The agency MBS sector has emerged as one of the best relative valuation opportunities in the fixed income market over the past year. Given the stabilization in yields after the May FOMC meeting and the recent cooling of economic data, we believe agency MBS outperformance could continue.

Mortgaged-backed securities (MBS) are bonds backed by both the principal and interest cash flows of underlying mortgages, which are pooled and repackaged into interest-bearing bonds through a process called securitization. The mortgage cash flows are passed through to the holders of those bonds. MBS can be backed by both residential and commercial real estate mortgages that are issued either by a housing agency – Fannie Mae (FNMA), Freddie Mac (FHLMC), or Ginnie Mae (GNMA) – or private financial institutions, commonly referred to as non-agency. The MBS market is one of the largest and most liquid global asset classes, with more than $12 trillion of securities outstanding and over $300 billion in average daily trading volume. For this Notes from the Desk, we will be focusing on agency-issued residential mortgages.

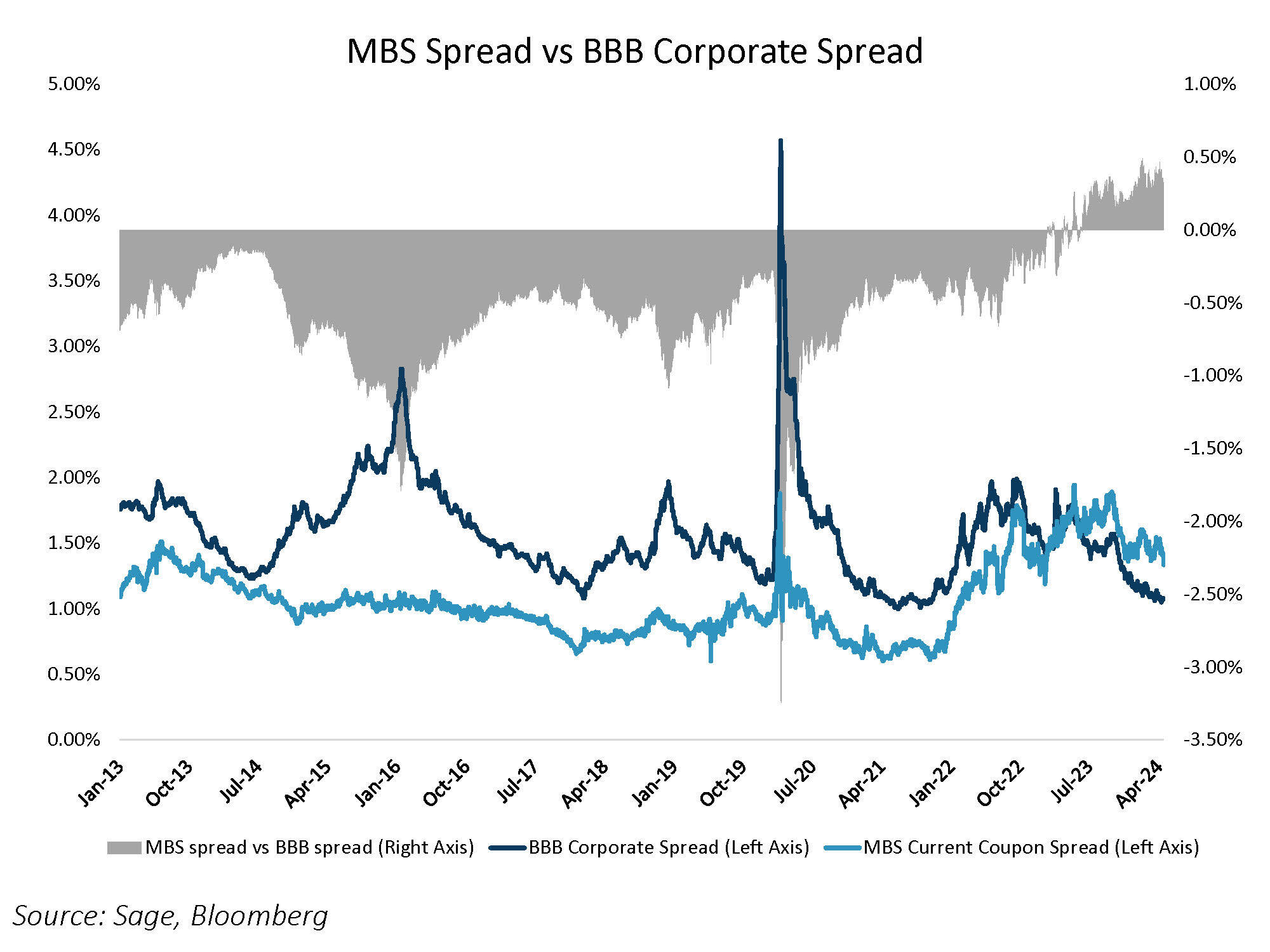

One of the features of agency MBS is that they have a government-backed credit guarantee from one of the housing agencies. While these agencies aren’t owned by the federal government, they are often seen as backed by it. Thus, agency MBS are not considered to carry any credit risk.

However, this doesn’t mean agency MBS are risk-free; there are three key risks associated with these bonds. First, prepayment risk is the possibility that mortgages within an MBS pool are prematurely paid back, which is detrimental to a bondholder as they would have lower future interest payments from the underlying home loans. The duration, or interest rate sensitivity, of an agency MBS would then get smaller as interest rates fall, and vice versa when yields rise, which results in MBS having negative convexity. The second key risk has emerged only in the quantitative easing era. As the Federal Reserve has been a large player in the MBS market, changing expectations around the Fed’s balance sheet policy has been a driver of MBS spreads. Third, US commercial banks are some of the largest buyers of MBS historically, and the regional banking crisis in 2023 has resulted in less demand for MBS, which has kept spreads elevated.

The chart below shows the current coupon MBS spread versus BBB corporate bonds. Despite having no credit risk, MBS are trading at a discount to the lower end of the investment grade corporate bond quality segment.

We continue to believe that the current valuation of agency MBS offers an opportunity to pick up a yield spread without taking on credit risk. As nearly 80% of mortgages have a rate below 5%, prepayment risk should not emerge as a key risk in the near term. Additionally, the FOMC has started to reduce the pace at which it is shrinking its balance sheet, which is a positive signal for MBS. Finally, the risk emanating from commercial banks should decrease as interest rates stabilize at or lower than current levels. The FOMC has all but ruled out interest rate hikes this year despite stronger-than-expected inflation in the first quarter, so the distribution of outcomes for interest rates remains skewed to the downside.

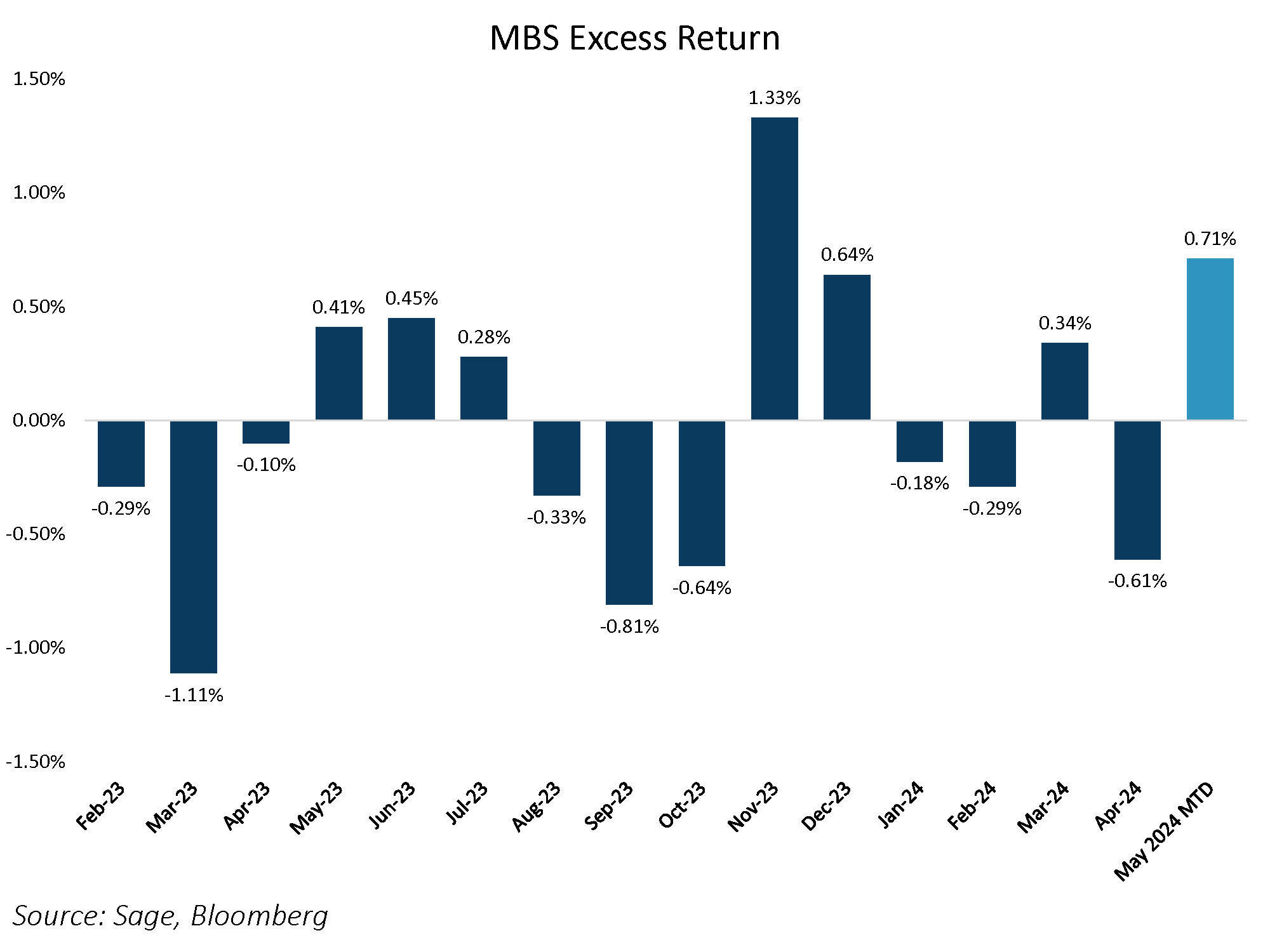

Since rate volatility decreased after the May FOMC meeting and recent data fell short of expectations, the agency MBS market has responded accordingly, with excess returns over treasuries reaching a six-month high. This trend may continue, as agency MBS valuations remain attractive.

For more news, information, and analysis, visit the ETF Strategist Channel.

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our web site at sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.