Last week, the long-awaited labor data showed a weakening labor market, but didn’t give clear signals for the Fed to cut rates by 50 basis points at the FOMC meeting next week. Nonfarm payrolls for August increased by 142k, below average expectation of 165k. Job growth for the prior two months was also revised lower, with June and July’s figures adjusted to 89k and 118k, respectively. This brings the three-month average job growth to 116k – weaker, but not yet in recessionary territory. The unemployment rate ticked lower to 4.2% while average hourly earnings surprised to the upside.

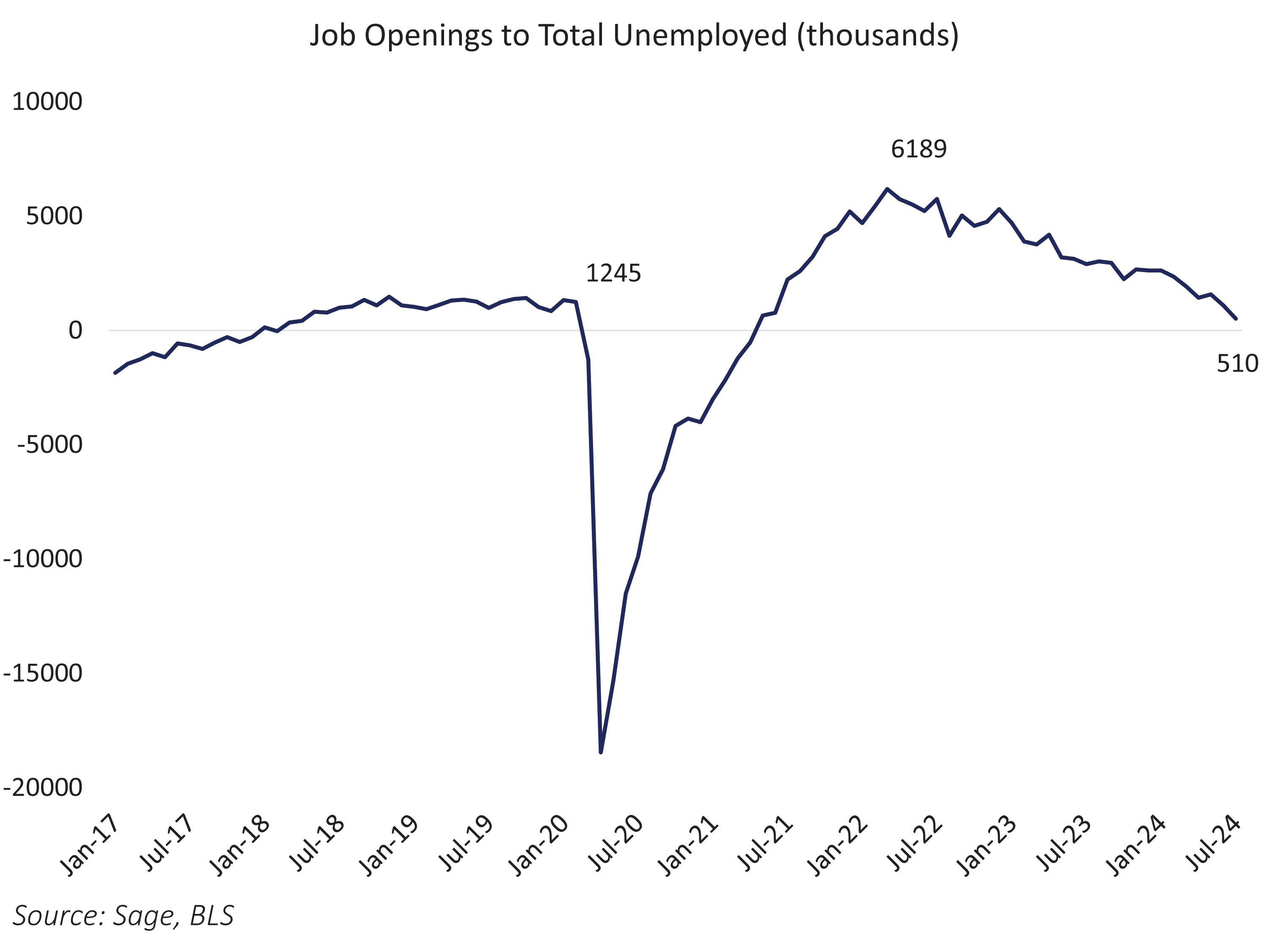

Job opening data continued to point to a slowing job market, with a total of 7.67 million jobs for July, below average forecasts of 8.10 million, while June’s print was revised lower to 7.91 million. The jobs-workers gap, which we define as job openings to total unemployed, is now approaching parity, with a difference of 510k in July. This is a significant change from the high of 6.2 million in 2022, and now well below the pre-pandemic levels.

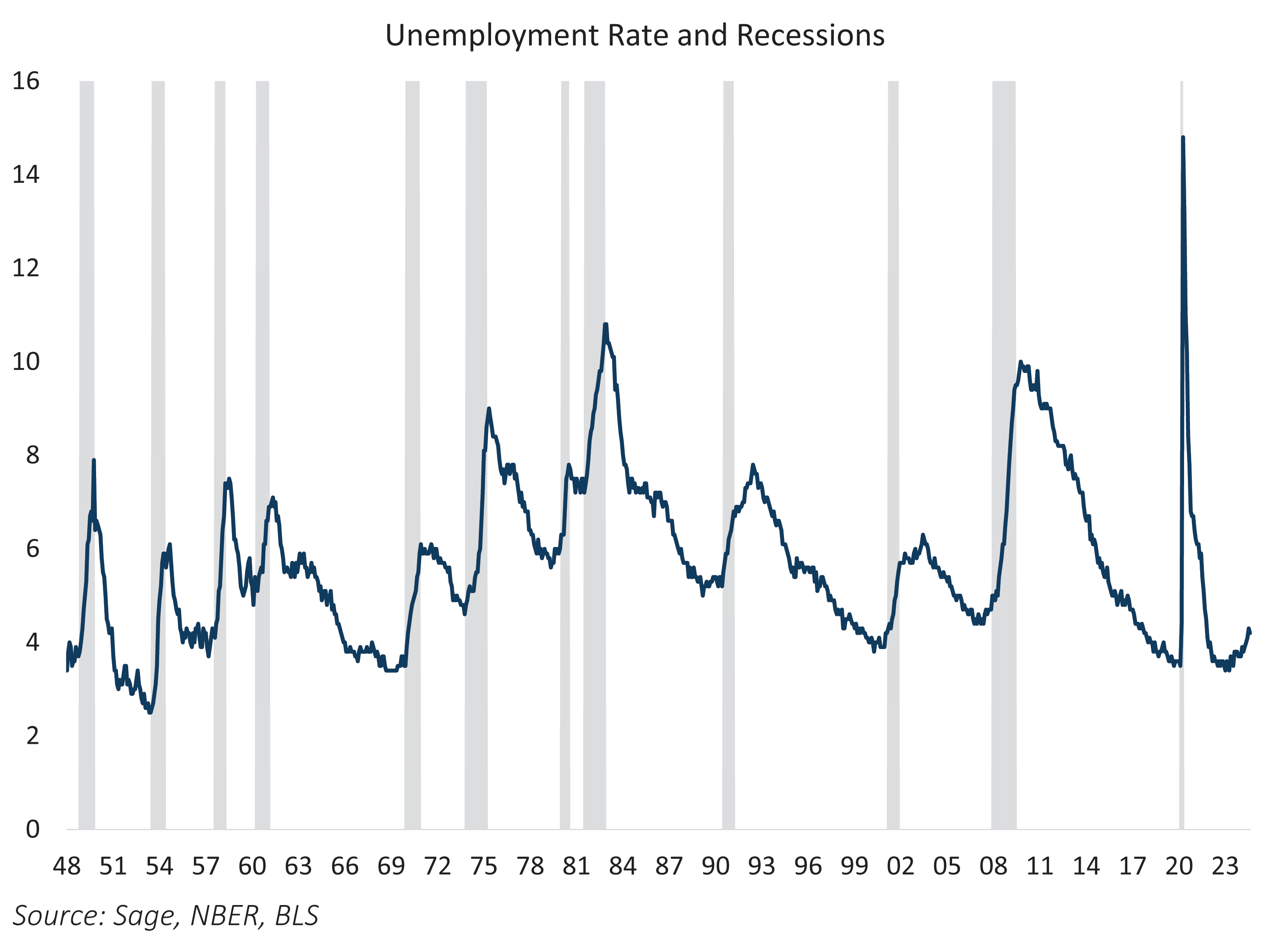

Labor market data shows a slowing labor market, but does the magnitude of the slowdown warrant a 50 basis point Fed cut at the September FOMC meeting? A simple way to address the question would be to look at the typical unemployment rate during past recessions. Over the past 12 recessions dating back to 1948, the average unemployment rate was 4.65% at the onset of recessions. The prevailing unemployment rate of 4.2% remains well below the average during the start of recessions, but not out of the realm of possibility in the near term which injects uncertainty into the Fed rate path.

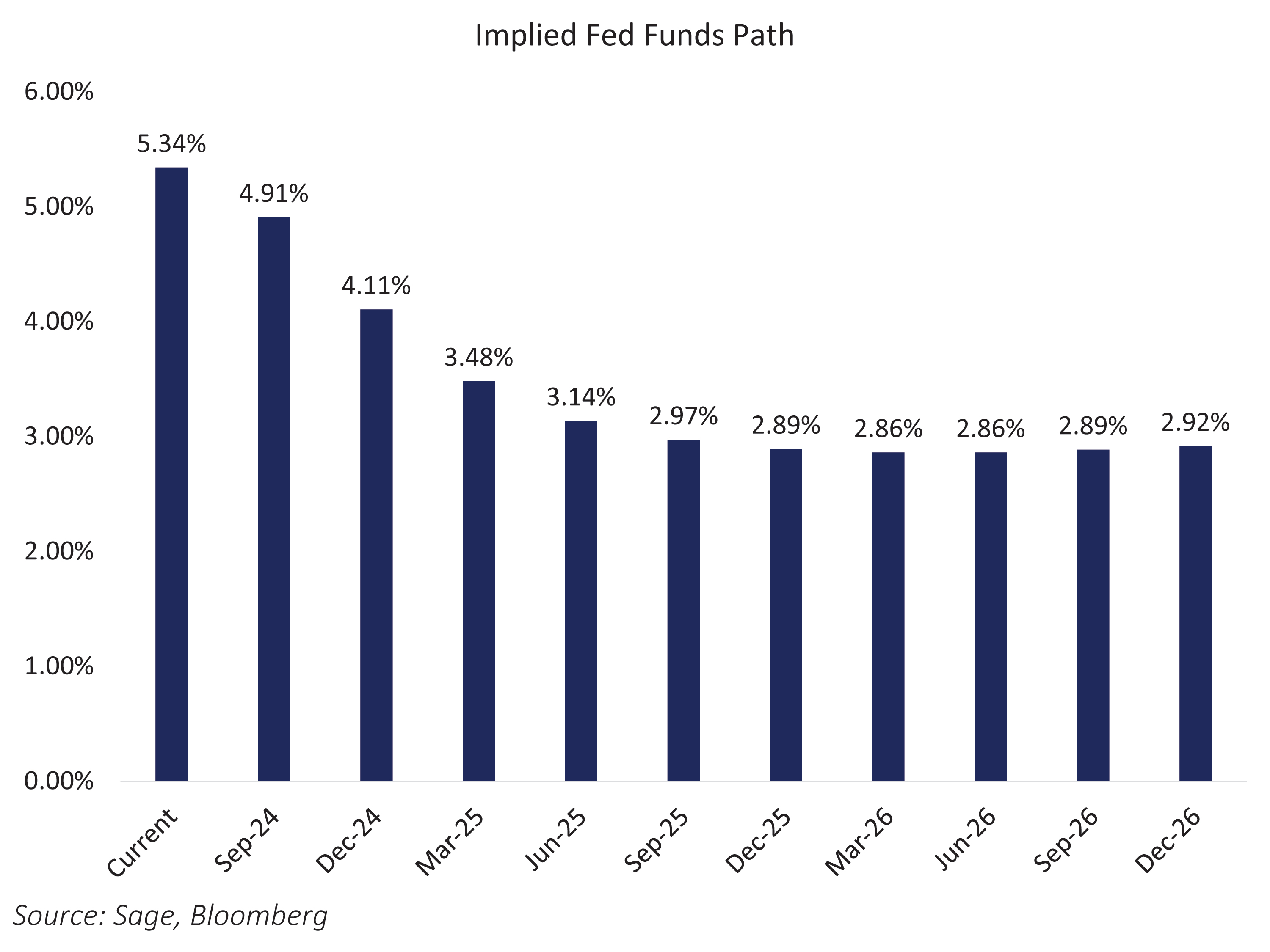

Market pricing of the Fed path reflects the uncertainty as to the magnitude of a rate cut in September and through the rest of the year. SOFR futures are discounting a larger-than 25 basis point rate cut at the September FOMC, and over 100 basis points of rate cuts through the rest of 2024. While the labor market is clearly slowing, we don’t believe the economic fundamentals justify a jumbo Fed cut in September and our base remains a 25 basis point rate cut at the September FOMC. The cost-benefit analysis of a 50 basis point rate cut is not clearly in favor of such a reduction, as the benefit of easing financial conditions should be weighed against the risk of sending the wrong message and spooking risk sentiment. This may result in a reflexive response from markets into economic confidence, which could flow through to put further pressure on economic growth.

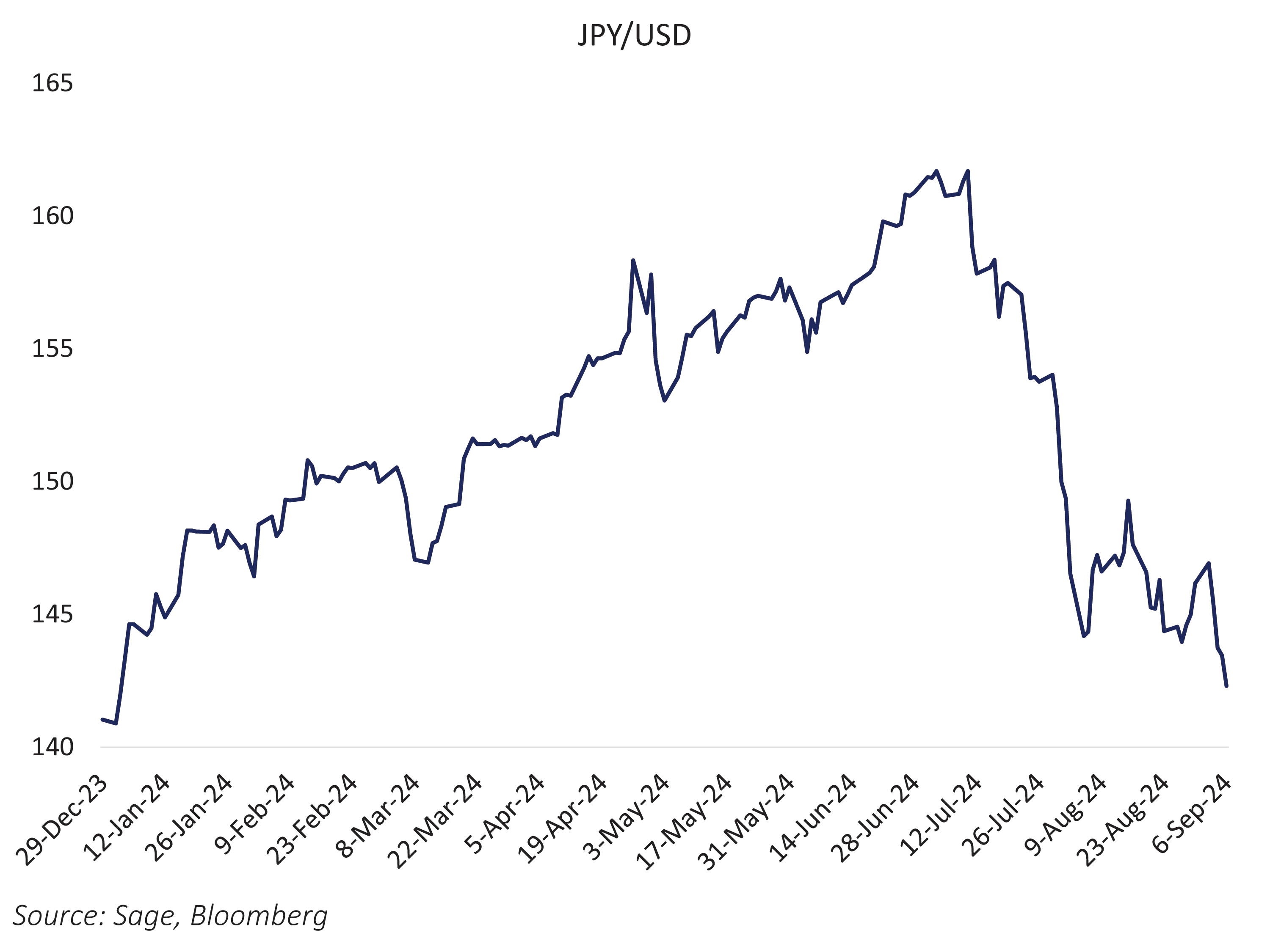

Outside of the Fed picture, markets still must contend with continuation from deleveraging as a result of the Yen carry trade. As we wrote in prior Notes, the unwind of the Yen carry trade was a catalyst for the volatility shock on August 5th, and the de-risking could still be occurring. The JPY have continued to strengthen past its level in early August, which could put pressure on further unwinding of risk across global investment portfolios, as risk positions funded by yen borrowing are reduced.

The labor market data last week did little to clarify the outlook for size of the Fed’s first rate cut of this cycle. While the labor market is weakening, it’s not clear that the Fed should opt for more than a 25 bp cut during the September FOMC meeting next week. A 50 basis point rate cut may present a less favorable cost-benefit scenario, as it risks sending a negative signal to market participants and the real economy. While we believe the risk to a larger yield shock is to the downside, interest rate markets could be in for a period of adjustment in the near-term as markets calibrate to Fed guidance at the FOMC meeting.

For more news, information, and analysis, visit the ETF Strategist Channel.

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our web site at sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.