By Bryan Novak

• Mega cap stocks have driven domestic stock market performance, by in large, in 2020. Might that be changing?

• Recent trends have seen changes in market segment performance such as small cap and value index performance

• Visibility into a COVID-19 vaccine may support a broader benefit for stocks, not just a few concentrated names

It’s hard to imagine in the year that has been 2020, after the deep collapse in risk assets in March, we would see such strong returns in any pocket of the equity market, especially when the U.S. economy and labor market have yet to recover to pre-pandemic levels. But that speaks more to the secular trend that has lifted not just technology stocks, but innovation segments. The U.S. and global economy were well entrenched in a techno-economic revolution, the likes we haven’t seen since the industrial revolution. This pump was primed and began well before COVID-19. The pandemic only exacerbated the differential between old and new economy. You can’t ignore this point, because in every short-term market move (the trees), there is a big picture to focus on that will drive value (the forest), and that is this.

There has been so much attention paid to mega cap tech and large/mega caps stocks, and for good reason. Return disparities have been great amongst broad equity benchmarks. Backers of the mega cap run use the backdrop I mentioned above to support further gains in this investment thesis. Naysayers, or mean reversion proponents, point to the few number of stocks that have been driving the majority of market returns, creating a wide disparity even amongst the major U.S. equity market indexes. This can be seen easiest in year to date returns (as of 11/13/20):

Source: Bloomberg Data: 1/1/20 – 11/13/20 Returns represent year-to-date performance of the specified indices through 11/13/20. An investment cannot be made directly into an index. Returns assume the reinvestment of dividends.

In Astor’s 2nd quarter conference call – we highlighted the discrepancy in returns between these stocks and the broader equity market. Despite the S&P’s strong rebound in the spring, many of the stocks that make up the S&P lagged the few mega caps heading into the third quarter.

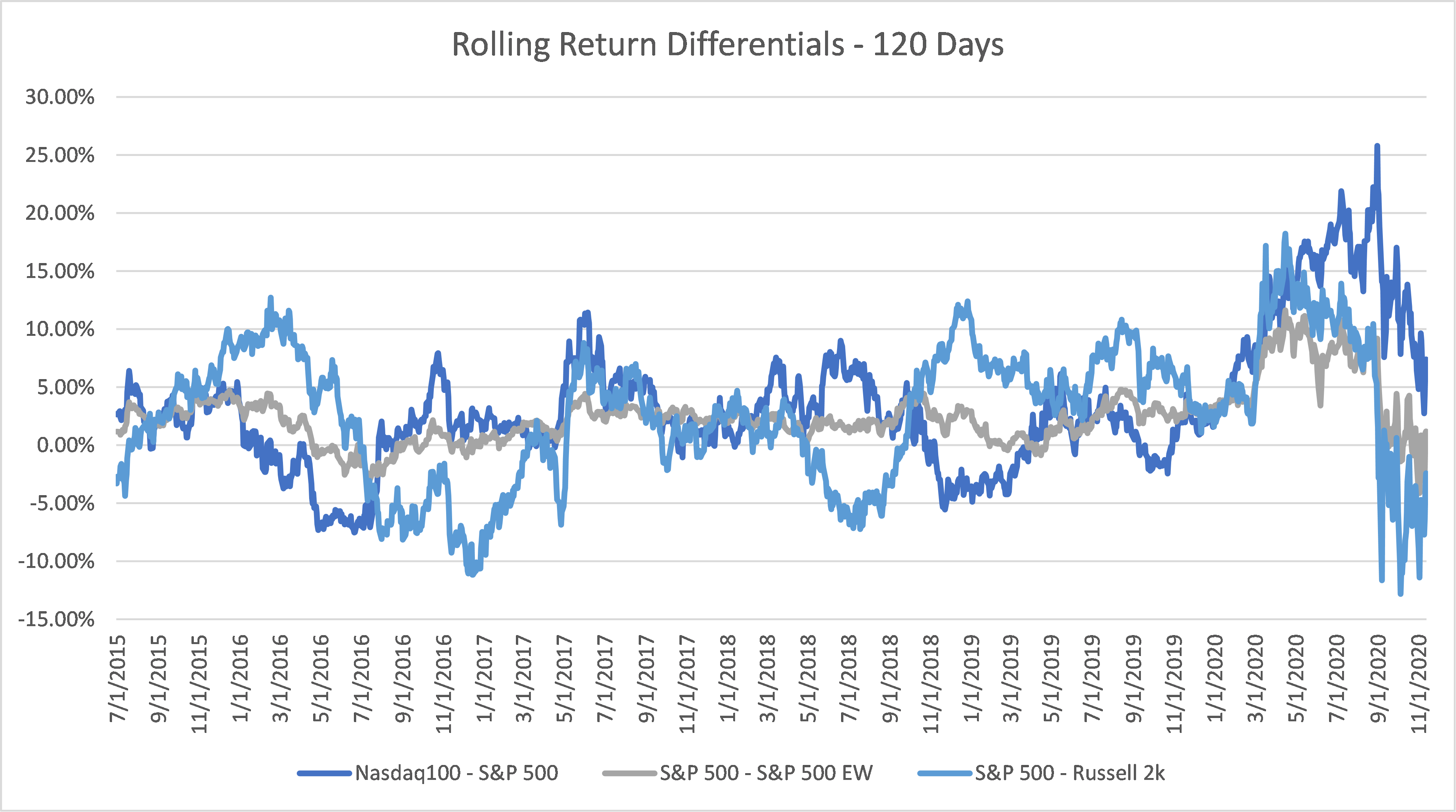

Q4 has suggested a shift in these relationships may be occurring as we move into year end. Moving past election date was one obstacle to clear from a volatility standpoint (certified results or not at this point). But more importantly, early last week and again to open this week’s trading, positive results from Pfizer and Moderna’s COVID-19 vaccine trials, separately, provided some clarity on the unknown for the economy. Looking at return comparisons between market caps and market weighted indexes, we can evaluate trends in these relationships. Coming into 2020, the trends had broadly been favoring the large and mega cap stocks for some time. This accelerated as the pandemic took hold. Tech and new economy companies (i.e.; video calling, online retail, cybersecurity), broadly illustrated by the NASDAQ Composite 100 Index, benefited from the prevailing new reality.

Chart 1

Source: Bloomberg, Astor Calculations Data: [7/1/2015 – 11/13/20]

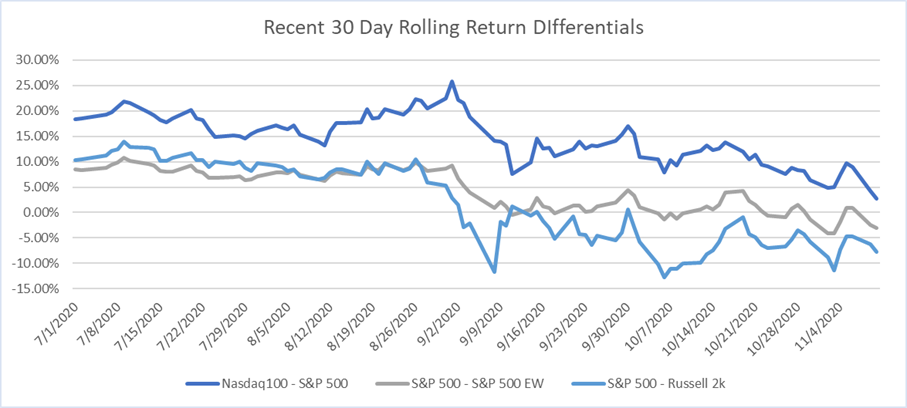

Chart 2

Source: Bloomberg, Astor Calculations Data: [7/1/20 – 11/13/20]

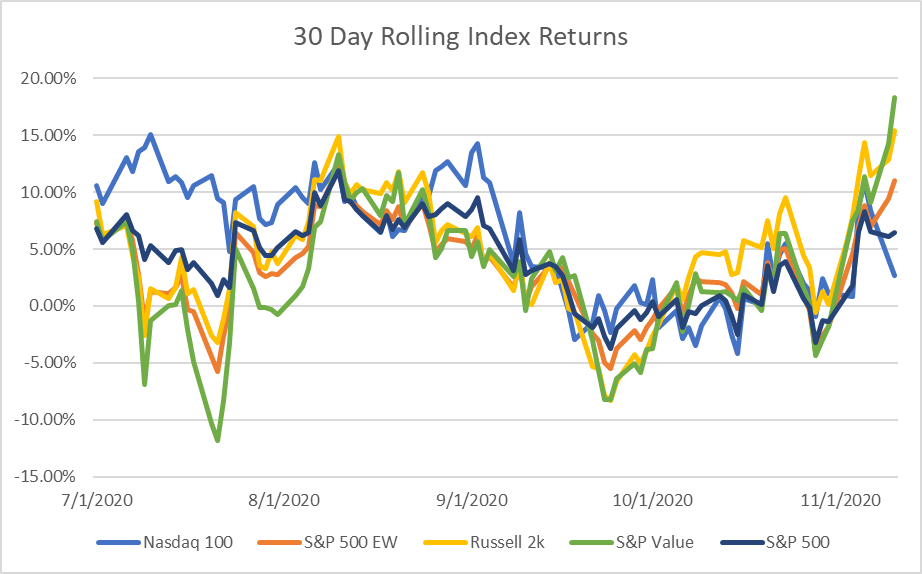

Source: Bloomberg, Astor Calculations Data: [7/1/20 – 11/13/20]

With a vaccine in sight (even if not here yet), the market has begun looking ahead for a move from the economy away from the stay-home model, even as the economy deals with the current reality pre-vaccine. We’ve seen an initial reaction that has favored value over growth, equal weight versus cap weight and small over large, all stemming from the same catalyst. Making wholesale changes against the competing backdrops may be a bit much, but we believe making complementary adjustments may benefit a portfolio in the long run.

DISCLOSURES

Astor Investment Management LLC (“Astor”) is a registered investment adviser with the Securities and Exchange Commission. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. Astor and its affiliates are not liable for the accuracy, usefulness, or availability of any such information or liable for any trading or investing based on such information. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results and no representation is made that a client will or is likely to achieve results that are similar to those shown. Factors impacting client returns include individual client risk tolerance, restrictions a client may place on the account, investment objectives, choice of broker/dealers or custodians, as well as other factors. Any particular client’s account performance may differ from the program results due to, among other things, commission, timing of order entry, or the manner in which the trades are executed. Clients may not receive certain trades or experience different timing of trades due to items such as client -imposed restrictions, money transfers, inception dates, and others. The investment return and principal value of an investment will fluctuate and an investor’s equity, when liquidated, may be worth more or less than the original cost. An investment cannot be made directly into an index. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services. Cap Weight: An index weighted across its constituents by the market capitalization size of each holding.

Equal Weight: An index weighted across its constituents equally, regardless of the market capitalization of each holding. Rolling Calculations: Refers to calculations where each data point is calculated by summing a set interval of past data points (e.g. 36 month rolling calculation would consist of 36 months of data at each point).The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points: including output and employment indicators. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. When investing, there are multiple factors to consider. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results. *The securities and weights represent the target allocations for the Dynamic Allocation strategy. Any individual investor’s portfolio may be allocated differently than presented here due to many factors, including but not limited to, timing of entry into the investment program, discretionary decisions by the clients and referring advisors, the structure of the invested product, custodial limitations, and/or the manner in which trades are executed. Securities and weights are subject to change without notice. The Dynamic Allocation strategy invests in Exchange-Traded Funds (“ETFs”). An ETF is a type of Investment Company which attempts to achieve a return similar to a set benchmark or index. The value of an ETF is dependent on the value of the underlying assets held. ETFs are subject to investment advisory and other expenses which results in a layering of fees for clients. ETFs may trade for less than their net asset value. Although ETFs are exchanged traded, a lack of demand can prevent daily pricing and liquidity from being available. Investors should carefully consider the investment objectives, risks, charges, and expenses of the ETFs held within Astor’s strategies before investing. This information can be found in each fund’s prospectus.

AIM-11/17/20-OP227