By: Nick Codola, CFA, CAIA

All investors have been spoon-fed on the 60/40 as THE balanced portfolio, and since the early ‘80s that has been true. But what happens when the interplay between stocks and bonds breakdown? What happens when the beloved 60/40 stumbles? Enter ‘Boomer Candies’.

The playful name refers to a group of ETFs whose explosive growth and popularity have been driven by Baby Boomers. You know Baby Boomers, they are the generation who control an estimated 54% of the stock market wealth (Fed Reserve). But why the need for these ETFs? Well, since the early ‘80s, bonds have been in a bull market as falling yields have acted like performance enhancing drugs (PEDs), fueling fantastic returns. However, just like anyone using PEDs for a prolonged period of time, bonds are now paying the piper now for their jaw-dropping run.

The low interest rate environment of the last decade coupled with the rapid rate hikes since ’22 have created a perfect storm to wreck the beloved 60/40. Bonds lost much of their income generation capabilities from low yields, their prices got crippled in the rate hikes, and their correlations to the S&P have significantly risen. Below are the Bloomberg US Aggregate Bond (AGG), the 20+ Year Treasury Bond Index (TLT) and Small-Cap Index (IJR) index ETF’s correlations to the S&P 500 over a one and 15-year period.

One Year Correlations

Data from Morningstar Direct as of 6.30.24

15 Year Correlations

Data from Morningstar Direct as of 6.30.24

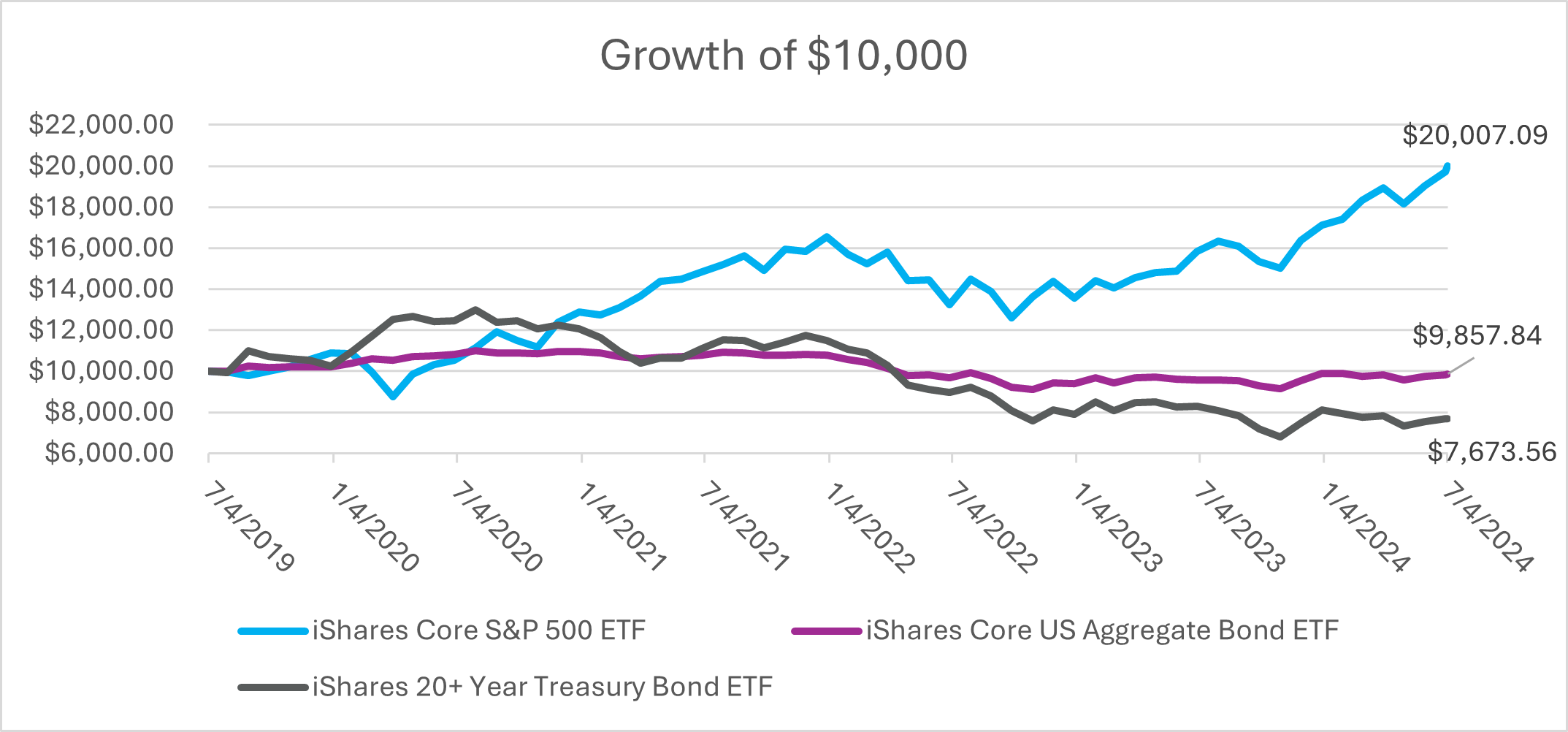

So, bonds have lost much of their income producing capabilities, they’re not as diversifying, and, as seen below, over the last five years, both AGG and TLT have annualized a negative return!

Data from Morningstar as of 7.4.24.

‘Boomer Candies’ provide an alternative to bonds which have lost their luster. These ‘candies’ help transform equities – which boast strong returns but also a lot of volatility and drawdown risk – into something more palatable for the retiree or soon to be retired. By using these products, investors can obtain income, and are afforded some form of buffer against an equity drawdown while still participating in some of the market’s upside. Although their returns are handicapped, the returns have nonetheless been superior to bonds which had a negative return over the last five years. By reducing volatility and max drawdowns, these financial sweet treats seemingly make equity risk more palatable for Boomers, helping them weather the equity market hiccups and stay invested for the long-term. By providing downside buffers, it also reduces a retiree’s portfolio withdrawal timing and horizon risk—the risk of withdrawing funds at an inopportune time which impairs their future prospects. As Mary Poppins said, ‘A spoonful of sugar helps the medicine go down.’

Running with the candy theme, there are a couple of candy types and each of them have a couple of ‘flavors’ to choose from.

- Buffered / Structured / Hedged Equity strategies: these strategies use options to transform an underlying equity index to have lower volatility and a modicum of downside buffer in exchange for surrendering a portion of the upside.

- Covered Call Strategies: these products harvest the volatility of the equity markets to generate a synthetic coupon payment so investors can have partial equity market participation and generate income too. There are a number of ways these strategies create a covered call strategy on an index, the most popular are: 1) they replicate an index, like the S&P 500, by buying the constituent stocks of the index at the appropriate weights and sell an out of the money call on the index. 2) The strategy could replicate the index but sell out of the money calls on the individual stocks. 3) The strategy might buy an index ETF, like IVV, and sell calls on that ETF. 4) The strategy may use futures on the S&P 500 and sell calls on the index. How ever they choose to run the strategy, if the ETF managers are clever with their option/future usage and ETF structure, these distributions can also be tax advantaged vs a straight dividend! With some of these strategies’ all-in distribution in the 6-10+% range, they help solve the issue of income sourcing for those retirees actively receiving distributions.

Sounds too good to be true? Well, it isn’t all sugar and rainbows. Just like candy, consuming too many of these strategies can create a sugar high and investors should be wary of developing cavities. It is paramount for the advisor and end client to understand how they work. All these strategies are more complicated than the underlying index they are built off of, but they have the same return drivers as the underlying indexes– if stocks go down, these ‘candies’ will feel it. The derivatives built around the index merely help to reduce the complexity of predicting the return over their intended timeframe, i.e. the number of outcomes possible for the fund.

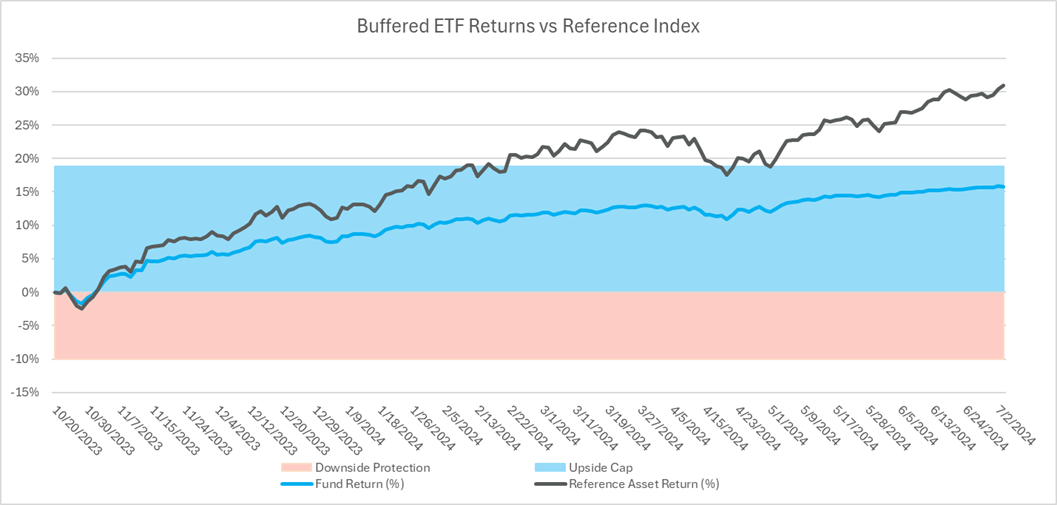

To bring the discussion into more concrete terms, the graph below is First Trust’s FT Vest U.S. Equity Buffer ETF (FOCT) constructed to buffer the first 10% of the S&P 500’s decline, but participate in the first 19% of the S&P’s rally over a 12-month time frame. Should the market drawdown 30%, its buffer should mitigate the first 10% decline, but it will fully participate in the further 20%. It also has upside risk because if the market is up 30% it will only be up 19%. Moreover, because it was built for a 12mo period, it also won’t accrue all the return until the end of the period. That means, it can deviate within that period.

If the S&P drew down 5% in the first month of the above structured product’s existence, on paper, this product should be down 0%. In reality, this ETF will be down a couple of percentage points because there is a chance that the market could keep going down in the next 11mo. If that should not be the case, and the S&P maintains that -5% return for the next 11 months, the Boomer Candy should post a positive return over that timeframe! We can see the interplay of these dynamics in the chart below. Note that even though the reference asset is up 30% since October, and well above the cap, the fund is only up around 16%. Moreover, notice how at the start of the time frame, the S&P had a negative return, and the fund’s return was negative, even though it was in its ‘downside buffer’ area.

Data from Morningstar and Bloomberg as of 7.4.2024

Turning our attention to the other type of ‘Boomer Candy’– covered call strategies, the returns in a down market will be the return of the market less the derivative income generated, and on the upside, it should be some fraction of the market’s return plus the income generated. However, again, intra-period returns will vary – if the S&P rallies and is up 2% in a day, the covered call strategies may only be up 0.5% because the call options sold to generate that income will reduce its price appreciation. Similarly, if the S&P is down 2% on a day, the covered call strategy will be down 2% on a price return basis, but on a total return basis it should be down less than 2% because the income generated will offset some of the losses.

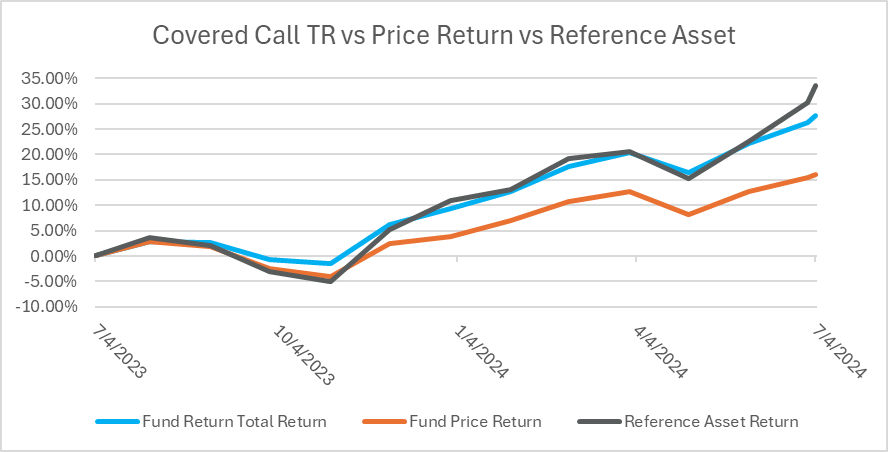

Nonetheless, if the end investor only looks at the price of the security, they will think they have been duped! They will feel doubly robbed in a scenario where the ETF rehedges the calls that night and if the market rallies the next day, the fund will lag! That can be visualized in the chart below, notice during the market sell off, the price return mirrored the reference asset sell off, but the total return of the fund was significantly better. However, as the market rallied, the fund lagged because the covered calls capped the upside.

It is always important to look at the covered call strategies both on a price-return and a total return basis to see performance of both the underlying strategy, the income overlay, and the interplay of the two. That way, an investor learns how much the income generated has dampened market movements and how much return they are exchanging for those distributions. The difference between the blue and orange line underscores the importance of the income generated by the derivatives. Below is a JP Morgan’s JPMorgan Nasdaq Equity Premium Income ETF (JEPQ) which runs a covered call strategy on the Nasdaq 100 Index. I broke out the return of the fund both on a total return basis and looking only at the price return of the asset to highlight the return derived from derivative income.

Data from Morningstar and Bloomberg as of 7.4.24

So, when considering adding some of these candies into a portfolio, remember while the betas—the absolute return movements in comparison to the reference index—of the ‘boomer candy’ strategies might be lower than the broad equity markets they are built from, the correlations are still high. That means, anything that hurts the ‘Boomer Candy’s’ reference index will hurt these ETFs and vice-versa. The degree and scale of that move is all that has been changed.

Just like eating a bunch of different candies might diversify the flavor, the underlying risks are still the same – cavities. At the risk of over doing the analogy, investors should continue to brush their teeth –rebalancing portfolios. Moreover, for those investors in search of assets which diversify and bring uncorrelated returns to a portfolio, they should explore other assets like liquid alternatives –vegetables. Although veggies do not have the same allure as candies, they do provide essential nutrients.

For more news, information, and analysis, visit the ETF Strategist Channel.

Orion Portfolio Solutions, LLC d/b/a Brinker Capital Investments (“OPS”) a registered investment advisor.

The views expressed herein are exclusively those of OPS, a registered Investment Advisor, and are not meant as investment advice and are subject to change. No part of this report may be reproduced in any manner without the express written permission of OPS. Information contained herein is derived from sources we believe to be reliable, however, we do not represent that this information is complete or accurate and it should not be relied upon as such. This information is prepared for general information only. It does not have regard to the specific investment objectives, financial situation, and the particular needs of any specific person. You should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed here and should understand that statements regarding future prospects may not be realized. You should note that security values may fluctuate, and that each security’s price or value may rise or fall. Accordingly, investors may receive back less than originally invested. Past performance is not a guide to future performance. Investing in any security involves certain systematic risks including, but not limited to, market risk, interest-rate risk, inflation risk, and event risk. These risks are in addition to any unsystematic risks associated with particular investment styles or strategies.

An index is an unmanaged group of stocks considered to be representative of different segments of the stock market in general. You cannot invest directly in an index. The S&P 500 Index is an unmanaged composite of 500-large capitalization companies. This index is widely used by professional investors as a performance benchmark for large-cap stocks.

Beta (β) is the second letter of the Greek alphabet used in finance to denote the volatility or systematic risk of a security or portfolio compared to the market, usually the S&P 500 which has a beta of 1.0. Stocks with betas higher than 1.0 are interpreted as more volatile than the S&P 500.

1786-BCI-7/19/2024