The most recent Federal Open Market Committee (FOMC) meeting triggered a response in both equity and fixed income markets reversing the inflation trade that has pushed longer term interest rates up and put value in favor over growth stocks. The U.S. Federal Reserve hinted that inflationary pressures may not be as transitory as first thought leading to expectations of a potential taper in asset purchases and a potential shift in their timeline regarding rate increases. While the more hawkish tone pushed long-term rates down, we expect to see rates resume an upward path over the near-term.

There has been a lot of debate concerning whether or not inflation is transitory. This is an important concept and has been used by more dovish Fed members to justify an accommodative monetary policy into 2023. Inflation can be cost-push or demand-pull. In the current environment, we are seeing both in play. For example, supply chain disruptions and dislocations created by COVID have lowered the supply of goods and services, therefore, placing upward pressure on prices.

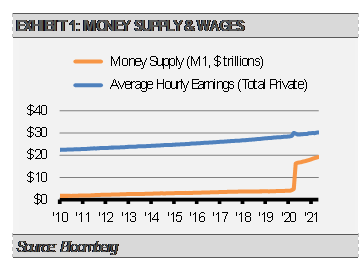

Couple this with pent up demand, a lot of liquidity (exhibit 1), stimulus, low interest rates, and higher wage pressures, and it makes it hard not to expect interest rates to resume an upward trajectory from their recent lows. The extent and duration of this will largely depend on which factors are actually transitory and if the Fed reacts promptly with rate hikes while abandoning their current interest rate hike expectations.

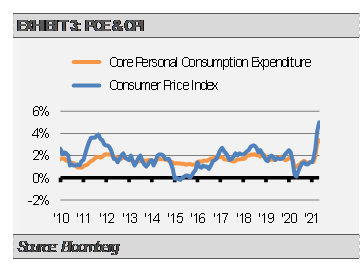

The Fed thus far has taken the position that inflation is transitory for the most part and has shown a willingness to ignore inflation by allowing it to drift higher than their target instead of remaining more focused on employment levels as a trigger. Of concern is that some elements impacting inflation may not be as temporary. For example, wage rates tend to be sticky, and this coupled with improvements in the unemployment rate as well as interest rate hikes off the table until 2023 as planned, could mean demand-pull inflation remains. Another consideration is the Fed’s inflation target is the Core Personal Consumption Expenditures (PCE) deflator, which excludes food and energy, rather than the Consumer Price Index (CPI), which is inclusive of food and energy and tends to run higher.

This leaves a lot of room for inflation expectations to move interest rates higher at least over the near-term and possibly trigger a shift in Fed policy impacting both the long and short end of the yield curve.

The current environment creates complexities for fixed income investors. The risks to both the long and short ends of the yield curve make variable rate and inflation-linked strategies attractive. Variable rate bonds, preferreds, and bank loans have coupons that reset based on a reference rate, which is correlated with the Fed Funds Target Rate or the markets expectations with respect to the rate. This provides investors with a hedge from a surprise shift in Fed policy due to inflation.

Inflation-linked bonds can also provide protection from rising rates due to inflation expectations and are offered in varying duration ranges. These securities adjust the principal with moves in inflation. Coupon payments, therefore, will be calculated on the inflation adjusted principal.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.