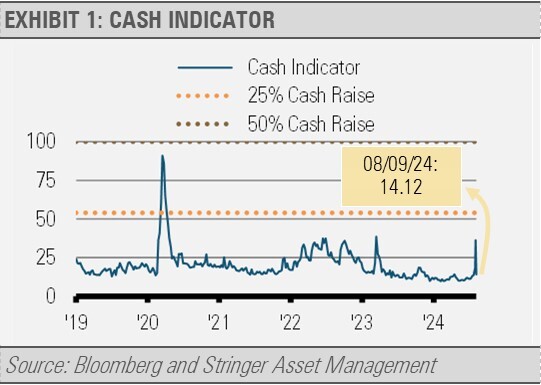

The Cash Indicator (CI) jumped higher based on recent market volatility, then quickly settled (exhibit 1). Though a jump in volatility like this is discomforting, it is to be expected given how complacent the financial markets have been.

Periods of exceptionally low volatility tend to be followed by a spike in volatility, which is a normal reaction. We have seen similar situations over the years, most recently in the spring of 2023. With the backdrop of persistent economic growth, the equity market quickly recovered.

Our framework for tracking economic growth or recession in real time tracks the progress of four different economic indicators inspired by the National Bureau of Economic Research, which is the group responsible for dating business cycles. This model continues to suggest economic growth.

Though the unemployment rate has ticked higher as jobs growth has slowed, real (inflation-adjusted) income growth and industrial production growth remain positive. In fact, both real income and industrial production recently reached all-time highs.

We can see the amount of money in the economy, as measured by M2, spike to above the pre-pandemic trend as measured both in absolute terms and relative to the size of the economy. The recent reversal of these trends eases the inflationary impulse.

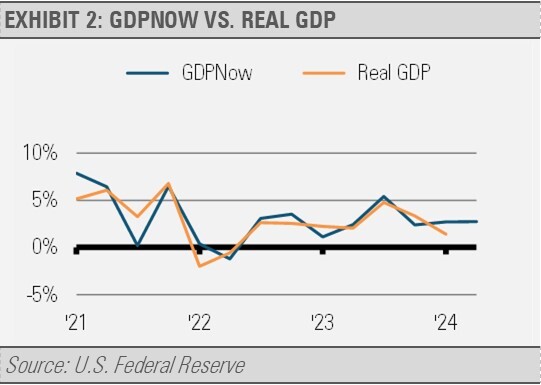

Combined, these data point to slow economic growth ahead. Meanwhile, the Atlanta Fed’s GDPNow model is forecasting a healthy 2.9% GDP growth for the current quarter (exhibit 2).

Especially with the constructive economic backdrop, periods like this may provide opportunities to buy quality assets. The market has been favoring our approach to anticipating U.S. Federal Reserve (Fed) rate cuts. Our focus on investment grade intermediate duration fixed income is working well. In addition, we utilized the recent equity market volatility to add to blue chip U.S. equities with downside protection as well as strong dividend payers.

In environments like this, we like to focus on risk management and make sure that we are deploying assets into quality investments. Given the recent equity market pullback, many of these companies are trading at more attractive valuations with business models that can better withstand economic turbulence.

We also maintain some defensive positions including dry powder to put to work should our leading indicators suggest the time is right for more cyclical tactical shifts.

Looking ahead, slower jobs growth and slowing inflation give the Fed more leeway to reduce short-term interest rates. The market is now pricing in at least 0.75% in rate cuts before the end of 2024, which would reduce short-term interest rates and money market yields by at least 0.75%.

We have positioned for these rate reductions by paring back our short-term interest rate exposure and increasing our allocations to the intermediate area, which locks in attractive current income and potentially benefits from capital appreciation as interest rates decline. We are expecting the potential for equity-like returns from our high-quality fixed income positions.

As the Fed began increasing short-term interest rates, assets in retail money market funds soared. With short-term interest rates much more attractive than in the recent past, we think that money market funds and short-term Treasuries deserve an allocation in investors’ portfolios. However, such a large move into money market funds over a short period of time suggests that investors may be over allocating to money market funds and T-Bills while perhaps not considering the implications and potential opportunity costs associated with holding such an overweight to them.

For example, while money market funds pay attractive yields today, the income provided by these funds will drop precipitously as soon as the Fed begins to lower interest rates. Conversely, allocations to investment grade intermediate fixed income are unlikely to see a significant reduction in current income when the Fed cuts rates. This positioning exhibits more income stability because these portfolios would have locked in today’s attractive rates for longer. Additionally, intermediate fixed income investors may also benefit from capital appreciation when the value of their bonds increase as interest rates fall.

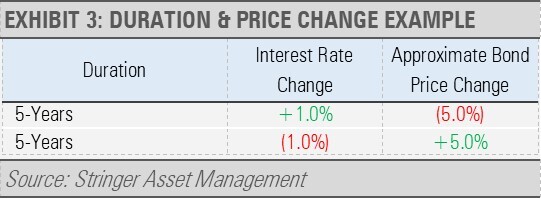

We can use duration of a bond or bond portfolio to illustrate this point (exhibit 3). Duration measures the sensitivity of a bond or bond portfolio to changes in the level of interest rates. In general, the value of shorter duration portfolios is less sensitive to changes while the value of longer-duration portfolios is more sensitive to changes in interest rates.

For example, a 1% increase or decrease in interest rates results in the price of a vanilla bond or a bond portfolio changing approximately 1% in the opposite direction for every year of duration. So, if a bond portfolio has a duration of 5 years and interest rates increase by 1%, the bond portfolio’s value will decline by approximately 5% in total. Conversely, if a bond portfolio has a duration of 5 years and interest rates fall by 1%, the price of the portfolio should increase by roughly 5%.

This gain would be in addition to the attractive current yields we are seeing. Note that changes in interest rates will not immediately impact the current income generated from a 5-year duration bond portfolio, only the price of the bond or bond portfolio will change.

INVESTMENT IMPLICATIONS

While holding assets in money market funds or T-Bills has its merits, our Three Layers of Risk Management framework leads us to additional opportunities that have the potential for attractive gains and principal protection.

Our work suggests that the investment grade fixed income space looks very attractive. As interest rates have risen and bond prices have fallen, we think core intermediate duration fixed income is set to offer attractive returns for years to come. Within that space, we favor defined maturity Treasury and corporate bond ETFs.

On the equity side, our allocations are tilted towards high quality U.S. and foreign equities that exhibit consistent earnings and low financial leverage as well as more defensive dividend payers.

In the alternative space, we allocate to equity option strategies that overlay U.S. blue-chip equities to either enhance current yield or offer downside protection.

Investors who are feeling more nervous can always adjust their allocation to one of our more conservative models.

CASH INDICATOR

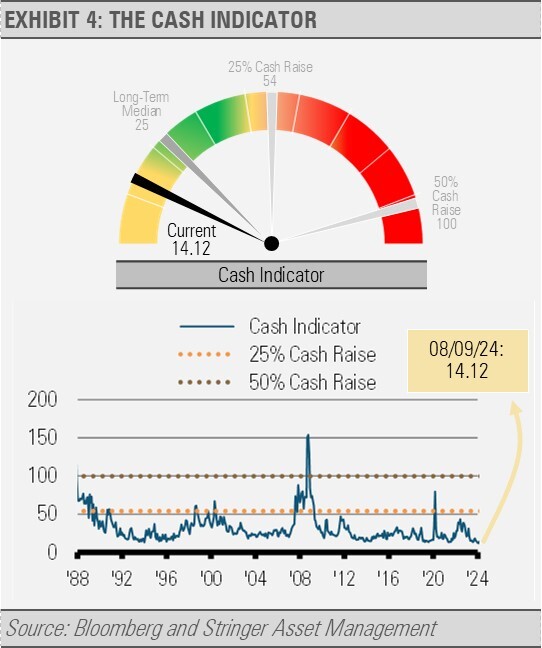

Despite recent volatility, the Cash Indicator is well below levels that would suggest that the markets are excessively fearful. Rather, we think that volatility like we are seeing simply reflects normalization. Excesses like the Yen carry trade deflating may temporarily disturb markets. Given the relatively positive economic backdrop, we see these bouts of volatility as opportunities to add to quality investments and have adjusted our allocations accordingly.

For more news, information, and analysis, visit the ETF Strategist Channel.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.