(Au)our Monthly Newsletter

“So I just don’t think a lot of people have seen this. When’s the last time anyone here has seen interest rates up 2 years in a row and 6 or 7 times this year and 4 or 5 next? Nobody has seen that. Nobody has seen a lot of a lot of things that are happening today.”

– Gary Friedman, Restoration Hardware CEO March 2022 Earnings Call

In late 2019, as we were de-risking portfolios ahead of what turned out to be one of the top 10 downturns of our lifetime, we used a musical chairs analogy to describe the situation. We said we were grabbing our coats to go as we saw the number of chairs shrinking, knowing that whenever the music stopped, it would be painful. Now, with inflation running high and war likely to cause permanent changes in how nations cooperate economically, the central banks find themselves in an increasingly undesirable predicament with even fewer chairs at the party. The need for central banks to combat inflation with higher rates in the face of growing uncertainty adds credence to the idea we may be entering a far different period than experienced over the past few decades.

Destruction vs Disruption

Emotions have been running high this first quarter of 2022. The Russian invasion of Ukraine heightened pre-existing economic concerns about growing inflationary pressure and the awareness that interest rates would be rising.

Unsurprisingly, the rising tension has brought on higher levels of volatility. One day people want full risk exposure. The next they want completely out of the market. As we have expressed throughout our history, though, emotional responses to market swings are not the best way to protect and build lasting wealth.

We need to consider separately the (hopefully) short-term impact of war on the global economy and the longer-term potential disruption that the redefining of trade relationships brought on by war and increasing interest rates can cause.

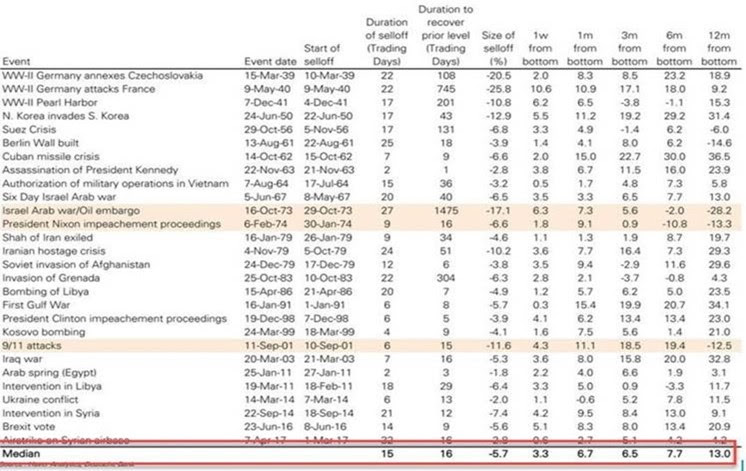

Global markets reacted quickly to Putin’s mind-numbingly destructive invasion of Ukraine, and as is typically seen with historical events, the markets partially recovered from the lows fairly quickly. We present a table below, produced by Mizuho Securities, showing past market-moving historical events, with their near- and intermediate-term impacts on equity prices (displayed in the chart as percent change from the bottom in various timeframes). In most cases, the markets recovered within months from the initial downward moves. However, in a few situations, the markets continued the downward trend for a year.

Whether the event’s market impact is short- or long-term might come down to whether the market perceives the event as a momentary (though harsh) period of destruction or as an event that will likely cause an ongoing period of disruption.

A destructive event, of course, will carry long-lasting implications for those directly involved. For example, even if the war ended today, Ukrainians face decades of rebuilding and many will carry the scars of war for life. But the regional impact of a destructive event does not always spread to the greater global economy.

On the other hand, we are defining disruptive events as those that interrupt the global economy’s current path with a new factor or phenomenon that permanently changes the direction of growth. The disruptive event acts like a jump ball in basketball, a reset where suddenly both teams must adjust to a new potential direction and tempo of play. We have discussed in past writings some signs the economic backdrop is changing, including a shifting trade environment after China’s takeover of Hong Kong and, recently, rising inflation and the scarcity of non-discretionary goods. With Russia’s aggression, we will need to add a changing energy supply and new East vs. West tensions to the mix.

For us, the trends of the past confirm that in most circumstances we must stay calm and be patient as we weather short-term destruction from war and increasing market volatility. However, in some instances, when the event brought a delineation between one global economic environment and another, past trends and market momentum become harder to trust given the changing landscape. We highlighted in the chart the few instances of this, such as the building of the Berlin Wall that marked the start of the cold war, the oil embargo of the 70’s, and the destruction of the World Trade Center towers on 9/11, as examples that brought about a more enduring and global change to economies. The current situation shares some characteristics of those events, as Russia and China expand their adversarial stance against the West. We maintain our focus on potential longer-term disruptions to the economy that may present new opportunities for profitable investing.

Rising Recession Risk

We are going to let the pictures do the talking to underscore our concern about the risk of recession. Below are four charts that we think highlight that growing risk.

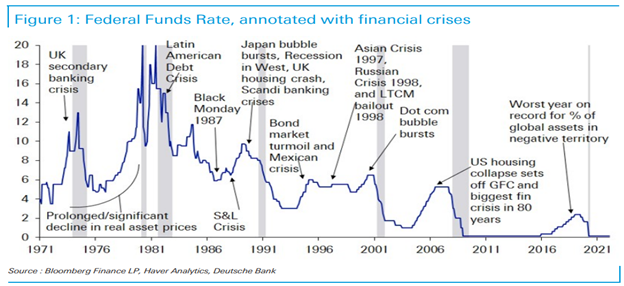

As the Federal Reserve starts raising interest rates, Deutsche Bank’s chart, below, makes the case that tightening cycles provide the backdrop for asset deflation (or busts). With financial leverage being high across the globe, as economic disruptions increase and monetary policies are tightened, the risk of a crisis increases.

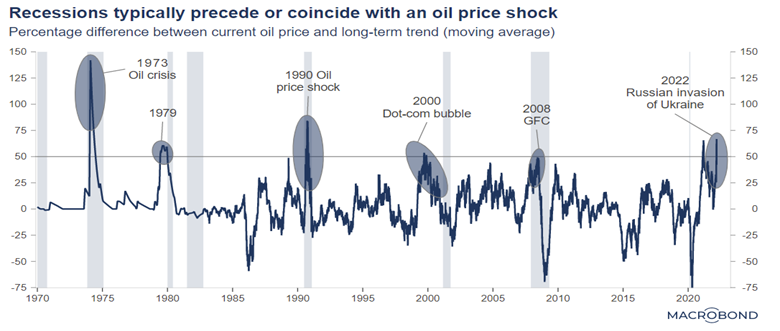

Even with aggressive investment in renewable energy, the world today is still highly dependent on fossil fuels, in particular, oil. The chart below shows how previous quick, upward movements in oil prices have coincided with recessions. History isn’t necessarily followed precisely, but we think its patterns deserve respectful consideration.

Consumer expectations are volatile and not a sound predictor of recessions, but with low unemployment and wages growing, it is interesting to see a rising nervousness among the population.

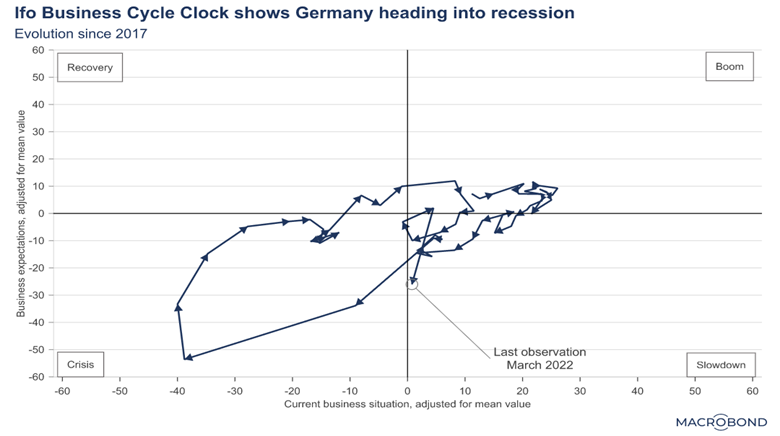

Germany, one of the larger developed economies, is also flashing warning signs. Its economy is slowing from very high levels, and future expectations are negative. The chart below shows the evolution of current and future economic expectations in Germany since 2017. They are moving into a precarious position.

Conclusions

Long-term averages of investment markets show a historically strong return after the impact of inflation, leading most to believe in a static “stay in the market and wait it out” approach. However, within those averages are periods encompassing wars, high inflation, and economic recessions that can test one’s resolve that the future could look anything like the past. In most cases, over the last 40 years of economic growth, the market recovered before market volatility brought one to the breaking point. Those few episodes we identified where the markets did not recover quickly were during periods of rising inflation. And that brings us to the present moment: this chance that we are today in one of the rarer but inevitable market shifts that takes longer to play out calls for, as suggested by our quantitative indicators, cautious positioning in Auour’s portfolios.

Best regards,

The Auour Investments Team

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal.

All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Auour Investments LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.