Economic Overview

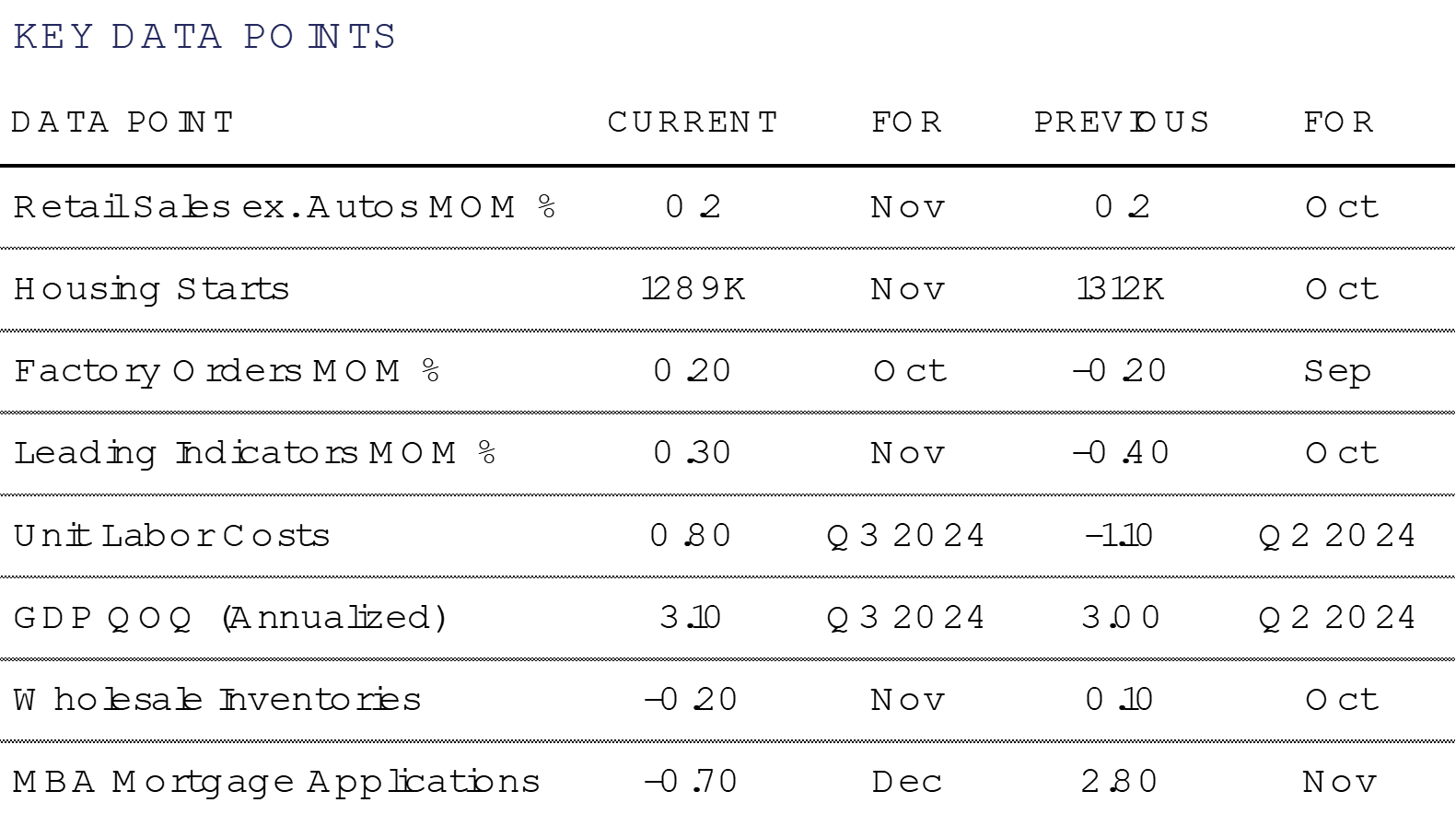

To close out the year The Fed cut rates by a quarter point to 4.25%-4.5%, as the market expected. Now the messaging of fewer cuts next year coupled with the possibility of higher expected inflation seems to be front of mind for many investors. Following the meeting, bond yields initially rose, with the biggest increase in 2- and 3-year notes and smaller increases in longer maturities, reflecting the expected pause.

The statement released by the committee changed only slightly, to include “In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks.” This led most to believe they are open to skipping cuts at future meetings.

Beth Hammack was the only voting member to openly express opposition to the cuts and instead favored no change in rates for now. However, there are four dots still at 4.625%, suggesting others may have also opposed the rate cuts at this time. The median dots for 2025 now illustrates two cuts (previously four) while the GDP forecast and projections for unemployment remain relatively unchanged. The most significant change in forecasts came in the inflation outlook. The 2025 PCE forecast rose from 2.1% to 2.5%, while the core PCE inflation forecast rose from 2.2% to 2.5%.

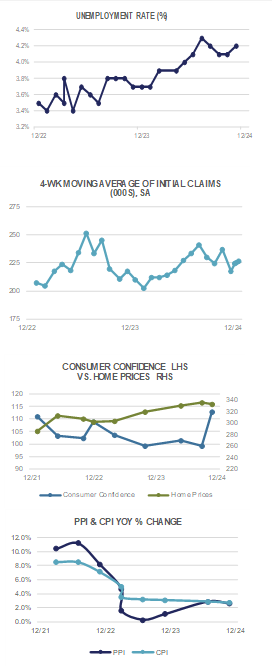

According to the National Association of Realtors, existing-home sales ascended +4.8% in November to a seasonally adjusted annual rate of 4.15 million, the swiftest pace since March (4.22 million). Sales accelerated +6.1% from one year ago, the largest year-over-year gain since June 2021 (+23.0%).

This is a stark contrast to December which saw a cooling in mortgage applications possibly signaling a slowdown in the very hot housing market. Mortgage volumes were the lowest in 10 months on a seasonally adjusted basis likely attributed to elevated borrowing costs. As we go to print, 30 year mortgage rates flirt with 7%, as we have seen longer-dated Treasury yields rise following hawkish projections by the FOMC.

Domestic Equity

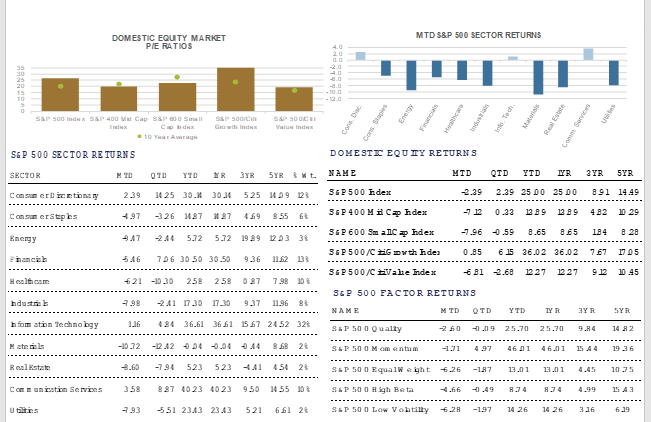

U.S. equities closed 2024 on a relative low note, with the benchmark S&P 500 Index shedding -2.4% to close at 5,882. While a Santa Claus rally didn’t materialize this year, the market as a whole made 57 all-time highs and posted a +25.0% total return on the year. What’s more, the market’s two-year performance ranks as one of the best since 1998.

From a market capitalization standpoint, 2024 was again dominated by the largest names in the broad market index. Specifically, the S&P Top 50 Index posted gains of +0.6% in December, showing some defensiveness relative to the rest of the market, and gains of +33.8% in 2024. The more than +800 basis point outperformance of Mega-Caps relative to the S&P 500 Index as a whole can also be highlighted by Factor and Sector contribution and concentration. For example, the S&P Momentum Index gained +46.0% in 2024, a nearly +1,000 basis point outperformance over the S&P 500 Growth Index (+36.1% return), and a nearly +2,000 basis point return on the S&P 500 Quality Index (+25.7% return). The S&P 500 Value Index on the other hand returned +12.3%.

From a sector standpoint, 8 of 11 S&P 500 sectors finished December in negative territory. The laggards were notable Value oriented sectors such Materials (-10.7%) and Energy (-9.5%), while interest rate sensitive sectors such as Real Estate (-8.6%) and Utilities -7.9%) were impacted by rising interest rates. Communication Services (+3.6%), Consumer Discretionary (+2.4%), and Information Technology (+1.2%) were the top performers on the month.

Small- and Mid-Caps gave back gains in December, with the Mid-Cap 400 and Small-Cap 600 Indices posting returns of -7.1% and -9.0%, respectively. While SMID-Caps collectively were underperformers during the period, their valuations remain compelling compared to Large-Caps, and Growth oriented sectors heading into 2025

Concentration risk remains top of mind heading into 2025. The “Magnificent 7” again produced outsized returns in 2024. According to data compiled by JP Morgan, the Magnificent 7 represented 55% of the market’s overall return. This small cohort of the market has been responsible for more than 50% of market returns for the past 3 consecutive years. Concentration risk can also be seen by the fact the U.S. makes up more than 67% of the world’s investable universe, and that the top 10 names in the S&P 500 represent nearly 39% of the market, both all-time highs.

Concentrated performance remains a key risk for 2025; however, concentration may pose an opportunity for rebalancing across the rest of the market – from the “other” 493 stocks in the S&P 500, to Small- and Mid-Caps, and Value oriented sectors.

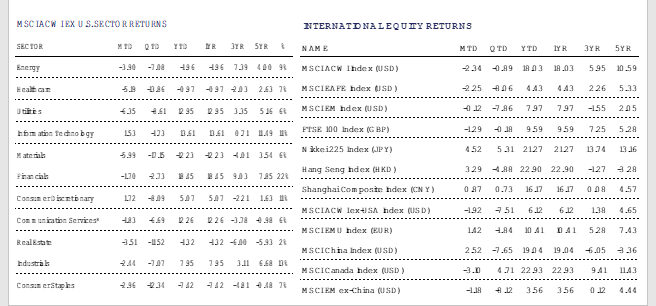

International Equities

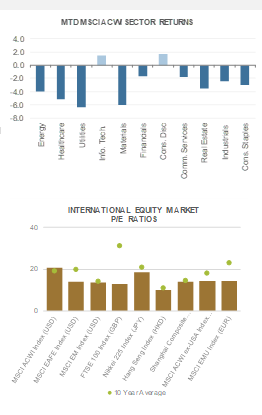

Internationally, markets were mixed but generally negative. The MSCI EAFE Index, which tracks developed markets outside the U.S. and Canada, was down over -2.0% last month. While the MSCI Emerging Market Index was relatively flat at -0.1% on the month.

The German market had a modest gain last month as the DAX was up +1.4% on the month, outperforming the STOXX Europe 600 Price index, which was down -1.0% on the month. This continues the 2024 trend as the German DAX has significantly outperformed the STOXX Europe 600 (+18.9% vs +9.0%), reaching an all-time high in December and was one of the top preforming European countries in 2024. Despite Germany’s solid performance in 2024, it failed to eclipse the US market and has showed signs of concern. The IFO Institute’s business-climate index, which measures German business managers optimism, dropped to 84.7, marking the sixth decline in seven months and the lowest point since May of 2020. Germany has been struck with political uncertainly with Premier Scholz losing a confidence vote in the German parliament earlier in December. Additionally, it’s manufacturing sector shows signs of slowing as major employers such as Volkswagen, Bosch, and Schaeffler have announced layoffs.

The Shanghai Composite Index also had a positive month, up +0.9% and a positive year up +16.2%, but still underperformed US markets. China’s economy currently grapples with significant excesses: a vast number of vacant or incomplete apartment complexes, trillions of dollars in debt that are straining local governments, and a surge in industrial production that is fueling an increase in exports and escalating global trade tensions. According to a recent WSJ article, the Chinese property meltdown has destroyed nearly $18 trillion of household wealth. To put this in perspective, that is more than American households lost during the 2008-2009 great financial crisis and is greater than the value of all listed stocks in China. China’s working age population continues to decline, while borrowing is approaching nearly three times it’s annual GDP. Time will tell if China’s strengths, such as its leadership in manufacturing or new stimulus packages will be enough to offset these robust headwinds.

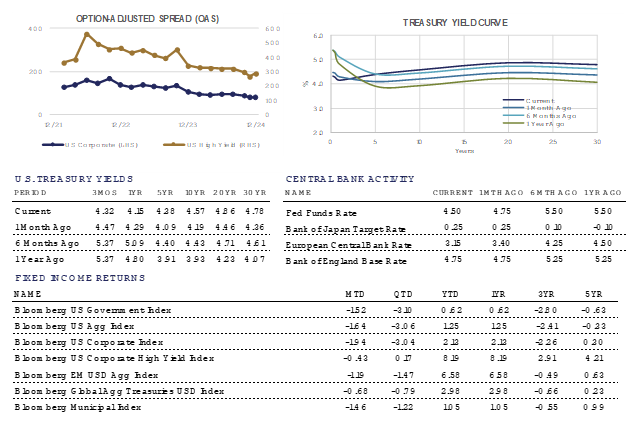

Fixed Income

In December, the Federal Reserve lowered the Federal Funds Target Rate by another 25 basis points, as expected. This rate cut was a bit controversial due to the lack of recent progress in bringing inflation back down to target. The most commonly referenced inflation measurements have actually reversed course and begun to move higher since September 2024.

To counterbalance the dovish positioning of an interest rate cut, the Fed’s statement and Dot Plot (a chart showing Fed official’s interest rate expectations) were significantly more hawkish than prior releases. The market had been expecting continued interest rate cuts throughout 2025. The Federal Reserve has tempered those expectations, with more than 100 basis points of market projected 2025 rate cuts evaporating during the fourth quarter of 2024.

Many market outlooks for 2025 have voiced concerns over the ability to push inflation lower from current levels. The outcome of the Presidential and Congressional elections have also influenced those concerns, given a focus on tariffs and moving production to more expensive locations.

These concerns may leave bond yields range bound in the near-term, as the markets wait to see what effects the change in administration will bring. Even so, the yield levels currently available on high quality fixed income investments are quite compelling on their own.

The month of December and the entire fourth quarter of 2024 was challenging for bonds as interest rates rose, and pushed bond prices lower. For the year, the bond indices tracked were uniformly positive, even with the headwind of rising interest rates. This is due to the attractive risk/return tradeoff that fixed income offers. Current yields are high enough to offset moderately rising interest rates, which can be viewed as a self insurance mechanism. This risk/return tradeoff is near its most attractive levels in 15 years.

High Yield bonds were the top returning category of 2024 due to their high coupon cashflow, relatively short duration, and a tailwind of tightening yield spreads. Emerging Market bonds offered the second highest return for the year, clearly rewarding risk takers in 2024.

Alternative Investments

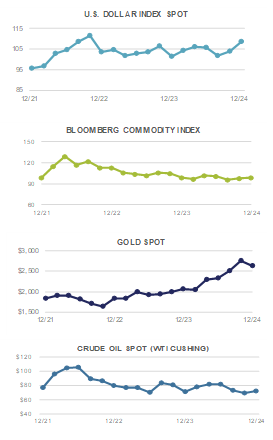

Alternative investments had mixed results in December. Broad commodities, as measured by the Bloomberg Commodity Index, were up +0.6% on the month but were roughly flat for all of 2024. There was varied performance within commodities during the year which makes the asset class difficult to summarize by one overriding force. The price of certain metals tumbled, such as iron ore and lithium, while other metals such as gold had strong performance.

Gold was slightly down during the month but was a standout performer among commodities in 2024, returning +27% for the year. Its strongest annual performance since 2010 was partially fueled by continued geopolitical risks, central bank demand, and Chinese consumer demand. Some investors are surprised to hear that the safe-haven metal outperformed the S&P 500 for the year despite all of the hype around AI within US Large Cap equities. In addition, the precious metal held up well despite a stronger US Dollar and rising Treasury yields which are classically thought of as headwinds.

US Natural gas futures surged +22.5% in December, primarily in the back-half of the month as the market anticipated a cold weather surge throughout the country in January. The new weather forecast, after a relatively mild autumn and start to winter, may fuel demand for heating and power generation.

Cryptocurrencies attracted headlines once again primarily driven by Bitcoin becoming more mainstream. Bitcoin’s price climbed over +100% in 2024 driven by a risk-on rally, potential deregulation efforts by President elect Trump, and Bitcoin ETFs being approved in January of last year. One Bitcoin ETF has grown to over $50 Billion in assets in less than a year, perhaps making it the most successful ETF launch of all time.

For more news, information, and analysis, visit the ETF Strategist Channel.