May’s Rebound

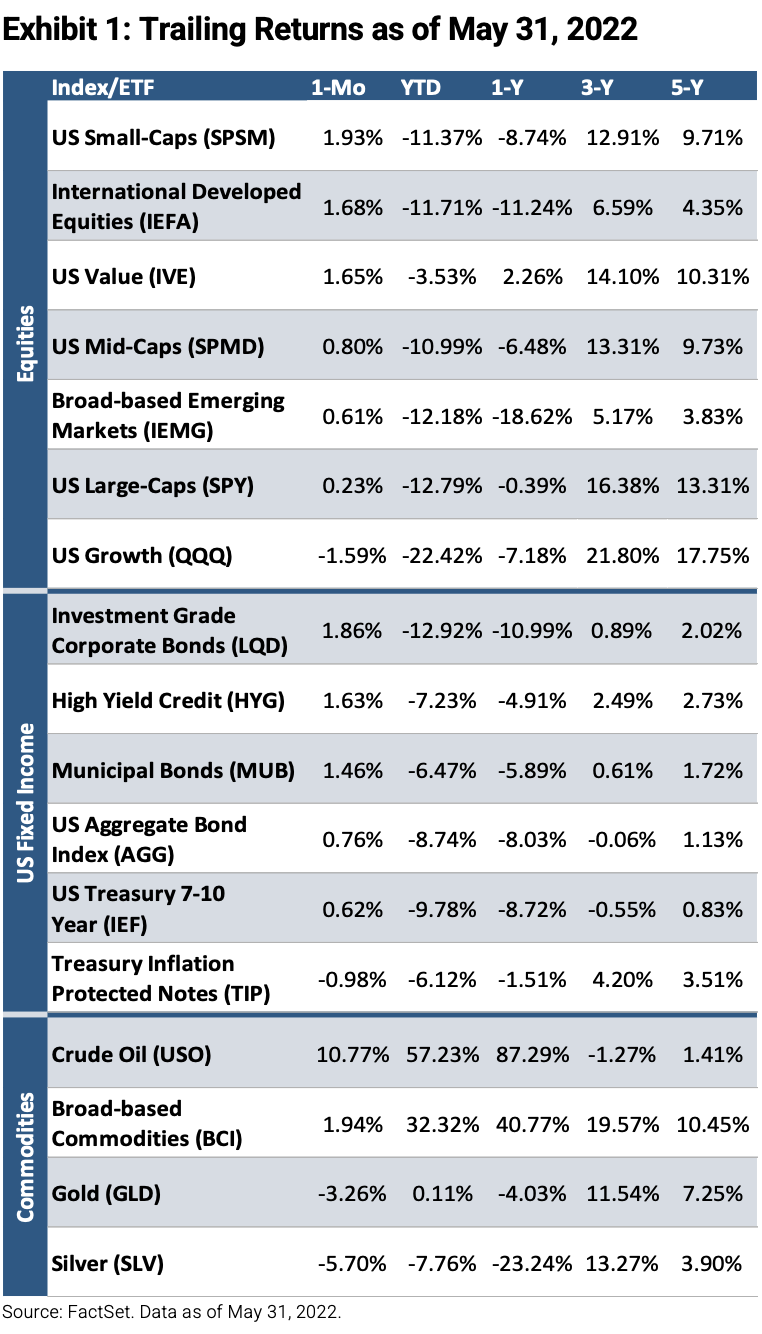

Despite negative returns in April and market turbulence throughout May, equities finished marginally higher for the month. US small-caps were amongst the best performers (+1.9%), followed by international developed equities (+1.7%) and US value (+1.7%). Bonds also delivered mostly positive returns as investment grade corporates were up 1.9%, high yield credits rose 1.6%, and municipal bonds gained 1.5%. Commodities produced mixed returns as crude oil and broad-based commodities rose (+10.8% and +1.9%, respectively) while gold and silver fell (-3.3% and -5.7%, respectively).

What’s Next for the Fed?

Earlier this month, the Federal Reserve raised interest rates by half of a percentage point. This marks the largest single rate hike in two decades as the Fed attempts to battle stubbornly high inflation. Members of the committee also outlined a plan to begin reducing its bond buying program starting on June 1st. As a result of the shift towards a more aggressive tightening policy, markets experienced volatility this month as recession fears mounted. Moreover, the Meeting Minutes released on May 25th suggest some officials remain united on the need for half percentage point increases at both the upcoming June and July meetings. However, other members have indicated the Fed may slow rate increases if monthly inflation readings continue downward, and even see a possible pause for rate increases in September.

Dividend and Value Strategies Outperform

As seen in the chart below, both dividend and value-oriented strategies led in May, posting gains from 2% to over 5%. The outperformance of these defensive plays can likely be attributed to heightened uncertainty amid concerns of tighter monetary policy and recession worries. Conversely, growth was the biggest laggard for the month and has underperformed significantly since the start of 2022 given its 21% decline.

Flirting with Bear Market Territory

A bear market can be defined as a decrease of approximately 20% from recent highs. Given the S&P 500’s peak on Monday, January 3rd, the index crossed this threshold on Friday, May 20th, but rebounded back above in the final hour of trading. This marked the seventh straight weekly loss for the S&P 500, its longest loss streak in decades. However, since May 20th, the index recovered losses and finished slightly up month over month. Economists attribute the rally to slowing but still elevated inflation measures and favorable earnings reports, which implies the sell-off may have been exaggerated.

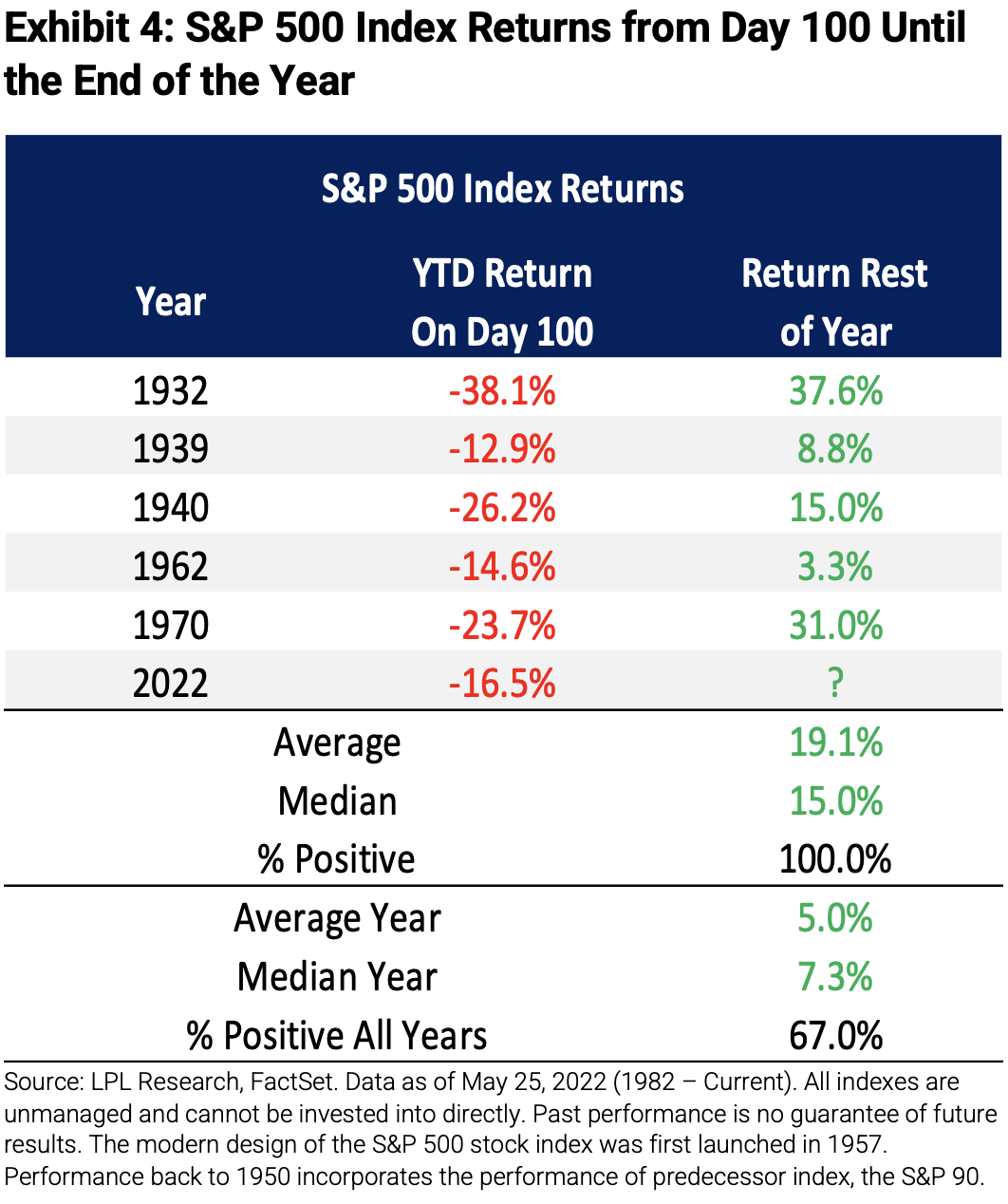

Will the S&P 500 Bounce Back this Year?

According to LPL Research, the previous 5 worst starts to a year measured by the performance of the S&P 500 were followed by greater returns for the remainder of each of those years. Additionally, while the average return calculated from the 100th day to year end across all years is 5%, the average gain across the same period of the last 5 worst starts is almost four times greater at 19.1%.

Stick with Short-Duration and Inflation Assets

Long-duration assets are experiencing a recession while there is a bull market for inflation-sensitive assets. In the current environment, it’s crucial to be globally diversified, own multiple factors, and utilize alternatives. It is important to hedge inflation risk as CPI readings may not return to their former trend line in the foreseeable future. Panic in the market may have also reached its peak as it often coincides with market bottoms. Regarding the Fed, we believe there is a high probability that we have seen peak Fed hawkishness and bearish sentiment.

Warranties & Disclaimers

There are no warranties implied. Past performance is not indicative of future results. Information presented herein is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and unless otherwise stated, are not guaranteed. The returns in this report are based on data from frequently used indices and ETFs. This information contained herein has been prepared by Astoria Portfolio Advisors LLC on the basis of publicly available information, internally developed data and other third-party sources believed to be reliable. Astoria Portfolio Advisors LLC has not sought to independently verify information obtained from public and third-party sources and makes no representations or warranties as to accuracy, completeness, or reliability of such information. Astoria Portfolio Advisors LLC is an SEC registered investment adviser located in New York. Astoria Portfolio Advisors LLC may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration requirements.