By Kevin Nicholson, CFA, Global Fixed Income Co-CIO, Co-Head of Investment Committee

SUMMARY

- We believe Jackson Hole may serve as the two-minute warning for the Fed to announce the tapering its Quantitative Easing (QE) purchases.

- The US has a supply issue and not a demand issue, and just needs time for them to balance out, in our view.

- We expect the 10-year Treasury to finish the year in the 1.50%-1.75% range and equity markets to continue to grind higher.

What Asset Tapering Means for Markets

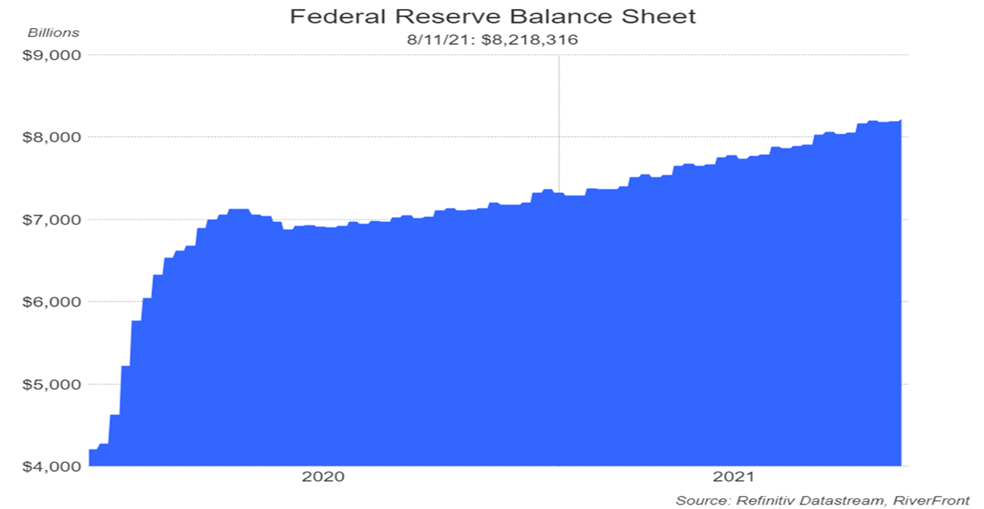

The Jackson Hole Economic Symposium begins on August 26th and the three-day event may serve as one of the most important policy events of the year. The Federal Reserve (Fed) will elaborate on its plan for meeting its dual mandate to maximize employment and to provide stable prices by keeping inflation around 2% over time. Since the onset of the pandemic, the Fed has been the backstop for the economy. Their creation of emergency facilities during the early days of the pandemic has helped to keep the economy from repeating the 2008 Great Financial Crisis. To that end, they have added over $4 trillion to their balance sheet since March 4, 2020, buying bonds and thus keeping long-term interest rates low. The Fed’s balance sheet reached an all-time high recently, totaling $8.2 trillion (see chart below). However, with unemployment approaching 5% and inflation near 3.5% as measured by Core PCE, Jackson Hole may serve as the ‘two-minute warning’ for the Fed to announce that it is slowing, or ‘tapering’ as the Fed calls it, the size of its bond purchasing program – known as Quantitative Easing (QE). Importantly, ‘tapering asset purchases’ is still supportive of bond prices and adds to overall liquidity.

Past performance is no guarantee of future results. Shown for illustrative purposes. Not indicative of RiverFront portfolio performance.

Examining the Fed’s Dual Mandate

Employment:

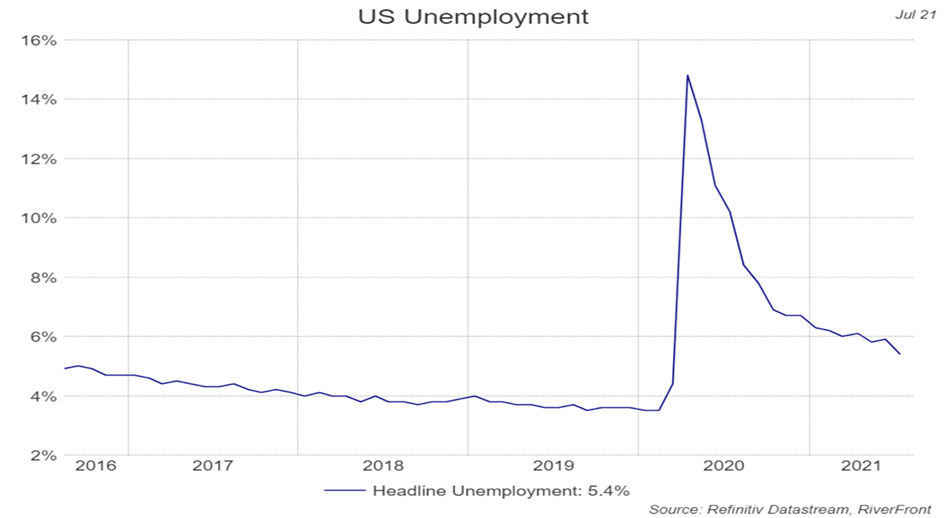

The recent strength in the labor market is making it harder to argue that the Fed is not well on its way to meeting its employment mandate. Non-farm payroll monthly additions have averaged nearly 617,000 per month thus far this year, with June and July averaging 940,500. The momentum is building and as the extended unemployment benefits expire on September 6th, more workers should enter the workforce. We think this will help to alleviate the labor supply shortage.

Shown for illustrative purposes. Not indicative of RiverFront portfolio performance.

Inflation:

The Fed has projected that inflation will be transitory until the supply-chain is back fully online. Currently core PCE is at 3.5% and headline inflation as measured by CPI is at 5.4%. Given that the Fed has undershot its target for so long, it has stated a willingness to let inflation run hot for short periods of time. Here at RiverFront, we acknowledge that different parts of the economy will experience periodic bouts of inflation over the next 6-9 months. However, we agree with the Fed’s view that that the current rate of inflation will subside once temporary COVID related supply disruptions are alleviated.

Fed Outlook: Timing of the Taper

The actions taken by the Fed at the onset of the pandemic were meant to lend support to an economy that was shutting down. Through QE the Fed has driven down interest rates supporting both bank lending and consumer demand. By combining monetary stimulus with fiscal stimulus in the form of transfer payments (stimulus checks), policymakers have helped engineer a historic rebound in the US economy. It is for this reason the US has a supply issue and not a demand issue. We believe a tapering of QE would help to rebalance the supply and demand dynamic.

The Fed has stated many times that it was going to give markets plenty of lead time prior to tapering its QE purchases. Following guidance at Jackson Hole, we believe that the Fed will formally announce its plans to taper at the September FOMC meeting and start tapering in November. The two-month grace-period would honor the Fed’s intent of giving the markets ample notice prior to tapering, in our opinion.

What does tapering mean for markets?

Once tapering begins we expect bond yields to rise. For context, we think the ten-year Treasury yield (1.26% as of last Friday) will finish the year in the 1.50% -1.75% range, moving back towards the higher levels seen in March of this year. Since rates hikes are not expected until late 2022/early 2023, continued improvement in earnings should allow equity markets to grind higher. We believe gradual tapering will allow time for the supply of goods and labor to catch up with demand mitigating inflation worries. If yields on the 10-year Treasury remain below 2%, we think the equity market will enjoy a ‘goldilocks’ environment with growth ‘hot enough’ to drive earnings, but ‘not so hot’ to cause a significant rise in interest rates. Therefore, we continue to position our asset allocation portfolios to favor stocks over bonds.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

In a rising interest rate environment, the value of fixed-income securities generally declines.

When referring to being “overweight” or “underweight” relative to a market or asset class, RiverFront is referring to our current portfolios’ weightings compared to the composite benchmarks for each portfolio. Asset class weighting discussion refers to our Advantage portfolios. For more information on our other portfolios, please visit www.riverfrontig.com or contact your Financial Advisor.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2021 RiverFront Investment Group. All Rights Reserved. ID 1798873