Click here to download the PDF

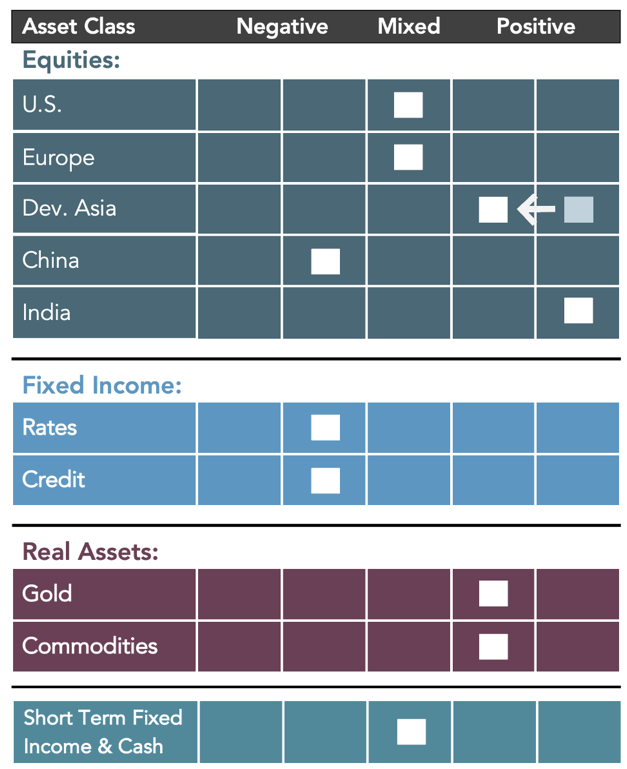

Equities:

Equities:

▶U.S. equities have continued to reach record highs pushing the S&P 500 even further into significantly overvalued territory. At the conclusion of the most recent FOMC meeting in early November, the Fed officially announced its plan to begin to taper its current $120 billion in monthly bond purchases. However, the announcement was not a surprise to the markets, and the Fed has successfully separated its tapering of bond purchases from any intention to raise short-term interest rates for the foreseeable future. Therefore, U.S. equity markets seemed to take the Fed’s announcement in stride. However, the risk that current heightened inflationary pressure from supply chain disruptions could continue well into 2022 remains a risk to the U.S. equity markets, particularly if the Fed’s reaction to these pressures is dismissed for too long.

▶The outlook for European equities remains unchanged. Although economic activity has rebounded throughout the EU, inflationary pressures have risen well above their comfort zone, and as in the U.S., it remains to be seen how transitory inflation in the EU will turn out to be. The EU has also experienced a widening of investment grade credit spreads which is a concern for corporations looking to refinance and service their debts. Further complicating the picture, the EU is already facing an energy shortage heading into winter which could be further emboldened should the winter weather in Europe be more severe than normal.

▶Japanese equity markets remain relatively more attractive on a valuation basis, though growth prospects as displayed by our flattening yield curve measure for the Japanese economy have dimmed somewhat. However, the recent elections in Japan have increased the possibility of future additional fiscal and monetary stimulus.

▶India equities continue to benefit from a yield curve that is both positively sloped and continuing to steepen. India should also continue to benefit from stimulative monetary and fiscal policy leading up to the elections.

▶The outlook for China equities remains clouded in uncertainty around the continuing financial difficulties among Chinese real estate development firms, more restrictive government policies and a slowing Chinese economy. The most recent report of GDP growth out of China showed that economic growth had slowed from +7.9% to +4.9% in the most recent quarter.

Fixed Income and Real Assets:

As inflationary expectations continue to rise faster than nominal interest rates, real interest rates remain decidedly negative (nominal interest rates less inflationary expectations) and our model research continues to favor real assets (commodities and gold) over fixed income as an asset class.

About 3EDGE

3EDGE Asset Management, LP, is a global, multi-asset investment management firm serving institutional investors, the advisor marketplace, and private clients. 3EDGE strategies act as tactical diversifiers, seeking to generate consistent, long-term investment returns, regardless of market conditions, while seeking to manage downside risks. The primary investment vehicles utilized in portfolio construction are index Exchange Traded Funds (ETFs). The investment research process is driven by the firm’s proprietary global capital markets model.

The model is tested over the widest variety of economic and market conditions and translates decades of research and investment experience into a system of causal rules and algorithms to describe global capital market behavior. 3EDGE offers a full suite of solutions, each with a target rate of return and risk parameters, to seek to meet investors’ different objectives. Of course, investing involves risks and the potential loss of your investment. There is no guarantee that any target return will be achieved.