The chop-fest continues and dip-buyers go on strike.

By Eric M. Clark, Accuvest

The market has been quite volatile since the vertical ascent that ended 1/26/18. To reiterate from former commentaries, the move up in January felt very “forced and terminal” meaning the end of this part of the move seemed at hand. It doesn’t mean the bull market has ended necessarily, but it may mean that the recent chop-fest could continue for a while longer. For now, the market seems to be locked in a trading range which is likely frustrating both bulls and bears (“trend-less”). Sentiment is currently pretty bearish from my perch. Time will tell if the masses are correct. The S&P 500 Volatility Index (VIX) has now risen 40%+ in 5 trading days and the AAII Bulls to Bears ratio is down to 1.15 (contrarian bullish).

Markets are digesting a lot of new information: Less synchronized global growth, a new Fed chair in Jerome Powell, “gradually tightening monetary policy despite anchored inflation”, earnings estimates getting tougher to beat in future quarters, growth expectations being potentially too optimistic, and potential trade-wars and tariff rhetoric. Every steward of capital has to assess whether conditions are getting better or worse on the margin. It’s clear to us that currently, on the margin, things are LESS good and certainly more confusing than they were just a few months ago. That warrants holding some additional cash (>5%) and selling/trimming into rallies until global investors refocus on stable fundamentals versus the current political chaos rampant in Washington. I try and stay away from politics but I will make one observation: how we say something is often more important than what we say. Why our politicians, one in particular, have chosen to alienate our biggest and best trading partners in the manner in which they have, is a mystery.

Related: Stocks Soft Despite More Signs of Economic Oomph

Up until the last few days, the market as measured by the S&P 500 was indeed making slightly higher highs and higher lows (a good thing). For now, we are comfortable being long “core brands” while holding a tactical allocation to cash. Our current stance is this: he primary trend is still UP based on a purely technical assessment. Our experience indicates that prices will react to an economic and market top long before the actual fundamentals indicate a sever slowdown has begun. This stance dictates that a fully defensive or balanced posture is not currently warranted so long as we stay within the current 9 year price channel. In the near term, we anticipate the market will reach fully oversold levels within a few days which will warrant putting some cash to work on an opportunistic basis. It would be normal to re-test the February 9 lows to reinforce that level of support. It would not feel good, however. Plenty of damage has already been done.

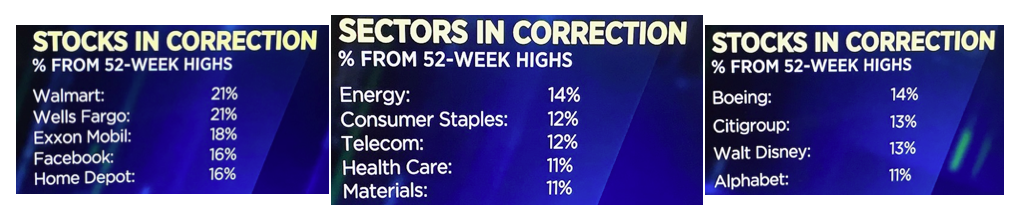

![]()

Source: CNBC

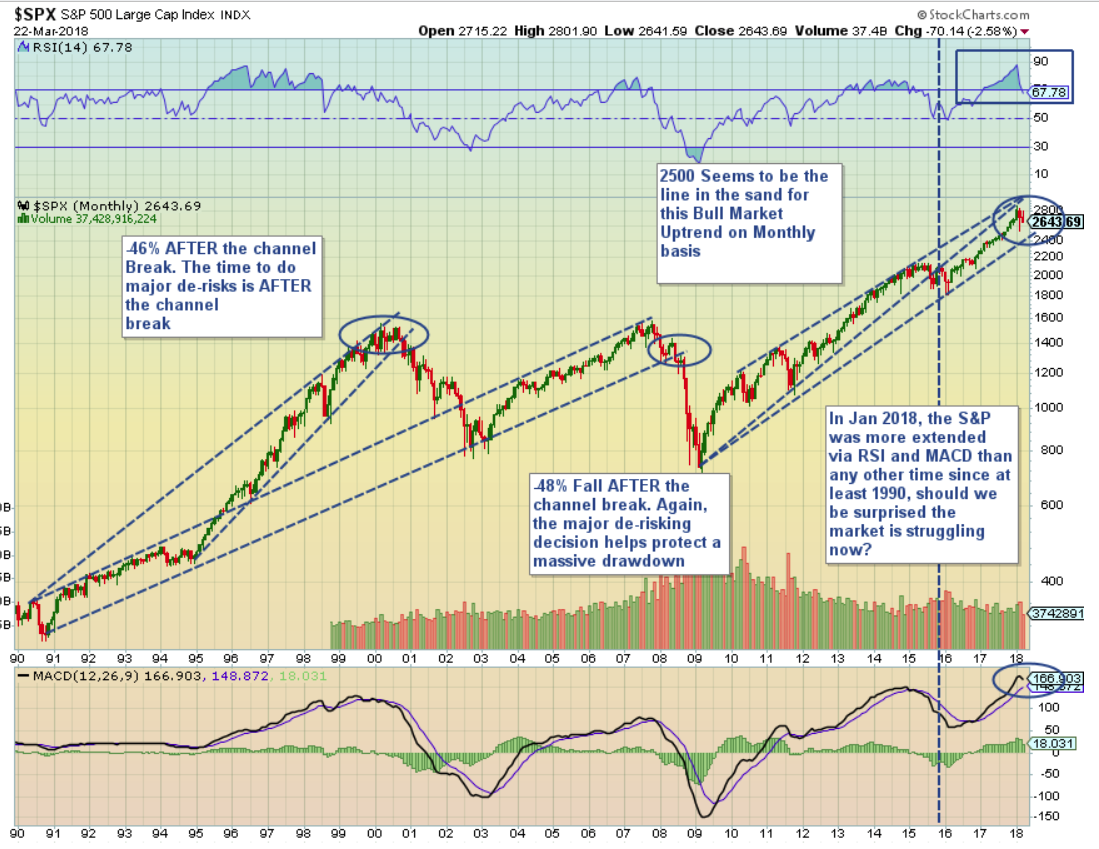

Current stock market status: The dominant trend is UP until we break the up-channel around SPX 2450ish.

Source: Stock Charts

Looking at the chart above we see something very important to remember: Bull markets eventually end when a well-established uptrend is broken to the downside. The chart is a monthly look-back at the S&P 500 Index via its ETF, SPY. There’s certainly room to fall given how extended we were in January but until this uptrend breaks on a monthly basis, we should give this bull market the benefit of the doubt and remain on a “buy the big dip” mode. If markets have “topped” in a major way and break the up-channel support ~2450 on the S&P 500, we would look to shift into a more balanced and defensive position. History has shown (chart above) the major drawdowns tend to happen after the up-channel has been broken. Our goal is to offer a smoother ride when corrections occur by holding higher levels of cash but the over-arching goal is to side-step the major drawdowns associated with recessions by de-risking in a more meaningful fashion once the major uptrend has been broken. Currently, that has not occurred.

It’s important to remember that fundamentally-driven humans, with a long-term plan, don’t seem to be driving the current price action in markets. Automated trading, Algo’s, dark pools, and “fast money traders” who trade on news, headlines, and technical levels are driving the bus so we must understand how they think, what levels they may trade against and when they may be programmed to cover shorts into panic. For active managers who pay attention to technical levels and try to buy high quality brands on sale, the current pullback offers significant long-term opportunities.

I won’t try and determine what exactly is driving prices lower today (Down -680 as I’m typing) other than to say that it’s 100% related to more sellers than buyers. I like to keep things simple. This too shall pass. In the meantime, we have our list of top brands to buy on sale, we have the cash to spend and we will wait for prices to come to us.

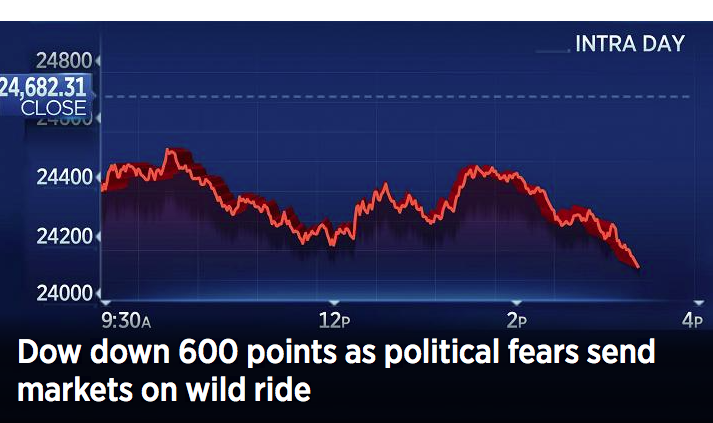

I’m waiting for the perfect buy-signal from CNBC, the “Markets in Turmoil” Show. Coming in 3.2.1

Source: CNBC

The time to be super bearish is when there doesn’t seem to be anything to worry about. As stated earlier, today we have plenty to worry about. Let us not forget though that volatility was abnormally low for the past 18 months so this return to VOL is a normal, albeit unwelcomed development. No one likes consistent volatility but from the perspective of an active, opportunistic manager, today’s environment offers wonderful tactical opportunities. We have the rare chance to own a portfolio of great brands with market-like beta without having to be fully invested. That’s an ideal scenario and the cash gives us optionality that most of our peers do not have. Most funds are too style-stubborn, cannot hold more than 5% cash, have no ability to de-risk to a greater degree and are anchored to fundamentals without paying any attention to market technicals. We prefer to listen to the message being sent through market prices and adapt to changing conditions. I’m licking my chops today but sitting on my hands for now.