Investors benefit the most over time by making less emotional decisions with regards to their portfolios. Helping investors overcome their behavioral biases is at the heart of everything we do. Each day presents us with another incredible opportunity to help.

Every few years, it seems the markets find another new idea that steals the headlines and dominates short-term returns. Seeing some stock prices rise while others languish can create a fear of missing out, or FOMO. If timed perfectly, playing on this momentum can reap impressive results. But we also know that over time, attempting to time the markets is a fool’s game.

While many market participants are enthused by the shiny new objects of the day, amazing investment opportunities are often being ignored, at least for a time. Eventually, markets once again normalize, and the shiny objects fade into the background as the once ignored opportunities take the lead.

Currently, with a very few large cap U.S. stocks driving equity market returns, we are seeing both the FOMO trades and an abundance of opportunities found outside of the spotlight.

In our view, the best solution for the FOMO challenge is discipline. By digging into the data, we can find many opportunities to generate attractive returns while managing risks in real time. Our Three Layers of Risk Management process helps us identify strategic long-term attractive investments as well as tactical opportunities while maintaining a plan in case of an emergency. We have seen this movie before. In fact, a similar equity market scenario played out only a few years ago. The narrow market rally we have experienced so far this year looks very similar to the narrow market rally we saw during the first few months of the 2020 pandemic recovery.

In September 2020, we wrote about the narrow market rally and that we thought investors could find compelling opportunities in other sectors of the equity market over the months to come. In our April 2021 commentary, we showed that the equity market quickly shifted from the early equity market recovery darlings to other sectors that were initially neglected (exhibit 1). We anticipate that the coming months will bring similar opportunities for disciplined investors.

In fact, we think that markets are packed with opportunities that have been neglected in the current narrow market recovery. Consider that while the capitalization-weighted S&P 500 Index has appreciated nearly 8.9% through May, an equal-weighted version of the same index is down more than 1.4% and the Russell 2000 Index of small companies is relatively flat at -0.6%.

Looking at this performance disparity more deeply reveals the following according to Capital Economics1:

- a market-cap weighted portfolio of the largest five companies in the S&P 500 Index returned roughly 40% through May, compared to only about 2% for the next 95 largest constituents and less than 1% for the remaining 400 firms; and

- approximately 70% of the current constituents of the S&P 500 Index have risen in price by less than the overall Index, around half have actually fallen in value this year, and about a quarter are down more than 10%.

INVESTMENT IMPLICATIONS

Today’s market environment has many similarities to the initial recovery from the early 2020 stock market declines. Just as we saw the number of investment opportunities increase during the narrowly led pandemic work-from-home market, we are seeing more attractive opportunities elsewhere. These opportunities include U.S. equities that have lagged or even suffered price declines this year as well as alternative assets, such as MLPs, whose earning’s potential and yields remain strong while their prices have lagged.

Overall, our largest broad equity sector overweights are to health care, energy (via MLPs), and consumer staples. Furthermore, because of the stretched valuations of the market capitalization-weighted indices, traditional fixed income looks very attractive as it can both act as a ballast to offset potential equity market risk while also generating attractive current income.

By staying true to a disciplined process and not succumbing to FOMO, investors can rest easier knowing their investments are allocated across a wide range of attractive opportunities. We have been writing optimistically about the opportunities that lie ahead for the next several years for months now. The stock market’s recent concentration has only made those neglected areas that much more attractive. Investors only need to look more broadly at the attractive valuations found outside of the latest market darlings to find areas likely to do well going forward.

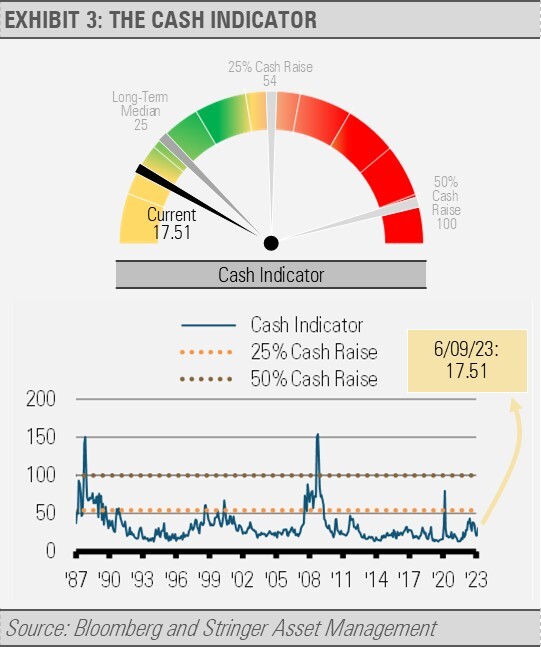

THE CASH INDICATOR

The Cash Indicator (CI) is well below its long-term median level. Readings this low suggest that markets are overly complacent. Therefore, we expect that markets may be at risk of a decline due to an unexpected shock over the coming months. Still, the risk of a crash remains low as there is plenty of liquidity and a solid long-term fundamental backdrop.

1Allen, Oliver. “Narrow stock market rallies have rarely lasted long.” Capital Economics Global Markets Update. Capital Economics, May 24, 2023. https://www.capitaleconomics.com/publications/global-markets-update/narrow-stock-market-rallies-have-rarely-lasted-long. Accessed 6/08/23.

For more news, information, and analysis, visit the ETF Strategist Channel.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.

Index Definitions:

S&P 500 Index – This Index is a capitalization-weighted index of 500 stocks. The Index is designed to measure performance of a broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.