By Michael Paciotti, CFA

“Those who know don’t tell and those who tell don’t know.”

― Michael Lewis, Liar’s Poker: Rising Through the Wreckage on Wall Street

When you manage investment dollars for as long as we have, invariably you tend to develop a number of catchy sayings or phrases that embody a lesson that was learned at one point or another. One of our favorites is “the markets are always telling a story. Some choose not to listen.” It’s a lighthearted way of saying that the market often implies certain things by its price action or valuation. At the heart of this, the story being told, is quite important to developing an effective strategy for the medium term. Within this story is what that market currently believes based on the collective opinions of its participants.

What’s almost as important as recognizing the existence of the stories, is realizing that they are not always correct. In fact, quite the opposite. They are usually, at least initially, incorrect before winding their way to something more reasonable before ultimately finding the truth. This is normal market efficiency at work. Now, identifying what is 1) false but 2) widely believed to be true, can be a pretty profitable investment strategy. It essentially leads to something being mispriced.

Most stories, however, are rarely visibly false, yet believed by most. The combination does happen from time to time, usually in the presence of a great bubble or anti-bubble. These inflection points tend to draw out strong emotional responses. The great bubbles don’t form by one gigantic leap or miscalculation but rather by a series of seemingly logical steps taken to a completely unreasonable destination (another of our catchy sayings).

Otherwise, the mistake would be so obvious that it likely wouldn’t be believed by most and, as a result, end up being the consensus. But small errors taken in sequence are much harder to see.

Over the years there have been a few yarns that have been spun with great elegance that the incremental steps taken were tiny and hardly noticeable, but the destination was miles from anything reasonable. Top of mind is the internet bubble and all of the stories surrounding firms with no earnings. From that era one of my favorites was a narrative that suggested that certain telecom, media, and technology companies should not be valued by conventional valuation methodologies, bandwidth was the important metric. This of course was complete nonsense. While I’m sure bandwidth was important, this statement implies the more the better, despite earnings, cash flow valuations, everything else. The result was a market swimming in fiber optic cable and a lot of unprofitable firms. At some point, some unknown brave soul ventured to be so bold as to ask, “what the hell are we going to do with all of this cable?” This simple yet very astute observation at the appropriate time is usually enough for the lightbulb to go on and for investors to collectively head for the exits, as it did in this case, resulting in a wipe out for many.

Now, you might be asking why this is relevant, is there a story being told today that is a bit outlandish? There is. Not necessarily outlandish as much as contradictory. It’s hard to see, one of those small misstep types that lead you to some ridiculous place. The story today is the conflicting narratives among stocks and bonds with regards to the future path of rates, the condition of the economy and what happens to earnings. We’ll discuss this and more in this quarter’s Market Insights Liar’s Poker.

Why are stocks and bonds related?

Before we get into the disconnect, it’s important to understand the linkage that exists between stocks and bonds. The connection between stocks and bonds exists through interest rates, specifically the discount rate. In my 2q 2021 Market Insights The Trillion Dollar Staring Contest I wrote the following:

The connection between bonds and interest rates is hardly crystal clear, but less nebulous than the connection between stocks and interest rates. Simplistically, if I own a bond with a 5% coupon and an identical bond with a 2% coupon comes to market, which would be preferable, buying the 5% bond from me or taking the same risk and getting 2%? Naturally, you would prefer the 5% bond to the 2% bond and so would everyone else (all else being equal), making it more valuable (i.e., the price would appreciate). This simple example is commonly quantified in fixed income markets as duration, or the bond’s sensitivity to a change in interest rates. Typically, the longer the maturity, or the lower the yield, the greater the duration. Now, the wonky explanation…duration just simplifies the impact that changing discount rates have on a stream of cash flows, in this case a bond, into one easily interpreted number. This can be seen in the formula below.

While hardly obvious in the formula, the exponent in each term indicates that cash payments that are received later are more heavily discounted than those that occur sooner. That is, they are worth less today than near term cashflows. What would you prefer, $100 today or $100 ten years from now? Obviously $100 today. Think of this like the opposite of compound interest. Given this, bonds that return cash to the bondholder more quickly have a lower sensitivity to that discount rate, meaning if rates move up, you would prefer to own a 10-year coupon paying bond over a 10-year zero coupon bond. The coupon paying bond will decline by less with the upward move in interest rates, since it is paying you regular cashflows throughout the life of the bond.

Now, how does this pertain to stocks? Really through the same relationship. With stocks, like bonds, today’s value is just a discount of future cashflows. Let me make some substitutions.

Essentially, the formula is the same. Instead of discounting coupons for bonds we are discounting dividends for stocks. At maturity, a bond returns principal. While there is no specific maturity of a stock, we can assume a sales price. In the same manner that we calculate a present value for a bond, we can calculate it for a stock, or really anything with a future cashflow. Going back to the original question, how do interest rates impact stocks? Simple, through the discount rate. Lower rates equate to a higher present value (i.e., a higher current value of the stock), all else equal, just like higher rates result in a lower present value.

So where’s the disconnect?

To fully appreciate the story being told, we need to go back a few months to the dovish pivot by Fed Chair Jerome Powell in early December of 2023. At his post meeting press conference Fed Chair Powell suggested that not only were we witnessing an end to the near twenty-month rate hike cycle, but that it was very likely rates would be lower, perhaps meaningfully so, by the end of 2024. In short order, fixed income markets reacted, pricing in a series of rate cuts, seven to be precise, to the future path of interest rates. Equities simultaneously cheered the decision rallying by 16.58% over the next seven months, leading to the first of many disconnects. Seven rate cuts is a serious amount of policy easing, 175bps if done in 25bps increments.

While the reduction in the discount rate would be beneficial to longer duration assets like stocks, that presumes that earnings are unaffected. What sort of economic weakness would inspire the Fed to cut so aggressively? In the last 35 years there have been four instances where the Fed has cut rates by at least 175bps; the early 1990’s recession, the aftermath of the Internet Bubble, the Great Financial Crisis, and COVID. In each of those instances, earnings per share for the S&P 500 declined from peak to trough by -36.68%, -54.02%, -91.92% and -32.51%. It’s difficult to envision an environment where the Fed would step in so aggressively without some disruption to earnings.

Now, I began this article by saying bubbles form by a series of small missteps. This is in my opinion one of them. Taken alone, it’s not completely unreasonable to believe what I’m about to tell you. The first, the current Shiller PE is about 34x the last ten-year average real EPS, about double its historical average, and 50% above its average of the last 40 years. Overvalued? Yep. Frothy? A bit. But, what if I told you that in the last 140 years, we’ve seen a valuation above 30x in 106(occurred in 6% of environments) of those months and a valuation above 34 in 52 of them (occurred in 3% of environments)? Remote? Certainly. Statistically though, neither are even a two-sigma event. Given a sigma of two, we should see those events roughly one in every 44 outcomes. Definitely possible. In fact, over a century, probable.

Now, what if I also told you that earnings growth this year and next are expected to be quite robust? You might say that fits neatly with the current high valuations.Odds are, more often than not, you’d be correct. The market could be anticipating the robust earnings growth and reflecting it in the current price.

Now, what if I also told you that earnings growth this year and next are expected to be quite robust? You might say that fits neatly with the current high valuations.Odds are, more often than not, you’d be correct. The market could be anticipating the robust earnings growth and reflecting it in the current price.

The consensus (according to Standard & Poor’s) is for S&P 500 earnings to grow in 2024 from $192 per share to $218 or an increase of about 13% and then grow again in 2025 to $252 for a total gain of 31%. The average annual growth rate since 1988, is 6.11% per year in nominal terms. Is it completely unreasonable for earnings to grow at twice the average in any one or two years? Certainly not. A strong economic environment could easily produce robust earnings growth on a short-term basis.

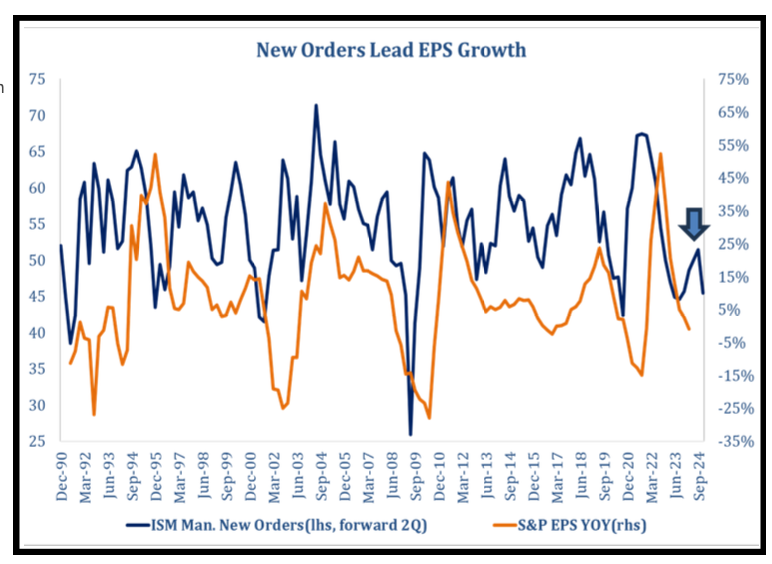

In fact, ISM New Orders tends to lead EPS growth by about 6 months. This is seen in the chart below. As we can see, earnings for the S&P should see a bump in the third and fourth quarters making this year’s consensus EPS growth even less of a stretch. Beyond that, it tends to get murky, suggesting that 2025 might be harder to reach than the 2024 consensus.

Now the punch line…Assuming all of this is accurate and 2024 remains strong, remind me again why the Fed would aggressively cut rates in this environment? As we saw historically, they have only cut this aggressively when economic growth is challenged, which is ultimately reflected in steep earnings declines. It doesn’t seem like earnings growth, at twice the near-term historical rate, fits with an aggressive rate cut narrative. The other thing to consider is inflation. Amidst such economic strength and aggressive rate cuts, how likely is it that inflation remains subdued at or near the Fed’s targets. Taken in isolation, none of these events are entirely unreasonable. When taken collectively, I fear we’ve marched ourselves one step at a time to an unreasonable place. That place being the expectation for both exceptionally strong economic and earnings growth, subdued inflation, met with aggressive stimulus. A perfect backdrop for stocks. Too perfect and ultimately unreasonable in my opinion.

But, how do we know stocks expect aggressive cuts?

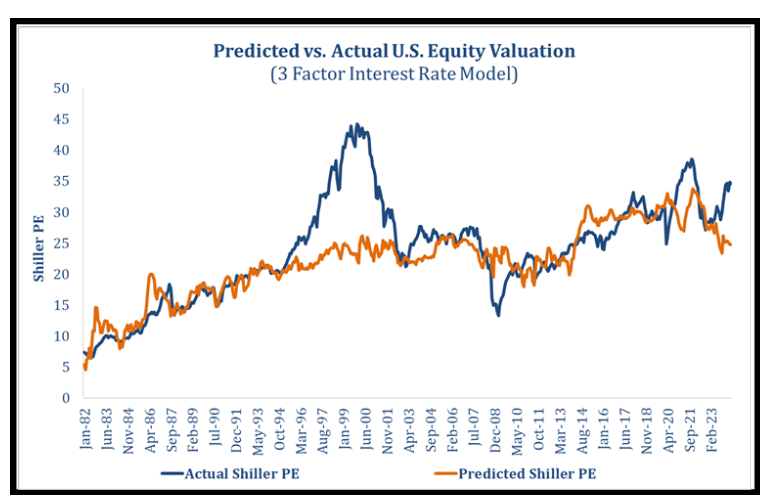

Now the last bit of evidence I’d like to offer brings rates and equity valuations together. The chart below is from one of our own models that we use to help predict the fair valuation of the equity market given the level of rates. Fair valuation is a bit of a misnomer as it implies normal expected returns and probabilities. In this case it’s more of what valuation is explained or supported by the current term structure. Being “fair” in this case does not imply normal future returns. It simply suggests where valuations should be given the level of rates and slope of the curve. Now all of that said the model currently suggests that the PE should be about 25x, lofty given historical standards. However, even when compared to that lofty estimate, equities are about 40% overvalued. Let me clearly state that we should not expect anything resembling a normal equity market return for any sustained period from this level.

Now, the interesting thing about this model is that we can easily observe various scenarios. As I mentioned, there are multiple moving parts here that involve the movement of yields across short, medium and longer maturities making this, in real life, probably not as straight forward as I will illustrate momentarily. But, there is good information content here. Let me pose the following question…. what level of rates would support the current valuation level (i.e. eliminate the over valuation)?If the 2y treasury yield, the instrument most correlated to Fed rate cuts, were to decline from 4.75% to about 3%.This would suggest that equity valuations, although high, can be explained by the current shape and level of the yield curve.

Coincidentally, this is 175bps or 7 rate cuts below current levels. While bonds have walked back the aggressive assumption, it appears as though equities have not gotten the memo. Admittedly this is a simplified example. Yields at longer maturities will usually move some, albeit less than short maturities as the Fed raises or lower rates, making this simplified scenario analysis at best an approximation. But it does further illustrate the conflict that exists in the narratives being told by stocks and bonds.

Conclusion

The title of this Market Insights, Liar’s Poker, refers to a game where each player attempts to bluff the other player about the number of repeating digits on the serial number of a random dollar bill. I might bet four zeros. You might bet five 3’s upping the ante each round until one player calls the other a liar. With each round, I could of course be telling the truth or lying. It’s your job, as the opposing player, to determine if I’m telling the truth or spinning some fantastic tale. Much like the game, markets sometimes speak the truth, but very often on the way to the truth, there’s at least a bit of embellishing that occurs. In behavioral science this is sometimes referred to as extrapolation bias or recency bias, where near term events are taken on a near linear path to a conclusion that may be unreasonable. I fear we have a bit of that today. Today’s tale, I believe to be not only quite a yarn, but a real whopper when taken in context. In bubbles, one of the final stages is what is called a blow off top where you see all sorts of excess risk taking and speculation…crazy stuff. Resist the urge to buy into this temptation. Stick to your plan, rebalance and don’t be lured in. Embrace bonds. While they haven’t done particularly well in the past year or two, they haven’t been this attractive in 20 years. For us, this has left us generally underweight

U.S. Equities in favor of more attractively valued opportunities across the globe. Markets ultimately tell the truth. But they do bluff quite frequently along the way. Thank you, as always, for your continued trust and confidence.

For more news, information, and analysis, visit the ETF Strategist Channel.

Market Insights is intended solely to report on various investment views held by Integrated Capital Management, an institutional research and asset management firm, is distributed for informational and educational purposes only and is not intended to constitute legal, tax, accounting or investment advice. Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. Integrated Capital Management does not have any obligation to provide revised opinions in the event of changed circumstances. We believe the information provided here is reliable but should not be assumed to be accurate or complete. References to specific securities, asset classes and financial markets are for illustrative purposes only and do not constitute a solicitation, offer or recommendation to purchase or sell a security. Past performance is no guarantee of future results. All investment strategies and investments involve risk of loss and nothing within this report should be construed as a guarantee of any specific outcome or profit. Investors should make their own investment decisions based on their specific investment objectives and financial circumstances and are encouraged to seek professional advice before making any decisions. Index performance does not reflect the deduction of any fees and expenses, and if deducted, performance would be reduced. Indexes are unmanaged and investors are not able to invest directly into any index. (MMXXIV-I)