by DOUG SANDLER, CFA

THE RIVERFRONT WRITING TEAM

REBECCA FELTON, Senior Market Strategist

CHRIS KONSTANTINOS, CFA, Director of Investments | Chief Investment Strategist

KEVIN NICHOLSON, CFA, Global Fixed Income Co-CIO |Co-Head of Investment Committee

DOUG SANDLER, CFA, Head of Global Strategy

ROD SMYTH, Chairman of the Board of Directors

SUMMARY

- QE, low rates, higher taxes, and rising inflation are important investor concerns, in our view.

- We do not believe these concerns should lead investors to abandon risk assets.

- We believe risk assets can provide protection from these concerns and should represent meaningful allocations in most portfolios.

Money printing, low rates, rising debt, tax and inflation concerns are NOT reasons to abandon stocks, in our view

‘The best laid schemes o’ mice an’ men, Gang aft a-gley [goes wrong]’ – Robert Burns

Since the financial crisis in 2008 we have witnessed an extraordinary behavioral phenomenon. It all started with a growing list of what we would call ‘ideological’ investor concerns that included:

- Money Printing: ‘Money-printing’, more kindly referred to as quantitative easing (QE), has irked many investors from the start. Ideologically, they would argue that the Federal Reserve should not intervene in financial markets.

- Low Interest Rates: One of the outcomes of money printing is artificially low interest rates. Many worry that interest rates are being kept too low for too long despite clear signs that the US economy is recovering.

- Rising Debt and Higher Taxes: The COVID-19 crisis elevated the concern that programs such as paycheck protection, enhanced unemployment benefits, stimulus checks, and eviction moratoriums have undermined the economy’s natural healing ability. These programs would also contribute to the significant government debt, which would ultimately need to be financed by higher taxes.

- Inflation: Rising prices (inflation) and the declining affordability of the basics like food, gasoline, transportation, and housing have further increased anxieties.

While we also share many of these worries and wonder about their long-term implications, these ideological concerns are not the behavioral phenomenon we are speaking about. The phenomenon we refer to above is the way in which many investors are reacting to these concerns. The common reaction by these investors is to sell ‘risk assets’, like stocks and commodities, and to hide in ‘stable assets’ like cash, CDs, and bonds. The irony is that a shift from risk assets to stable assets may make these investors even more vulnerable to these concerns.

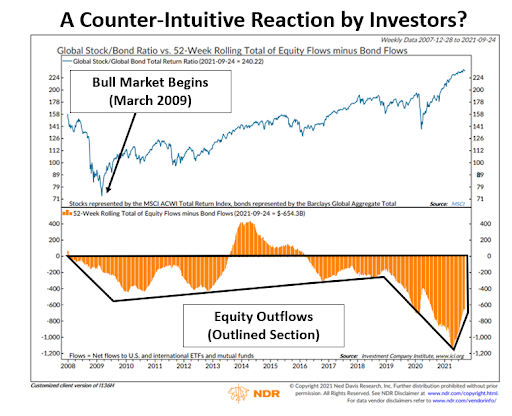

This is because stable assets have less potential to rise to offset the impact of money printing, low rates, higher taxes, and/or spikes in inflation. In our opinion, this behavior of worried investors can be seen in the chart below from Ned Davis Research. The top panel shows that global stocks have consistently outperformed global bonds since 2009. Yet, the bottom panel displays a consistent pattern of fund flows out of stocks into bonds throughout most of the 12-year recovery.

Copyright 2021 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo.

Risk assets have a different return profile than stable assets. While they have the potential to decline in value – sometimes substantially – they also have the potential to rise. For example, money printing can be good for risk assets because it creates asset price inflation, which many Americans have experienced over the last decade through the ownership of their homes. Likewise, the negative implications of higher taxes and government spending can be partially offset by owning the stocks of companies that are the beneficiaries of that spending. Low interest rates are rarely a negative for risk assets like stocks since low rates provide low-cost funding for companies with attractive investment opportunities. Finally, risk assets can sometimes partially protect an investor against inflation since many companies can raise prices and pass that inflation on to consumers without sacrificing their earnings.

While we believe that the ownership of risk assets is currently the best way to protect oneself from these ideological concerns, there are times where risk assets can be expected to perform poorly and a shift away from them would be justified. One example would be a lasting economic crisis like the one experienced in 2008/2009. Another example would be an event that causes foreign investors to lose faith in the US’ ability to repay our debt. A third example would be a massive change to the tax code that would significantly impact corporate earnings. A final example would be a period of high and lasting inflation that would permanently impair stock valuations.

Crises trigger policy responses. While RiverFront’s view is that these examples are unlikely to come to fruition in the near-term, if they were to happen, we think the negative implications to risk assets would not be long-lasting. This is because policymakers would likely intervene before any such crisis could take lasting hold. Their intervention would likely follow the same playbook they have been following for over a decade; print more money, further lower interest rates, and ramp-up fiscal spending. Such a response would, when the dust settles, likely benefit risk assets while further punishing stable assets. Given these realities, RiverFront’s balanced portfolios remain overweight risk assets relative to our benchmarks. Furthermore, we think investors should consider the following:

- Accumulate Investors: Given the long-time horizons of accumulate investors, declining purchasing power poses one of the most important risks to attaining goals. Risk assets, in our view, provide the best protection against declining purchasing power and should thus be fully represented in accumulate portfolios. Additionally, declining markets offer the accumulate investor the opportunity to buy stocks at lower prices.

- Sustain Investors & Distribute Investors: Purchasing power protection is also important to sustain and distribute investors since retirement can encompass many years. According to the Social Security Administration, a 65-year-old male has a life expectancy of 19 years while a 65-year-old female can be expected to live nearly 22 years. Mathematically, this means 65-year-olds will need their money to grow 1.8x for males and 1.9x for females in a 3% inflationary environment. As inflation increases, the required growth rate also increases. For example, if inflation rose to 5%, 2.6x growth would be needed for a 65-year-old male and 3x growth for a female, all else being equal. Therefore, we believe sustain and distribute investors should consider meaningful allocations to risk assets in their portfolios and favor income vehicles that offer the potential for distribution growth, like stocks with growing dividends.

For more news, information, and strategy, visit the ETF Strategist Channel.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

Principal Risks:

In a rising interest rate environment, the value of fixed-income securities generally declines.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

When referring to being “overweight” or “underweight” relative to a market or asset class, RiverFront is referring to our current portfolios’ weightings compared to the composite benchmarks for each portfolio. Asset class weighting discussion refers to our Advantage portfolios. For more information on our other portfolios, please visit www.riverfrontig.com or contact your Financial Advisor.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below.

Changes in the value of foreign currencies compared to the U.S. dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the U.S. dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the U.S. and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-U.S. securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Index Definitions:

MSCI ACWI (All Country World Index) captures all sources of equity returns in 23 developed and 23 emerging markets.

For each outcome category (accumulate, sustain and distribute) RiverFront’s portfolio management team has assigned one or more RiverFront product(s) based on their assessment of the product’s investment objective as it relates to a typical client’s return and risk objectives when seeking investment outcomes of accumulating wealth, sustaining wealth and distributing wealth. The team has also designated RiverFront product alternatives for those clients looking to take more or less risk with the outcome category. The ‘more aggressive’ (or more risk) alternatives will generally have greater equity and international exposure as well as longer time horizon targets, while those designated as ‘more conservative’ (or less risk) will have fewer equities, a lower exposure to international and shorter time horizon targets. Since the risk assessments are dependent on the outcome category selected, RiverFront products may fall in multiple categories. For example, the Advantage Global Allocation portfolio, may fall under ‘more aggressive’ to those with the outcome of ‘sustain’, but ‘more conservative’ for investors interested in ‘accumulation’. All investments carry a risk of loss and there is no guarantee that an investment product or strategy will meet its stated objectives.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2021 RiverFront Investment Group. All Rights Reserved. ID 1870454