In the 1970s the most dreaded word in economics was inflation. Fast forward to the present and many are wondering if we will ever see sustained inflation again. Given the unprecedented central bank intervention over the last twelve years, inflation has been remarkably subdued, indeed at times investors have fretted that the US was experiencing deflation. For years, the Fed has tried to reach its long- term goal of 2% inflation, to no avail. However, the Fed’s giant experiment has created inflation in other parts of the economy not captured by formal economic metrics such as the Consumer Price Index (CPI) and the Personal Consumption Expenditure Price Index (PCE) that tend to dampen inflation calculations.

CPI and PCE:

CPI and PCE are two baskets that economist use to measure inflation. CPI is produced by the Bureau of Labor Statistics (BLS), and PCE is produced by the Bureau of Economic Analysis (BEA). While both indices measure inflation, they differ in their calculation, weighting scheme, and scope.

CPI tracks the prices of thousands of goods consumed by urban consumers in the same proportions each month, while PCE measures the aggregate change in the goods and services that are actually consumed. The make-up of these two baskets (CPI and PCE) have biases that, in our opinion, cause inflation to be dampened by their methodologies. For instance, CPI does not account for health care costs that are covered by insurance, only those expenses that are paid directly by the consumer out of pocket, eliminating a good portion of the cost.

While PCE includes all components of health care costs, it introduces the ‘substitution impact’ of goods and services in its calculation. For example, when the price of potato chips increases, consumers can switch to cheaper pretzels. PCE captures this substitution effect, thus not garnering the full impact of the price increase of potato chips.

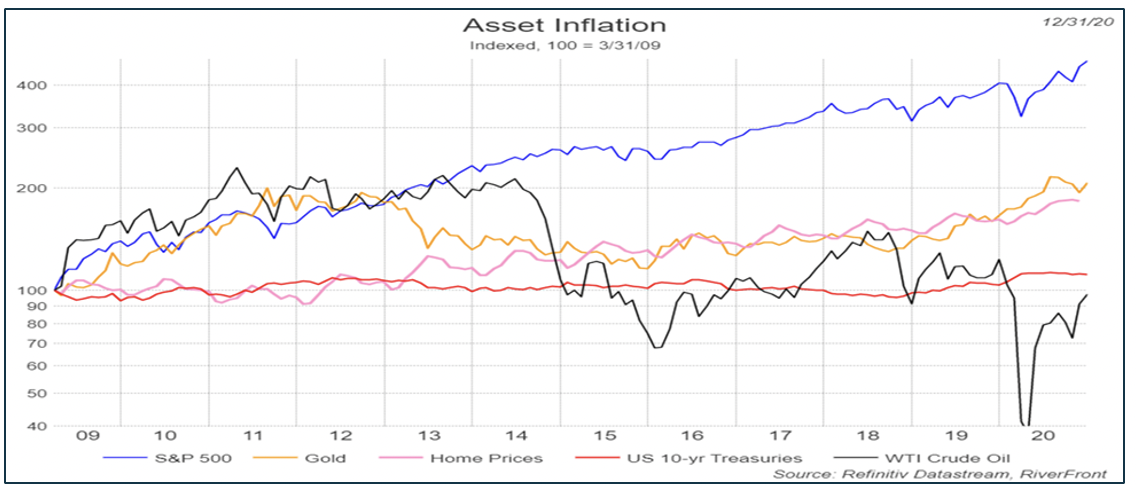

Asset Inflation:

Since the 2008 Great Recession, although ‘normal’ inflation as defined by CPI and PCE has been hard to sustain, the Fed’s easier monetary policies have created inflation in financial assets that are held by just 60% of Americans. The policies of the Federal Reserve were designed to drive short term interest rates to zero, and to provide excessive demand for bonds through outright purchases to drive their yields down as well. As a result of this policy, other financial assets such as stocks, gold, and real estate have experienced significant price increases. Since March 9, 2009 when the S&P 500 bottomed, the index is up 470% on a price basis, the price of Gold is up 207%, US 10-Year Treasuries are up 11%, and home prices are up 83% as of December 31, 2020. Conversely, the West Texas Intermediate (WTI) Crude Oil price was down 3% as of the same period (as shown in the following chart):

Disclosures: Past performance is no guarantee of future results. Shown for illustrative purposes. Not indicative of RiverFront portfolio performance. Index definitions are available in the disclosures.

This distinction is important because energy costs are a major input cost for goods and the depreciation of oil has helped keep a lid on goods inflation.

Inflation Drivers:

So, what are the drivers of inflation? We believe that there are two sides to inflation: Demand and Supply. On the demand side, one driver would be accelerating wages that would increase the spending power of consumers. On the supply side, one potential shock could be additional tariffs and/or trade quotas that would limit the amount of goods available.

Currently, the unemployment rate sits at 6.7%, well above what economist consider to be full employment. Additionally, the labor participation rate, the percentage of workers seeking employment, is 61.5% which is well below the 5-year high experienced in January 2020 of 63.4%. As more workers re-enter the workforce, hiring could increase without reducing the unemployment rate. Thus, an increasing labor participation rate has the potential to offset some of the improvements in the unemployment rate resulting from increased hiring (see Weekly View from 9/14/20: “Implications of a ‘Job-Light’ Recovery”). For wages to increase the economy needs to reach full employment and the demand for labor exceed its supply. In turn, rising wages allows consumers to have more discretionary income to purchase goods and services. Thus, demand increases and allows for potential price increases.

Supply and demand curves often act independently, so another path to increase inflation could come from the supply side. Supply has been strong for most goods and services as technological innovation has allowed companies to be more productive while not driving up costs, and globalization has dramatically increased low-cost supply. This has ultimately created excess supply in many industries, which has limited the amount of price increases that producers could pass on to the consumer. We believe this phenomenon has played a significant role in limiting the rise of inflation. However, if government stimulus can significantly increase demand and corporations hold back on increasing supply the sheer scarcity effect could induce inflation, in our view.

Conclusion:

There are number of paths that can be taken to increase inflation; however, we do not envision any of the paths developing enough to fear inflation becoming a problem in 2021. In our opinion, inflation is not a concern at present due to the number of workers still unemployed and the impact of the pandemic is still unsettled as the economy deals with selective lockdowns. Therefore, we believe that equity markets will continue to trade at elevated valuations as investors search for yield in a zero -interest rate environment with few alternatives. We view inflation as a potential issue to worry about in 2022 and beyond. However, if inflation expectations increase too much due to the economy rebounding faster than we forecast we will add Treasury Inflation Protected Securities to the portfolios to protect our client’s purchasing power.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

In a rising interest rate environment, the value of fixed-income securities generally declines.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

Treasury Inflation Protected Securities (TIPS) are Treasury securities that are indexed to inflation in an effort to protect investors from the negative effects of inflation. The principal value of TIPS is periodically adjusted according to the rate of inflation as measured by the Consumer Price Index (CPI), while the interest rate remains fixed. TIPS will decline in value when real interest rates rise. Portfolios that invest in TIPS are not guaranteed and will fluctuate in value.

Buying gold (bullion or coin) allows for a source of diversification for those sophisticated persons who wish to add precious metals to their portfolios and who are prepared to assume the risks inherent in the bullion market. Any bullion or coin purchase represents a transaction in a non-income-producing commodity and is highly speculative. Therefore, precious metals should not represent a significant portion of an individual’s portfolio.

West Texas Intermediate (WTI) is a crude oil that serves as one of the main global oil benchmarks. It is sourced primarily from Texas and is one of the highest quality oils in the world, which is easy to refine.

Index Definitions:

The Consumer Price Index (CPI) is a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them. Changes in the CPI are used to assess price changes associated with the cost of living. The CPI is one of the most frequently used statistics for identifying periods of inflation or deflation.

The PCE Price Index is the primary inflation index used by the U.S. Federal Reserve when making monetary policy decisions. Personal consumption expenditures (PCEs) are imputed household expenditures defined for a period of time.

Standard & Poor’s (S&P) 500 Index TR USD (Large Cap) measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2021 RiverFront Investment Group. All Rights Reserved. ID 1465508