In 2023, we witnessed one of the narrowest equity markets over the last 100 years with only a handful of stocks holding significant sway in the S&P 500 Index. We view the recent broadening of equity market gains as a healthy development as the market has begun appreciating names that had been neglected last year and trading at attractive valuations. We expect this broadening to continue as economic growth persists in the near term.

Recent economic reports suggest first quarter GDP growth in the 2% range, which is a downshift from last year’s brisk pace but closer to longer-term trends. Continued labor market strength and persistent inflation-adjusted income growth lead our Recession Tracker model and offset a slowdown in consumer spending and sluggish industrial production. Furthermore, the Fed’s acknowledgment of diminishing inflationary pressures suggests rate cuts this year, which broadens the path to a soft landing.

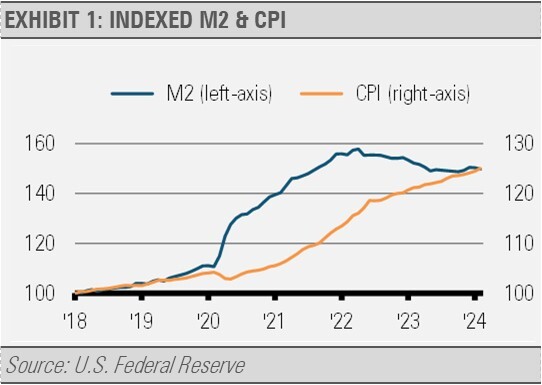

Just as the Fed lagged in addressing inflation, they now appear behind the curve in terms of rate cuts. We predicted the decline in inflation based on the relationship between money growth and inflation with inflation typically trailing changes in money growth by 12-18 months. As the excess pandemic era stimulus wanes, the rate of inflation is following the decline in money growth and prompting us to expect somewhat faster rate cuts than the Fed’s current forecast. While we do not expect prices to fall broadly, we do expect the increase to slow over time to a pace closer to the Fed’s 2% target.

Investors overallocated to money markets and T-Bills may witness a swift decline in interest income with Fed rate cuts. In contrast, those in intermediate-duration fixed income may experience more stable income alongside potential capital appreciation as interest rates decrease. We think that diversifying across fixed income maturities can be advantageous today.

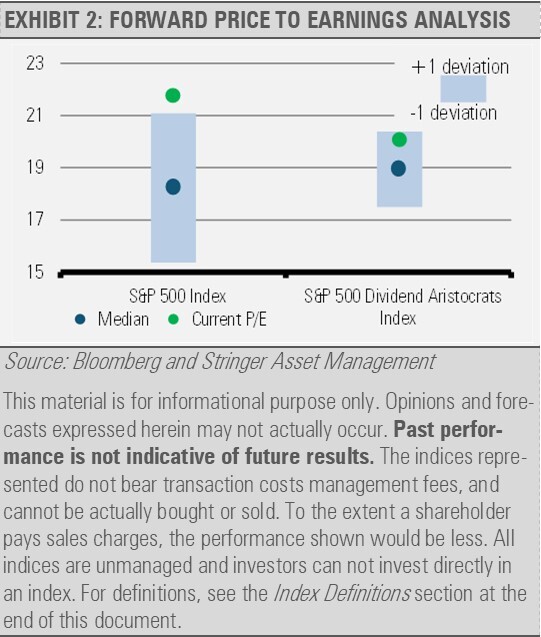

In addition, investors may want to focus on other areas for income, such as dividend-paying stocks. High quality dividend payers may increase their dividend payouts over time, which can help offset the eroding effects of inflation. Additionally, high-quality dividend-paying stocks trade at discounts relative to the broader market and only slightly above their long-term averages.

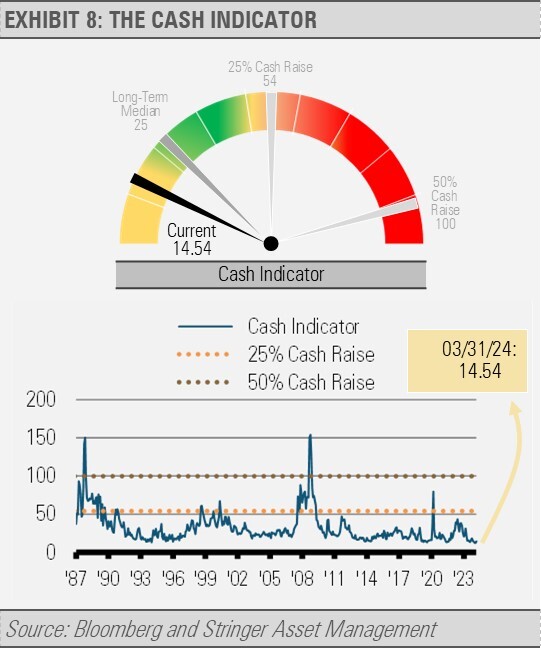

Considering the last several months’ lack of market volatility as measured by the VIX Index, the current calm may not persist. The recent low VIX levels rank in the bottom 20% of trading days over the last 30 years. Historically, low volatility periods have been followed by higher volatility that offers opportunities to acquire attractively priced equities. The VIX is a crucial component of our Cash indicator (CI) process and can be valuable during periods of heightened volatility.

In summary, while high money market rates may seem appealing today, they carry their own risks. Diversified intermediate-duration high-quality fixed income investments offer compelling income and the potential for capital appreciation. High-quality equities with dividend income potential are also attractive.

Additionally, investors should be prepared for opportunities to add to equity holdings in the coming months as volatility is likely to increase. Volatility can benefit long-term investors by providing opportunities to accumulate high quality assets at a discount.

Our long-term outlook is as optimistic as ever based on very healthy business and household sector fundamentals that we think will lead to solid economic growth for the next decade or more. Only the U.S. combines a large and growing labor force, a free, private sector to drive innovation, and deep financial markets to fund innovation and growth.

The U.S. is starting from a strong position in terms of industrial output and global competitive advantage. The U.S. leads global manufacturing in 7 of 16 categories, many of which are in the highest value-added industries, such as the chemicals and pharmaceuticals industry, the computer, electronic, and optical products industry, and the motor vehicles industry.

Global supply chain fragility was exposed by the COVID-19 pandemic. With the global trade order becoming more fractured and multi-polar, these weaknesses are now exacerbated. Manufacturers are becoming more focused on supply chain resiliency rather than optimizing efficiency.

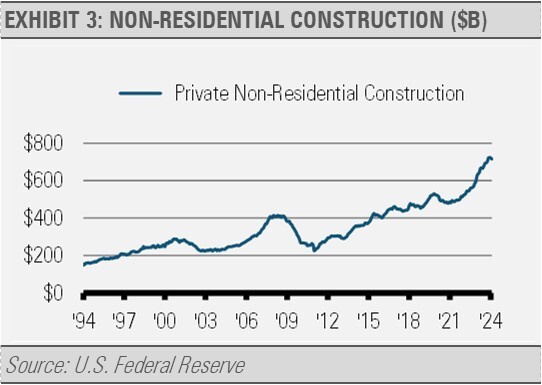

Largely because of these trends as well as government incentives, construction spending on manufacturing facilities has absolutely skyrocketed since late 2021, going from approximately $500 billion per year pre-pandemic to over $700 billion per year (exhibit 3).

At the same time, investments in research and development (R&D) are booming. According to The World Bank, the U.S. ranks first in total dollars spent annually, third as a percent of GDP, and fifth per capita. No other country comes close to these consistently strong rankings.

Productivity growth (innovation) is one of the keys to long-term economic growth, and R&D investments are crucial to increasing that productivity growth over time. Looking back at innovation breakthroughs over time, innovations in agriculture made farming more productive and allowed people to move off the farm and into the cities more than 100 years ago. Thirty years ago, it was automation in the factories and in business computers and software that made the workplace more productive just as the home PC and the internet made us all more connected. Fracking and associated technologies boosted U.S. energy output ten years ago, and that recently led to the U.S. becoming a net exporter of energy.

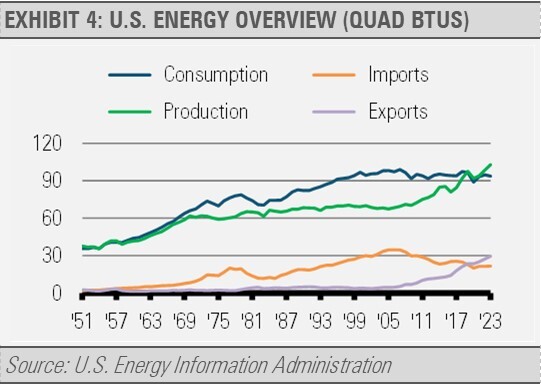

In fact, the U.S. energy sector is a timely example of the productivity boom that can follow R&D investments. As the following graph illustrates, energy consumption (demand) significantly outstripped U.S. energy production (supply) for years until the U.S. energy sector figured out how to significantly increase production through the development of new technologies.

Along with the increase in supply to meet and then exceed demand, energy exports also increased while imports decreased. This is a real-life example of how the theory behind capitalism and the open market works successfully.

Next up is the promise of artificial intelligence (AI). AI is likely to impact computer programming first, but also may make meaningful contributions to pharmaceuticals and other industries in the years ahead.

Combined with investments in plant and equipment and R&D spending, business investment is at an all-time high as U.S businesses are clearly prioritizing investment in the future. Not only is the U.S. labor force growing in an environment of economic freedom, but investments in new plant and equipment and R&D stand to make that labor force increasingly more productive. While near-term economic challenges persist, long-term trends in labor force growth, economic freedom, and business investment remain exceedingly positive.

Turning to the household sector, consumer spending makes up nearly 70% of U.S. economic activity, so the strength of household finances and household creation trends are key to economic growth.

Headlines abound that suggest a weakening of the U.S. consumer. Articles detailing persistent inflation, growing credit card usage, and an increasing number of past-due loan payments make things sound shaky. We think that historical context is necessary. Comparing current income growth rates, consumer debt-to-income levels, and delinquency rates to history suggests that personal income has been growing faster than inflation while households in general are only now getting back to normal debt-to-income levels after a period of massive government stimulus.

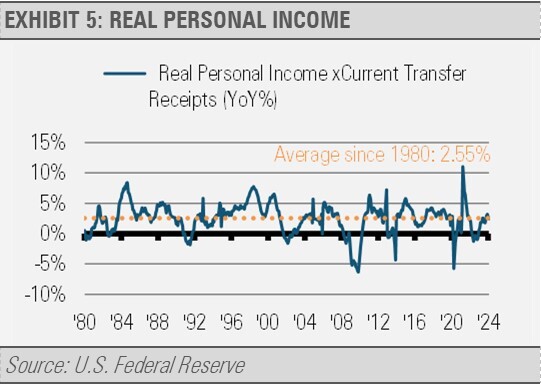

While inflation has certainly made for a challenging environment, less well documented is that real, inflation-adjusted income per worker has been growing persistently. In fact, income per worker has continued its uptrend and currently stands above the growth trendline going back to 1959. Workers on average are making more money than ever before even after adjusting for inflation. In our view, income growth above the rate of inflation continues to be very positive and bullish for the U.S. economy.

As the following graph shows, inflation-adjusted income growth is finally normalizing on a year-over-year basis after a wild ride since COVID-19 hit. After initially plummeting during the early stages of the pandemic, followed by a spike as the economy reopened and massive government stimulus took effect, and then a significant decline once again as inflation eroded income gains, the most recent data shows that real personal income growth has stabilized at close to historical norms for the last several months. As inflation normalizes over time, we expect a smoother path for inflation-adjusted income growth going forward.

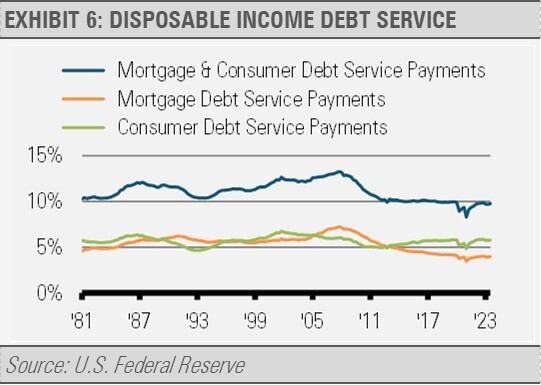

Looking at debt levels, the combination of mortgage and consumer debt as a percentage of disposable income was 9.8% in the third quarter of 2023, the latest data available. This has increased from the post-pandemic government stimulus backed days, which experienced the lowest debt-to-income levels in history going back to 1980.

Current debt-to-income levels are in line with the previous business cycle trend, which saw a great deal of household deleveraging. We note that these figures are still well below the 2001-2007 business cycle trough of 12.2% and also below the trough level of 10.4% in the 1990s and the trough of 10.3% from the 1980s. Increasing debt-to-income levels are only now just getting back to historical averages overall.

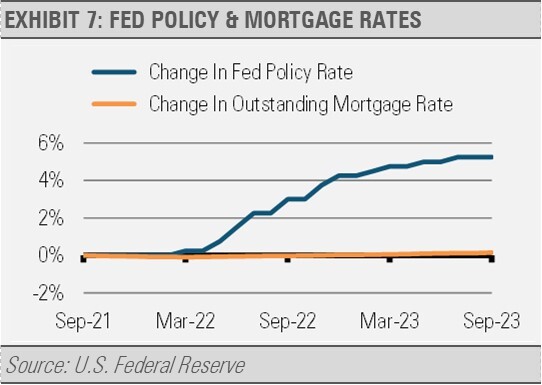

Meanwhile, U.S. homeowners took advantage of years of lower interest rates to further buttress their finances for decades to come. More than 90% of U.S. mortgages are fixed rate, which typically locks in interest rates for 15 or 30 years. We can see the positive long-term impact of these fixed rate mortgages reflected in the change in the average outstanding mortgage interest rate compared to the pace of rate hikes enacted by the Fed over the last two years. While the Fed has raised short-term interest rates by nearly 5.5% over the last two years, the average outstanding mortgage rate is up only 0.15% over that same period.

This is not to say that consumers are not at risk today. We are seeing worsening financial conditions for lower income households especially. In fact, according to the New York Federal Reserve, delinquency rates from credit cards and auto loans are still rising above pre-pandemic levels for lower income households. Younger and lower-income households are being hit especially hard by this financial stress. We will be watching these areas closely in the months to come.

Putting all this together leads us to believe that the U.S. is about to embark on a new era of economic growth driven by a growing and increasingly productive private sector.

CASH INDICATOR

The Cash Indicator (CI) has begun to levitate above its recent lows, which reflects an increased recognition of risk. However, the CI remains well below its long-term median. Readings this low have historically been reflective of complacency in the financial markets. Periods of complacency have normally been followed by increased volatility. With a relatively positive economic backdrop, we think that investors should be prepared to take advantage of increased volatility to add to high-quality core positions.

For more news, information, and analysis, visit the ETF Strategist Channel.