By Kevin Nicholson, CFA, Global Fixed Income CIO, Co-Head of Investment Committee

SUMMARY

- ‘Don’t Fight the Fed’: Fed hawkish…but Treasury market disagrees.

- ‘Don’t Fight the Trend’: Improving with the hopes of a softer landing.

- ‘Beware of the Crowd at Extremes’: Neutral and searching for direction.

The calendar has flipped to a new year, but our Three Tactical Rules are still fighting the demons of 2022: a Federal Reserve determined to fight inflation, a trend that continues to fall, and a crowd that hangs out near extremes. While the demons remain, progress has been made and the tactical rules of “Don’t Fight the Fed”, “Don’t Fight the Trend”, and “Beware of the Crowd at Extremes” are trending towards a more neutral portfolio positioning, in our view.

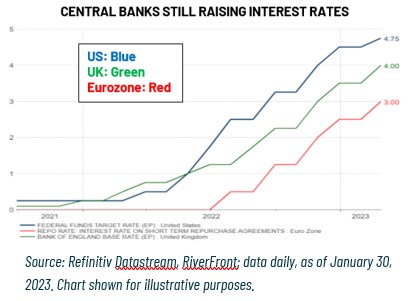

‘Don’t Fight the Fed’: Red Light – Fed hawkish, but Treasury Market Disagrees.

The Fed raised interest rates at the eighth consecutive meeting on February 1, 2023, moving the target fed funds range to between 4.50% and 4.75% (see blue line in chart, below). Market expectations are for the Fed to end its interest rate hiking campaign after the May meeting, as recent economic data has indicated that the economy is slowing with one exception: a strong labor market. If market expectations prove correct, the terminal fed funds rate will be 5.125%, in line with the Fed’s forecast at its December meeting. Despite the Fed having raised rates nearly five percentage points since March 2022, core Personal Consumption Expenditures (PCE) inflation remains at 4.4% year-over-year, well above the Fed’s preferred target of 2.00%.

The Fed has been insistent that it would not cut interest rates upon reaching the terminal fed funds rate; however, it appears the Treasury market has not gotten the memo. Long-term interest rates have fallen since October, as investors anticipated slower growth and the rising probability of a recession due to the Fed over-tightening monetary policy. While Treasury investors may be proven right eventually, we believe that this view is premature given the strong labor market and an unemployment rate of 3.4%, the lowest rate since May 1969, according to the White House. A strong labor market can give consumers confidence to spend and thus reverse the progress the Fed has had in

bringing headline inflation down from its June 2022 high of 9.1%, in our opinion. The Fed is concerned that this dynamic will force it to have to do more later if it does not stay the course, hence the need for further hikes, albeit at a slower pace.

Internationally, the Bank of England (BOE) and European Central Bank (ECB) have been actively fighting inflation as well. The central banks have raised interest rates significantly, but at different paces relative to each other and the Fed. The BOE has raised interest rates over the last 14 months by 3.9%, while the ECB has raised rates by 3% in the last 8 months and has signaled for additional rate increases. The BOE on the other hand, is getting closer to the end of its rate hiking campaign. Regardless of the pace of rate hikes, as shown in the chart above, major central banks are not on the side of investors as they attempt to contain inflation, in our view. While headline inflation has shown signs of slowing globally, the fight is not over. Thus investors who chose to purchase longer-dated maturities in the bond market are fighting central banks, and this is a mistake, in our opinion. For stock investors, central banks’ continuing to hike will likely continue to be a headwind.

Don’t Fight the Trend: Neutral – Improving with the Hopes of a Softer Landing.

The S&P 500’s trend is currently falling at a 12% annualized rate, which sounds like the broken record of 2022 (see chart, right). However, with the Fed getting closer to the end of its interest rate hiking cycle, there may be light at the end of the tunnel. The S&P 500 has recently broken above the 200-day moving average and has stayed there for 12 trading days, indicating improvement in the trend, in our opinion. If the S&P stays at its current level, the trend will turn positive in early March. In our view, a positive trend increases the odds of having positive returns over the subsequent three months dramatically.

Internationally, the trend of the MSCI ACWI ex US is falling at an annualized rate of just 6% (see chart, right). After prolonged weakness, the trend for international stocks is flattening faster than the US. At current levels, the international trend will turn positive by the end of February, bolstering the odds for positive returns over the subsequent three-month period, in our view. Given that both the domestic and international trends are improving and could turn positive in Q1, we believe the trend is still not an investor’s ‘friend’ yet but is becoming a closer acquaintance.

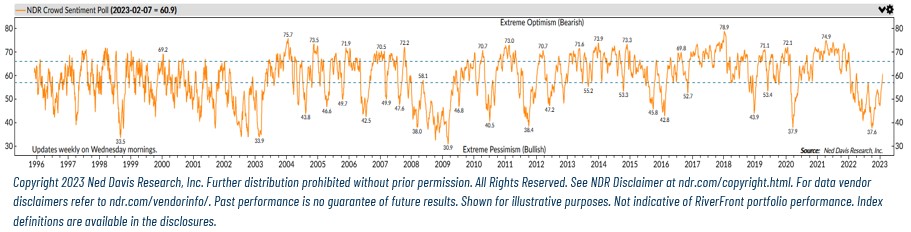

Beware of the Crowd at Extremes: Neutral and Searching for Direction.

We regard Crowd Sentiment as the contrary indicator of the Three Tactical Rules. Over the last year, the crowd has experienced highs and lows as investors attempted to handicap and navigate the evolving monetary policy landscape. The chart below shows a measure of investor sentiment calculated by Ned Davis Research. When the line is high it shows extreme optimism, and when it is low, extreme pessimism. This is our preferred way to measure investor psychology.

Recently, the crowd moved out of the extreme pessimism zone into neutral for the first time since April 2022, according to Ned Davis Research. The crowd moving to neutral does not warrant a change in portfolio positioning, in our opinion, as we do not believe we are at the types of optimistic or pessimistic extremes that would justify such moves. On its own, the crowd is not providing much of a signal, but when combined with an improving trend, the odds of a positive return over the next three months improves significantly in our model.

Conclusion:

Today, our three tactical rules of “Don’t Fight the Fed”, “Don’t Fight the Trend”, and “Beware of the Crowd at Extremes” are collectively sending a neutral signal, in our view. However, despite the Fed taking a hawkish tone, the improving trend and neutral crowd are on the verge of shifting our tactical stance to more bullish. Given that tactical asset allocation is tough to time, we like to ‘skate to where the puck is going’, not to where it is currently (to use a hockey euphemism). Given our view of an improving tactical landscape, our longer horizon portfolios are slightly ‘overweight’ positioning relative to their benchmarks, while in our shorter horizon portfolios we are waiting for further confirmation.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Important Disclosure Information:

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

All charts shown for illustrative purposes only. Technical analysis is based on the study of historical price movements and past trend patterns. There are no assurances that movements or trends can or will be duplicated in the future.

Ned Davis Research (NDR) is a global provider of independent investment research, solutions and tools. Founded in 1980, NDR helps clients around the world make objective investment decisions.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

In general, the bond market is volatile, and fixed income securities carry interest rate risk. (As interest rates rise, bond prices usually fall, and vice versa). This effect is usually more pronounced for longer-term securities). Fixed income securities also carry inflation risk, liquidity risk, call risk and credit and default risks for both issuers and counterparties. Lower-quality fixed income securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer. Foreign investments involve greater risks than U.S. investments, and can decline significantly in response to adverse issuer, political, regulatory, market, and economic risks. Any fixed-income security sold or redeemed prior to maturity may be subject to loss.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below.

Changes in the value of foreign currencies compared to the U.S. dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the U.S. dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the U.S. and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-U.S. securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Index Definitions:

A Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

MSCI ACWI ex USA Index captures large and mid cap representation across approximately 22 of 23 developed markets (DM) countries (excluding the US) and approximately 25 emerging markets (EM) countries.

Definitions:

The Federal Reserve System (FRS) is the central bank of the United States. Often simply called the Fed, it is arguably the most powerful financial institution in the world. It was founded to provide the country with a safe, flexible, and stable monetary and financial system. The Fed has a board that is comprised of seven members. There are also 12 Federal Reserve banks with their own presidents that represent a separate district.

The 200-day moving average is a popular technical indicator which investors use to analyze price trends. It is simply a security’s average closing price over the last 200 days.

Personal consumption expenditures (PCE), also known as consumer spending, is a measure of the spending on goods and services by people of the United States. According to the Bureau of Economic Analysis (BEA), a U.S. government agency, PCE accounts for about two-thirds of domestic spending and is a significant driver of gross domestic product (GDP).

Gross domestic product (GDP) is the total monetary or market value of all the finished goods and services produced within a country’s borders in a specific time period. As a broad measure of overall domestic production, it functions as a comprehensive scorecard of a given country’s economic health.

The European Central Bank (ECB) is the central bank responsible for monetary policy of the European Union (EU) member countries that have adopted the euro currency. This currency union is known as the eurozone and currently includes 19 countries. The ECB’s primary objective is price stability in the euro area.

The Bank of England (BoE) is the central bank of the United Kingdom. The BoE oversees monetary policy and issues currency. It also regulates banks, financial firms, and payment systems. Like other central banks, the BoE may act as a lender of last resort in a financial crisis. The National Bureau of Economic Research (NBER) is a private, non-profit, non-partisan research organization with an aim is to promote a greater understanding of how the economy works. It disseminates economic research among public policymakers, business professionals, and the academic community.

Federal funds, often referred to as fed funds, are excess reserves that commercial banks and other financial institutions deposit at regional Federal Reserve banks; these funds can be lent, then, to other market participants with insufficient cash on hand to meet their lending and reserve needs. The loans are unsecured and are made at a relatively low interest rate, called the federal funds rate or overnight rate, as that is the period for which most such loans are made.

Don’t Fight the Fed – ‘Supportive’ means the Fed’s monetary policy regarding inflation and employment is in what we believe based on our analysis to be the investors’ best interest; ‘Against’ means the Fed’s monetary policy, in our view, is going against the investors’ best interest; ‘Neutral’ means the Fed’s monetary policy is neither supportive or against the investors’ best interest in our view. Don’t Fight the Trend – Terms correlate to the 200-day moving average as it relates to the equity indexes: ‘Positive’ means that the trend is rising, ‘Flat’ means the trend is flat, ‘Negative’ means the trend is falling. Beware the Crowd at Extremes – Terms correlate to the NDR Crowd Sentiment Poll and its measurement of Extreme Optimism (Bearish), Neutral, or Extreme Pessimism (Bullish).

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at riverfrontig.com and the Form ADV, Part 2A. Copyright ©2023 RiverFront Investment Group. All Rights Reserved. ID 2735923