By Kostya Etus, CFA®, Chief Investment Officer, Dynamic Investment Management

Strong Labor Market and Lower Inflation

Ever since the Federal Reserve (Fed) began hiking rates to fight inflation, the market has been afraid of good economic data. The reasoning is that good data (such as higher consumer spending, increased industrial production and low unemployment) could lead to an overheated economy and thus, higher interest rates.

In 2023, that tune has changed as the Fed has signaled it plans to halt raising rates sometime this year. Now the focus has shifted, from guessing what the Fed will do, to the health of the economy and potential of a recession. This means that when good economic data is released, it’s well received by investors, and we’re no longer living in Bizarro World. The latest data:

- Jobs Report Shows Continued Strength in the Labor Market. The U.S. Labor Department reported that non-farm payrolls rose by 236,000 in March, in line with expectations. The unemployment rate remained at a steady 3.5%, while labor force participation hit a post-COVID high of 62.6%. Hourly earnings cooled to 4.2%, supportive of lower inflation going forward.

This is another jobs report which highlights continued economic resilience combined with easing inflationary pressures, all of which should be well received by the Fed and indicates we’re near the end of the rate hiking cycle.

- Annual Inflation Rate Slows for a Ninth Consecutive Month. The Bureau of Labor Statistics reported the Consumer Price Index (CPI), a primary measure of inflation, grew at an annual rate of 5.0% in March, below expectations. This is the lowest rate since May 2021 and a healthy drop from 6.0% rate in February.

Yet again, this is another sign we’re close to the end of rate hikes, and perhaps could see a return to a more easing monetary policy in the future.

Economy Remains Solid

Despite a strong labor market and falling inflation, there’s still uncertainty around a potential recession and more importantly, the severity of that recession. The unofficial scorekeeper of a recession’s start and end is the National Bureau of Economic Research (NBER), and they look at a variety of economic factors to make their determination.

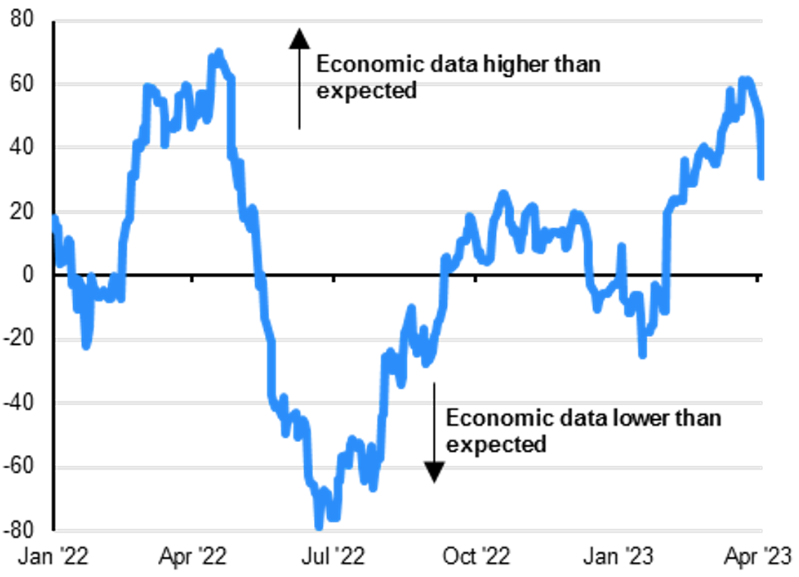

One way to get an aggregated view of economic health is to look at an indicator which combines a mix of variables. The “Citi Economic Surprise Index” chart, shown below, represents the sum of the differences between official economic results and forecasts. A reading of more than zero indicates that economic performance has been better than expected and vice versa for below zero readings.

Notice that conditions were quite weak in 2022, but how are we faring this year?

- Economy Started the Year Strong. At the end of March, the Citi index jumped to the highest level since April 2022, indicating that economic data have been beating expectations. Expectations are for solid GDP growth in the first quarter of 2023.

- Recent Indications Point to a Softening. We have had some more disappointments in April with softer than expected manufacturing and services numbers as reported by the Institute of Supply Management (ISM) Purchasing Managers Index (PMI).

- Economy Remains Solid. However, the overall level of the index is well above zero and the recent drop could simply be seasonal in nature. Given the continued labor market strength, lower inflation trends and the expectations for a more accommodative Fed in the future, the prospects of a less severe recession appear more likely.

Citi Economic Surprise Index

(2022 – Present)

Source: FactSet, J.P. Morgan Asset Management. As of 04/10/2023.

As always, Dynamic recommends staying balanced, diversified and invested. Despite short-term market pullbacks, it’s more important than ever to focus on the long-term, improving the chances for investors to reach their goals.

Should you need help navigating client concerns, don’t hesitate to reach out to Dynamic’s Investment Management team at (877) 257-3840, ext. 4 or [email protected].

For more news, information, and analysis, visit the ETF Strategist Channel.

Disclosures

This commentary is provided for informational and educational purposes only. The information, analysis and opinions expressed herein reflect our judgment and opinions as of the date of writing and are subject to change at any time without notice. This is not intended to be used as a general guide to investing, or as a source of any specific recommendation, and it makes no implied or expressed recommendations concerning the manner in which clients’ accounts should or would be handled, as appropriate strategies depend on the client’s specific objectives.

This commentary is not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Investors should not assume that investments in any security, asset class, sector, market, or strategy discussed herein will be profitable and no representations are made that clients will be able to achieve a certain level of performance, or avoid loss.

All investments carry a certain risk and there is no assurance that an investment will provide positive performance over any period of time. Information obtained from third party resources are believed to be reliable but not guaranteed as to its accuracy or reliability. These materials do not purport to contain all the relevant information that investors may wish to consider in making investment decisions and is not intended to be a substitute for exercising independent judgment. Any statements regarding future events constitute only subjective views or beliefs, are not guarantees or projections of performance, should not be relied on, are subject to change due to a variety of factors, including fluctuating market conditions, and involve inherent risks and uncertainties, both general and specific, many of which cannot be predicted or quantified and are beyond our control. Future results could differ materially and no assurance is given that these statements or assumptions are now or will prove to be accurate or complete in any way.

Past performance is not a guarantee or a reliable indicator of future results. Investing in the markets is subject to certain risks including market, interest rate, issuer, credit and inflation risk; investments may be worth more or less than the original cost when redeemed.

Investment advisory services are offered through Dynamic Advisor Solutions, LLC, dba Dynamic Wealth Advisors, an SEC registered investment advisor.

Photo: Lora Ohanessian, Unsplash