By Kevin Nicholson, CFA, Global Fixed Income Co-CIO, Co-Head of Investment Committee

SUMMARY

- Negative yielding debt, the US Treasury debt ceiling, and the delta variant are factors we believe are driving the ten-year yield lower.

- We expect the ten-year Treasury to remain below 1.50% until tapering begins and moving up to 1.50% to 1.75% range by year-end.

- Covered calls allow investors to collect additional income using equity securities they already own in their portfolio.

Investors Seeking Alternatives

Temperatures are rising as we get deeper into the summer and the bond market has investors feeling the heat as interest rates have fallen in recent weeks. The low levels of Treasuries combined with corporate credit spreads, both investment grade and high yield, have investors wondering how they will ever generate income in their portfolios. We believe that the ten-year will remain below 1.50% through the summer. Once the Federal Reserve (Fed) begins to taper, we believe that yields will move back into the 1.50% to 1.75% range. However, even if yields rise to 1.75% this is not enough to generate the appropriate amount of income for investors who are nearing retirement. Therefore, we believe investors will have to find alternative ways to generate income. One way to do this is through a covered call strategy (which we explain below), as we have recently done in our balanced portfolios.

Bond Market: What is driving yields lower?

Ten-year Treasury yields fell below 1.50% in early June and currently are 1.22%. We believe that the bond rally has been driven by the increasing amount of negative yielding debt overseas, the US Treasury facing an upcoming debt ceiling that is limiting supply, and the COVID-19 delta variant threatening the global economy’s recovery.

- Negative Yielding Debt– In May the amount of negative yielding debt fell to $12.8 trillion. However, since then yields have fallen further as the pandemic has caused European and Japanese debt to go more negative. Currently, for those countries there is $15.2 trillion outstanding. Given hedging costs have increased only a few basis points during that time, we believe it is more advantageous for citizens of these countries to sell their currencies and buy Treasuries.

- US Treasury Debt Ceiling– In 2019 the debt ceiling was suspended. However, it is set to be reinstated at the end of the month. This has forced the US Treasury Department to rein in debt issuance, creating a supply shortage when there is so much capital looking for a home.

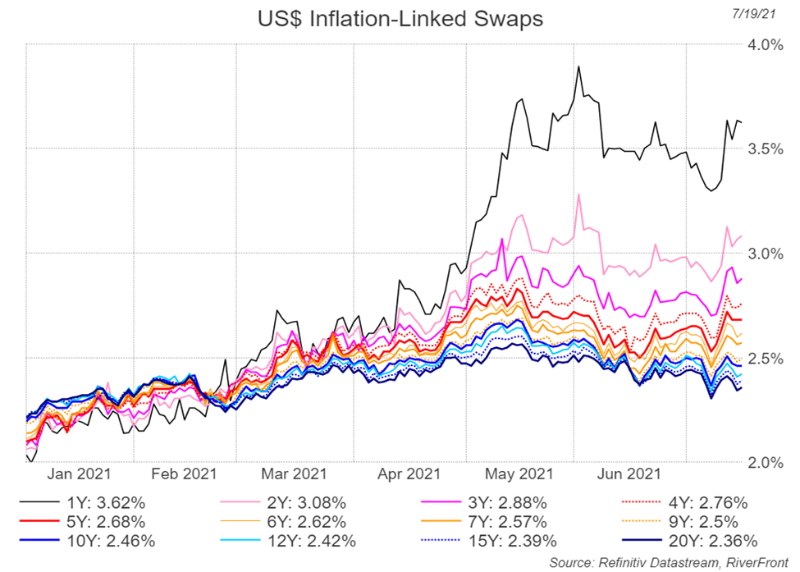

- Delta Variant– The rise of the delta variant has changed the calculus for the global economic recovery. Investors are now expecting the rate of growth to slow from previous expectations as portions of the global economy are delayed from re-opening, according to the signals from the bond market. Slower growth means lower demand and less inflation, and over the last month or so inflation expectations have fallen as shown in the chart left.

Past performance is no guarantee of future results. Shown for illustrative purposes. Not indicative of RiverFront portfolio performance.

What is it the bond market signaling?

Currently, the bond market is signaling to investors that inflation is transitory as yields have come down from the high of the year of 1.74% made on March 31st, despite headline CPI (Consumer Price Index) readings of 5.4% year over year. Additionally, the bond market is signaling that the outsized growth that we have witnessed coming out of the pandemic is not sustainable and that growth will slow more than previously expected, in our opinion. Beyond the signals being sent by the recent action of the Treasury market, the accommodative stance by the Fed has provided corporations access to capital. Additionally, credit spreads currently are indicating there are no credit issues forthcoming. For example, both investment grade and high yield corporate bond credit spreads are trading tighter than their long-term averages and show no sign of stress. Hence, our forecast is for bond yields to remain rangebound until the Fed becomes less accommodative and begins to taper bond purchases, which we believe will occur in November or December. Therefore, we reiterate that we expect the ten-year Treasury to remain below 1.50% until tapering begins and moving up to 1.50% to 1.75% range by year-end.

How does our forecast impact portfolio income?

Assuming rates move to the top-end of our trading range, investors still cannot depend on a predominately fixed income portfolio to generate enough income to sustain their lifestyle in the sustain and distribute phases of their life. For example, a million-dollar portfolio of fixed income that yielded 1.75% would only generate $17,500 per year. Given the limitations of an all-fixed income portfolio, we have recommended that investors use a combination of equities and fixed income to meet their income needs. However, with the ten-year treasury yielding 1.22% and the dividend yield on the S&P 500 yielding 1.34%, there will still be an income shortfall unless equities also have sufficient price appreciation and can be sold to meet income needs. Therefore, investors must find alternative ways to increase income.

Using Covered Calls: How to collect additional income using equities that you already own.

An alternative means of potentially generating income is to use the equity portion of the balanced portfolio mentioned above to supplement the coupon distributions from fixed income securities: the dividend/income payments from equities and any capital appreciation by implementing a covered call strategy. A covered call option strategy uses equities that the investor already owns to generate additional income by selling the right for a third-party to purchase the equity security or a basket of equity securities at a pre-determined price (strike price) by a specified date (expiration date) in exchange for a fee (option premium) that is paid to the investor. The third-party is under no obligation to purchase the equity security or basket of equities from the investor but has the option to purchase if the security or securities reach the strike price prior to or by the expiration date. The investor collects the option premium which becomes incremental income to the traditional income streams mentioned previously for a balanced portfolio regardless of whether the third-party exercises the option to purchase the equity security or basket of equities. We recognize this is a complicated concept to explain, so if you have further questions, your Financial Advisor can help explain this further.

The risk that the investor faces is the potential forfeiture of the equity security or basket of equities if the third-party decides to exercise the option to purchase the security. Under this scenario the investor loses the upside appreciation potential of the equity security and only collects the premium. Therefore, we believe it is important to implement this strategy when the expectation is for the market to trade within a narrow range.

Conclusion:

We do not believe bond yields are going to rise as much as originally expected this year, leaving investors to look for alternatives to generate income, in our opinion. While we continue to prefer equities over fixed income, there are inherent risks that come with being overly dependent on them to help supplement the income from the fixed income portion of the balanced portfolio. Therefore, we have recently implemented a covered call strategy in all balanced portfolios as we seek to increase the portfolios’ income and help clients in the sustain and distribute phases of their investment journey.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

In a rising interest rate environment, the value of fixed-income securities generally declines.

Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

A covered call refers to a financial transaction in which the investor selling call options owns an equivalent amount of the underlying security. To execute this an investor holding a long position in an asset then writes (sells) call options on that same asset to generate an income stream. The investor’s long position in the asset is the “cover” because it means the seller can deliver the shares if the buyer of the call option chooses to exercise.

A basis point is a unit that is equal to 1/100th of 1%, and is used to denote the change in a financial instrument. The basis point is commonly used for calculating changes in interest rates, equity indexes and the yield of a fixed-income security. (bps = 1/100th of 1%)

High-yield securities (including junk bonds) are subject to greater risk of loss of principal and interest, including default risk, than higher-rated securities.

Index Definitions:

Standard & Poor’s (S&P) 500 Index TR USD (Large Cap) measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2021 RiverFront Investment Group. All Rights Reserved. ID 1727344