will come to pass. Additionally, this material contains information derived from third party sources. Although we believe these sources to be reliable, we make no representations as to the accuracy of any information prepared by any unaffiliated third party incorporated herein, and take no responsibility therefore. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change without prior notice.