As we go to press, U.S. equities have officially entered correction territory for the first time since the onset of the pandemic. Market volatility has spiked, with the CBOE Volatility Index (better known as the VIX) up more than +35% intra-day, and more than doubling year to date to a recent 36 (we started the year at 17.2). Angst over a plethora of issues is currently plaguing the market including higher interest rates, inflation, domestic politics, and geopolitics on the Eastern Front in Europe with Russia and Ukraine, amongst others. Which of these risk factors is precisely the culprit is hard to pinpoint, given the Federal Reserve signaled higher interest rates to come back on November 22. Investors may simply fear the Fed is further behind the curve than they admit, which may ultimately result in more aggressive, or more hawkish, monetary policy in months to come.

The fixed income markets have moved quickly over the past few months as the Federal Reserve has become less tolerant of high inflation readings and more comfortable with the employment rate. The Fed no longer views inflation as “transitory,” which means that instead of waiting for it to resolve itself, they are preparing to confront it head-on. This will be done by removing or lessening monetary stimuli, such as zero interest rate policy (ZIRP) and Quantitative Easing (QE).

In addition, we continue to experience pandemic-fueled supply chain disruptions, goods shortages, too few workers, and headline inflation hit an unattractive 7% in the most recent release. Some countries have again resorted to lockdowns during the recent Omicron wave, which will present an impediment to the speedy resolution of many of these issues.

Given the significant concern over policy changes, it becomes understandable that we may experience some market indigestion. There is even some anxiety that the first-rate increase will be larger than typical, a full half-percentage point instead of a quarter-point.

As of today, a non-telegraphed half percentage point rate increase is not a high probability. Unexpected policy changes are not well received and increase price volatility in the markets, as was experienced during the infamous “taper tantrum” in 2013. Chair Bernanke was less successful at clearly communicating his intentions to the market than our current Chairperson. Powell has learned from living through the impact of the 2013 miscommunication with the markets and has been very intentional about avoiding a replay of it.

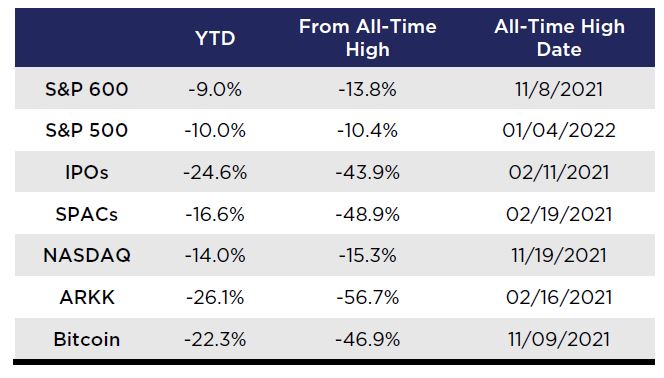

While it’s painful to see a sea of red in global equity markets, it’s important to put the recent volatility into perspective. Year to date, it’s the most speculative area of the market that has been most vulnerable to selling pressure.

Companies with no earnings, pipe dreams for revenue and profits, and those that just got plain expensive have all seen their share prices fall. Bitcoin has fallen more than -50% from its all-time high of $67,734. Not only has Bitcoin been cut in half, but it’s also been cut in half again, having lost more than -50% of its value, albeit from lower prices, on multiple occasions. Other areas of speculation, namely initial public offerings (IPOs) and special purpose acquisition vehicles (SPACs,) have taken a beating, down -24.6% and -26.1%, respectively, this year.

Source: Bloomberg, Nottingham Advisors. S&P 600 = IJR ETF, S&P 500 = SPY ETF, IPOs = IPO ETF, SPACs = SPAK ETF, NASDAQ = QQQ ETF, ARKK = ARKK ETF, Bitcoin = XBTCUSD. Performance represents unannualized total returns.

Technology has come under pressure, most notably from “innovation” names with sky-high valuations. Cathie Wood’s ARK Innovation ETF, up +152.8% in 2020, fell -23.4% in 2021, and is down another -25.7% YTD, highlighting the impact that discounting future cash flows at a higher interest rate has on equity prices. The NASDAQ 100, by comparison, is down -14.0% YTD.

From a fundamental standpoint, earnings season has thus far been robust, with 82% of companies reporting better than expected results. This week nearly 20% of the S&P 500 will report Q4 results, led by Apple, Microsoft, and Tesla. Visa and Mastercard report on Thursday which should be telling for consumer spending given recent choppiness in retail sales data.

Taken together, the recent correction in U.S. equities is probably overdue since March 2020, given cumulative gains of +52.4% from 2020-2021 inclusive of the pandemic induced drawdown. Perhaps investors waited for the calendar to turn the page before taking gains, or perhaps the market’s crystal ball sees higher interest rates and a Russia/Ukraine conflict more clearly than the rest of us. In the meantime, S&P 500 earnings are expected to be $220 in 2022 and $242 in 2023, meaning at a recent 4,300 on the S&P 500, Large-Caps trade for 19.5x this year’s expected earnings, and 17.8x next year’s estimates.

Looking ahead, all eyes will be on Fed Chair Powell on Wednesday afternoon. Any change to the Chair’s expected plan of action will be delineated as the Fed wraps up their January meeting. The market will be looking for Powell to provide clarity on the speed and magnitude of future hikes, all while digesting a slew of earnings releases over the coming weeks from the world’s largest companies. As geopolitics continues to take center stage, volatility may remain elevated, and we’ll be keeping our eyes open for opportunities as the dust settles.

Nottingham Advisors, LLC (“Nottingham”) is an SEC registered investment adviser located in Amherst, New York. Registration does not imply a certain level of skill or training. Nottingham and its representatives are in compliance with the current registration and notice filing requirements imposed upon SEC registered investment advisers by those states in which Nottingham maintains clients. Nottingham may only transact business in those states in which it is registered, notice filed, or qualifies for an exemption or exclusion from registration or notice filing requirements. For information pertaining to the registration status of Nottingham, please contact Nottingham or refer to the Investment Advisor Public Disclosure Website (www.adviserinfo.sec.gov). Any subsequent, direct communication by Nottingham with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

This newsletter is limited to the dissemination of general information pertaining to Nottingham’s investment advisory services. As such nothing herein should be construed as the provision of personalized investment advice. The information contained herein is based upon certain assumptions, theories and principles that do not completely or accurately reflect your specific circumstances. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. Adhering to the assumptions, theories and principles serving the basis for the information contained herein should not be interpreted to provide a guarantee of future performance or a guarantee of achieving overall financial objectives. As investment returns, inflation, taxes and other economic conditions vary, your actual results may vary significantly. Furthermore, this newsletter contains certain forward-looking statements that indicate future possibilities. Due to known and unknown risks, other uncertainties and factors, actual results may differ materially from the expectations portrayed in such forward-looking statements. Readers are cautioned not to place undue reliance on forward-looking statements, which speak only as of their dates. As such, there is no guarantee that the views and opinions expressed in this article will come to pass. This newsletter should not be construed to limit or otherwise restrict Nottingham’s investment decisions.

This newsletter contains information derived from third party sources. Although we believe these third party sources to be reliable, we make no representations as to the accuracy or completeness of any information prepared by any unaffiliated third party incorporated herein, and take no responsibility therefore. Some portions of this newsletter include the use of charts or graphs. These are intended as visual aids only, and in no way should any client or prospective client interpret these visual aids as a method by which investment decisions should be made. We have provided performance results of certain market indices for illustrative purposes only as it is not possible to directly invest in an index. Indices are unmanaged, hypothetical vehicles that serve as market indicators and do not account for the deduction of management fees or transaction costs generally associated with investable products, which otherwise have the effect of reducing the performance of an actual investment portfolio. It should not be assumed that your account performance or the volatility of any securities held in your account will correspond directly to any benchmark index. A description of each index is available from us upon request.

Investing in the stock market involves gains and losses and may not be suitable for all investors. Past performance is no guarantee of future results.

For additional information about Nottingham, including fees and services, send for our Disclosure Brochure, Part 2A or Wrap Brochure, Part 2A Appendix 1 of our Form ADV using the contact information herein.