By Kevin Nicholson, CFA, Global Fixed Income Co-CIO, Co-Head of Investment Committee

SUMMARY

- We believe the Fed’s actions should not derail investors before it begins raising interest rates.

- We believe the trend and sentiment both suggest proceeding with some caution.

- Collectively, the three tactical rules still point to a pro-risk allocation, in our view.

Last weekend, Novak Djokovic attempted to capture the calendar grand slam in tennis by winning the US Open, after already winning the Australian Open, the French Open, and Wimbledon earlier in the year. Djokovic fell short in his quest and now our three tactical rules are attempting their version of a calendar grand slam: signaling pro-risk for the entirety of 2021. As we begin to close-out the third quarter, we explore the status of “Don’t Fight the Fed”, “Don’t Fight the Trend”, and “Beware of the Crowd at Extremes” which appear to be painting the lines (shots that land on the lines); still pro-risk but proceeding with caution.

Don’t Fight the Fed: (Serving Up an Ace)

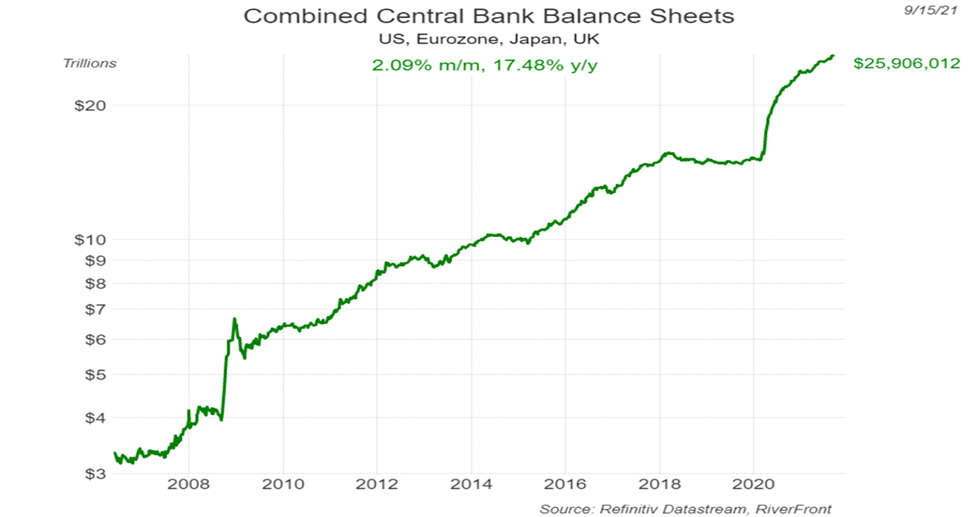

Since the beginning of the year, the Federal Reserve (Fed) has grown its balance sheet by just over $1 trillion. In June, the Fed increased the rate that it pays participating banks to 5 basis points, in order to soak up excess liquidity. Additionally, the Fed has stated it will delay raising interest rates, even though it is planning to begin tapering its $120 billion purchases of Treasuries and mortgage-backed securities sometime before year-end. While we acknowledge tapering will make the Fed less accommodative, we believe they will still be printing money for a period of time and will still be acting in investors’ best interest by delaying rate hikes. Therefore, we believe the Fed is still on investors’ side regarding monetary policy.

Similar to the US, most international central banks have started talking about tapering, but have yet to trim their money-printing programs. Of the major international central banks that we follow, European Central Bank (ECB), Bank of England (BOE), and the Bank of Japan (BOJ), only the BOJ has not considered any form of tapering. Despite international central banks considering tapering, they have not done so and remain on investors’ side, as illustrated by the chart below:

Past performance is no guarantee of future results. Shown for illustrative purposes. Not indicative of RiverFront portfolio performance.

Central banks around the world continue to serve up aces for investors, in our view. When a tennis player serves an ace – an unreturnable serve – their confidence builds, and by keeping rates low, we think central banks are signaling to investors that it is okay to have a higher risk profile and invest in equities.

Don’t Fight the Trend: (Swinging Away at the Baseline)

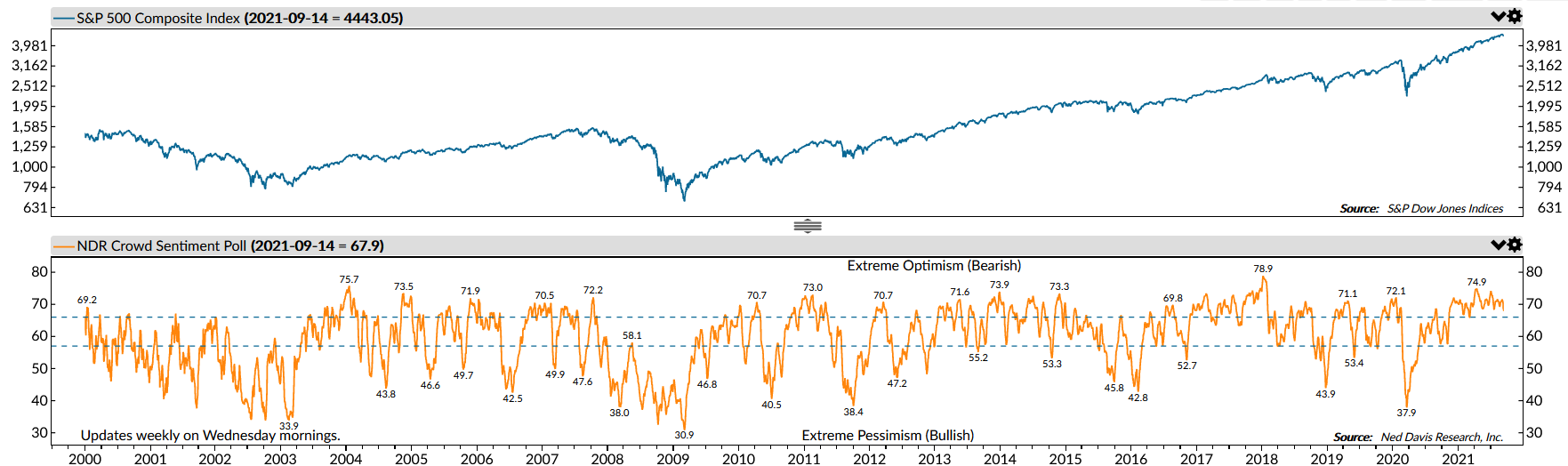

We define the US primary stock market ‘trend’ as the 200-day moving average of the S&P 500. Currently, the trend in the US is rising at an annualized rate of 35%, an extraordinarily strong slope which we believe is unsustainable for long periods of time. However, through the lens of our proprietary trend heatmap, the strength of the trend is still pointing to positive future returns over the next 3 months. While we continue to watch the trend cautiously, its positive momentum has helped the S&P 500 continually make new highs. The international trend represented by the 200-day moving average of the MSCI All-Country World-Ex US Index, on the other hand is at a less extreme 20%.

Past performance is no guarantee of future results. Shown for illustrative purposes. Not indicative of RiverFront portfolio performance.

Given the strength of the trends domestically and internationally, we would compare this to a tennis player standing at the baseline trying to keep the ball in play, increasingly aware that too strong of a swing could cost them the point.

Beware of the Crowd at Extremes: (Double Faulting)

The Crowd has been riding high this year as it has benefitted from strong earnings growth, supportive Fed policy, and government transfer payments in the US. As the economy has reopened from the pandemic, the Crowd has remained in the extreme optimism zone. The elevated level of crowd sentiment has concerned us for all of 2021, as we recognize that at some point the music will stop and the party will end. We believe that sentiment at extreme optimistic levels sets investors up for disappointment, similar to the letdown a tennis player feels when they double fault. At current levels, looking at crowd sentiment in isolation would prompt us to reduce the level of equities in the portfolio.

Copyright 2021 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/.

Conclusion:

Unlike Djokovic, we place greater odds on our three tactical rules achieving the rare calendar grand slam, as collectively they still point to a pro-risk portfolio positioning. The Fed and global central banks are accommodative, the trend is positive and growing rapidly, and excessive crowd optimism is being worked off by the current pullback. In keeping with these conclusions, the balanced portfolios currently have equity allocations that are 6 to 7 percentage points higher than the composite benchmark allocation.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

Standard & Poor’s (S&P) 500 Index TR USD (Large Cap) measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

MSCI ACWI ex USA Index captures large and mid cap representation across 22 of 23 developed markets (DM) countries (excluding the US) and 26 emerging markets (EM) countries.

The 200-day moving average is a popular technical indicator which investors use to analyze price trends. It is simply a security’s average closing price over the last 200 days.

In a rising interest rate environment, the value of fixed-income securities generally declines.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below. Changes in the value of foreign currencies compared to the U.S. dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the U.S. dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio. Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the U.S. and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-U.S. securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Mortgage-backed securities are subject to prepayment and extension risk; as such, they react differently to changes in interest rates than other bonds. Small movements in interest rates may quickly and significantly reduce the value of certain mortgage backed securities.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

Don’t Fight the Fed – ‘Supportive’ means the Fed’s monetary policy regarding inflation and employment is in what we believe based on our analysis to be the investors’ best interest; ‘Against’ means the Fed’s monetary policy, in our view, is going against the investors’ best interest; ‘Neutral’ means the Fed’s monetary policy is neither supportive or against the investors’ best interest in our view. Don’t Fight the Trend – Terms correlate to the 200-day moving average as it relates to the equity indexes: ‘Positive’ means that the trend is rising, ‘Flat’ means the trend is flat, ‘Negative’ means the trend is falling. Beware the Crowd at Extremes – Terms correlate to the NDR Crowd Sentiment Poll and its measurement of Extreme Optimism (Bearish), Neutral, or Extreme Pessimism (Bullish).

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2021 RiverFront Investment Group. All Rights Reserved. ID 1843476