Last month, we thought that the flash purchasing managers indices, which provide a proxy for growth expectations, and the Jackson Hole Economic Symposium were top events. First, the flash purchasing managers index showed a general decrease from an elevated level. Most likely, this decrease in growth expectations occurred because of the pickup in COVID-19 cases globaly. The Jackson Hole Economic Symposium did not disappoint. Federal Reserve chairman, Jerome Powell, released statements suggesting that inflation has likely reached a sustained level above the 2% target, while employment has not completely recovered and the COVID-19 delta variant remains a risk. Heading into September, we think the following are the top three events that could impact financial markets.

Taper torture?

The traditional method for analyzing monetary policy focused solely on changes to short-term interest rates. However, since the Great Financial Crisis (2008), assets purchasing programs by central banks (a.k.a. “quantitative easing”) are as important, if not more, than short-term interest rate policy. Unfortunately, we do not have a rich history of the impact of changing asset purchasing programs on financial markets. Currently, the US Federal Reserve Bank (“Fed”) purchases $120 billion of Treasuries and asset-backed mortgages per month. In our opinion, any reduction in this purchase program should be considered tightening monetary policy. Thus, financial markets could torture themselves in finding any insight into the Fed’s plan. The next official Fed meeting is on September 24, 2021.

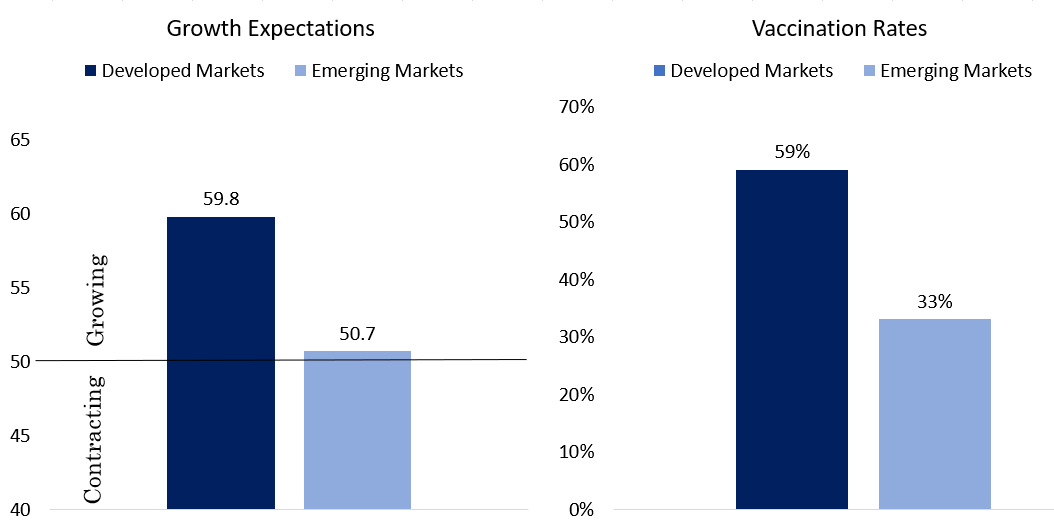

Diverging COVID-19 vaccination policies

A quick glance at the COVID-19 vaccination rates shows a stark difference between Developed Market (“DM”) countries and Emerging Market (“EM”) countries. The average DM country has a 59% vaccination rate, while the average EM country has a 33% rate. The most recent growth expectations data also shows a significant difference between the DM and EM regions, with the DM region much more opportunistic about future growth. During the first week of September, the growth expectations data for a variety of countries will be released. While we expect a deterioration in growth expectations given the recent increase in COVID-19 cases globally, we will be more curious if the gap between DM and EM growth expectations remains. If the growth expectation gap remains, we would continue to expect DM country equity market performance, on average, to outpace EM country equity market performance.

Figure 1.

Source: Innealta Capital. “Growth Expectations” refers to the Market PMI Manufacturing Index for Developed Markets and Emerging Markets, respectively. Vaccination Rates as of 08/25/2021. PMI data as of 07/31/2021.

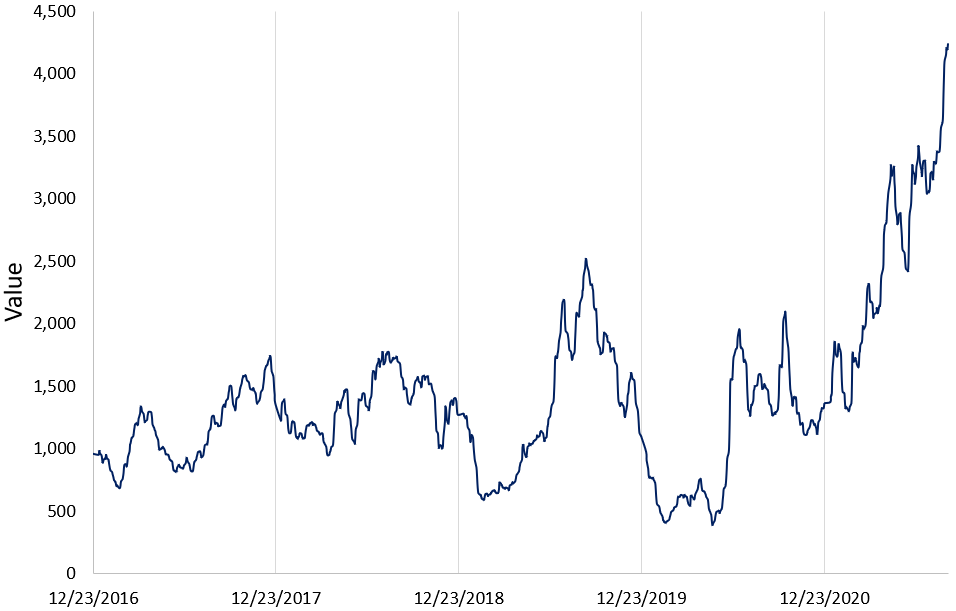

Boats of trade

While the most recent US Consumer Price Index (“CPI”) reading showed a 4.1% year-over-year increase, criticism has grown that the CPI index does not reflect global inflationary pressures. Shipping accounts for 90% of traded goods. The Baltic Dry Sea Index, which measures shipping container pricing, has increased by over 210% year-to-date! As the surge in COVID-19 cases is likely to create increased pressure on global supply chains and slow down global demand, it will be interesting to see how shipping container prices react and, more importantly, long-term inflation expectations. So far this year, long-term inflation expectations have not increased as the market seems to think that inflation could be temporary.

Figure 2. Baltic Dry Sea Index

Source: Innealta Capital. Time frame 12/31/2016 to 08/27/2021. Frequency daily.

From a market information perspective, we expect September to be more exciting than August. The macroeconomic growth expectations data will begin during the first few days. COVID-19 related information, either vaccinations or cases, will occur throughout the month. And the US Federal Reserve Bank will conclude the month. We maintain the view that changes to US monetary policy are the most important driver of financial market performance during September.

Disclosures

This material is for informational purposes and is intended to be used for educational and illustrative purposes only. It is not designed to cover every aspect of the relevant markets and is not intended to be used as a general guide to investing or as a source of any specific investment recommendation. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, investment product or service. This material does not constitute investment advice, nor is it a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. In preparing this material we have relied upon data supplied to us by third parties. The information has been compiled from sources believed to be reliable, but no representation or warranty, express or implied, is made by Innealta Capital, LLC as to its accuracy, completeness or correctness. Innealta Capital, LLC does not guarantee that the information supplied is accurate, complete, or timely, or make any warranties with regard to the results obtained from its use. Innealta Capital, LLC has no obligations to update any such information.

840-INN-08/30/2021