By Kevin Nicholson, CFA

SUMMARY

-

- Viewed through various lenses, we believe inflation will remain a problem throughout 2022.

- Consumers can help pump the brakes on inflation by slowing purchases, in our view.

- Additionally, we believe equities offer a better alternative than bonds for keeping up with inflation.

A Deeper Dive on the Impact on the Consumer

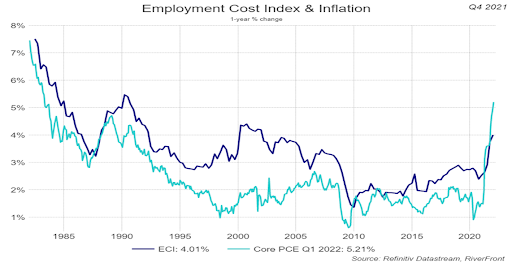

The COVID-19 pandemic has consumed the global economy for the last two years, and as it recedes from the headlines, it is replaced by inflation. In the US, headline inflation grew 7.9% year-over- year in February, hitting a 40 year high. We believe the primary cause is the fiscal and monetary stimulus applied during the pandemic by the US government in the form of transfer payments and the Federal Reserve’s (Fed) balance sheet growth. This coordinated stimulus led to money supply growing faster than nominal Gross Domestic Product (GDP) for most of the pandemic, thus inflating consumer prices in a supply-constrained environment. For the average American, prices (light blue line, chart below) are rising faster than wages (dark blue line) which will eventually cause an economic slowdown, as consumers spend more of their income on necessities and less on discretionary items such as travel and entertainment.

Taking a deeper dive on the impact that inflation is having on the consumer, we look at flexible Consumer Price Index (CPI). The expenditures in the CPI Index that are defined as ‘flexible’ include items such as food, energy, and clothing that have rapid price changes; food and energy are two of the largest components. Flexible CPI has increased by 18.2% over the last year and currently is rising at a 19.9% annualized rate through February, due the Russian invasion of Ukraine and continued supply-chain bottlenecks. There may be little relief in food and energy prices if Russian sanctions remain in place and war disrupts planting season in the Ukraine, the world’s largest grain supplier.

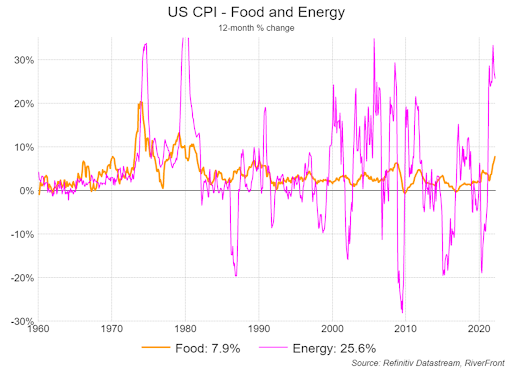

Food and energy prices are the two necessities that garner the biggest portion of the American worker’s income, so while the Fed tends to focus on measures that exclude food and energy like core Personal Consumption Expenditures (PCE), the average worker is focusing on how far their paycheck can stretch. In the last year, the cost of food has increased 7.9%, right in line with headline inflation. Everyone must eat, so consumers may resort to buying white labeled grocery store brands instead of nationally recognized brands to make a dollar go further.

In the case of energy, prices have risen over 25% year-over-year. Rising energy prices are coming at a time when the economy is reopening, and workers are going back into the office, spurring demand just as crude stockpiles have been falling and production decreasing due to sanctions against Russia. In the chart below, energy inflation has proven to be very volatile over the last fifty years, while food inflation has been more stable. We believe the combination of the food and energy inflation rising at the same time is concerning.

While we have highlighted the impact of food and energy on the consumer, we want to give further insight by looking at sticky versus flexible CPI. Sticky CPI looks at a basket of goods in the CPI index whose prices do not change rapidly. The sticky CPI basket focuses on expenditures such as education, medical care, and housing. In the last year, sticky CPI has risen 4.5% and currently is rising at a 6.5% month-over month annualized rate. While sticky CPI’s current trajectory is not as high as that of flexible CPI, it still is negatively impacting consumers because, monthly it’s higher than the 5.8% growth rate on wages. Additionally, while sticky CPI goods are slower to change prices, when they ultimately do rise, they tend to be larger increases. For instance, tuition expenses are set on an annual basis so they are repriced with a lag but will likely reflect upward price pressures over the previous 12 months. We expect sticky CPI to continue to climb higher as input costs climb throughout the year. From the consumer’s perspective, inflation is ‘public enemy number one’ as prices keep climbing and eating up more and more of their paycheck.

Looking at inflation through the lens of the Fed is more nuanced than that of the consumer, but policy changes enacted by the Fed also impacts the consumer. The Fed recently raised the Federal Funds (Fed Funds) rate to fight inflation but has since realized that it may need to move faster than the 25-basis point increase announced at the Federal Open Market Committee (FOMC) meeting on March 16th. Instead of raising the Fed Funds rate by 25 basis points at each of the remaining six meetings for the year, the Fed is now contemplating some 50 basis point increases along the way. The goal for the Fed is to reach the neutral rate, the rate where inflation is constant, and the economy is at full employment with maximum production. The neutral rate cannot not be determined with pinpoint accuracy, but most economists believe it to be approximately 2% to 2.25%. The neutral rate aligns with the Fed’s traditional 2% inflation target using core PCE. Unfortunately, January’s core PCE reading was running at 5.2% year-over-year, well above the 2% average the Fed targets.

In conclusion, regardless of the lens through which investors choose to view inflation, we believe it will remain a problem throughout 2022. The Fed has vowed to do whatever it takes to get inflation under control and only time will tell if they are successful. The ‘cure for high prices is high prices’, as the saying goes… in other words, we believe consumers can help the Fed pump the brakes on inflation by slowing purchases. In the meantime, we continue to favor equities over fixed income across the portfolios. We believe that equities offer a better alternative than bonds for keeping up with inflation, given that rising yields create bond price depreciation and inflation erodes the ability of income to offset losses. We favor ‘inflation recovery plays’, like energy, some materials, and industrial companies whose earnings respond positively to inflation and nominal growth. In general, we will proceed with caution given the complex implications of inflation on returns for both equities and fixed income.

For more news, information, and strategy, visit the ETF Strategist Channel.

Important Disclosure Information:

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

All charts shown for illustrative purposes only. Technical analysis is based on the study of historical price movements and past trend patterns. There are no assurances that movements or trends can or will be duplicated in the future.

In a rising interest rate environment, the value of fixed-income securities generally declines.

A basis point is a unit that is equal to 1/100th of 1%, and is used to denote the change in a financial instrument. The basis point is commonly used for calculating changes in interest rates, equity indexes and the yield of a fixed-income security. (bps = 1/100th of 1%)

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero).

Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

The Consumer Price Index (CPI) is a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them. Changes in the CPI are used to assess price changes associated with the cost of living. The CPI is one of the most frequently used statistics for identifying periods of inflation or deflation.

The term personal consumption expenditures (PCEs) refers to a measure of imputed household expenditures defined for a period of time. Personal income, PCEs, and the PCE Price Index reading are released monthly in the Bureau of Economic Analysis (BEA) Personal Income and Outlays report.

The federal funds rate is the target interest rate set by the Federal Open Market Committee (FOMC). This is the rate at which commercial banks borrow and lend their excess reserves to each other overnight.

Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2022 RiverFront Investment Group. All Rights Reserved. ID 2098675