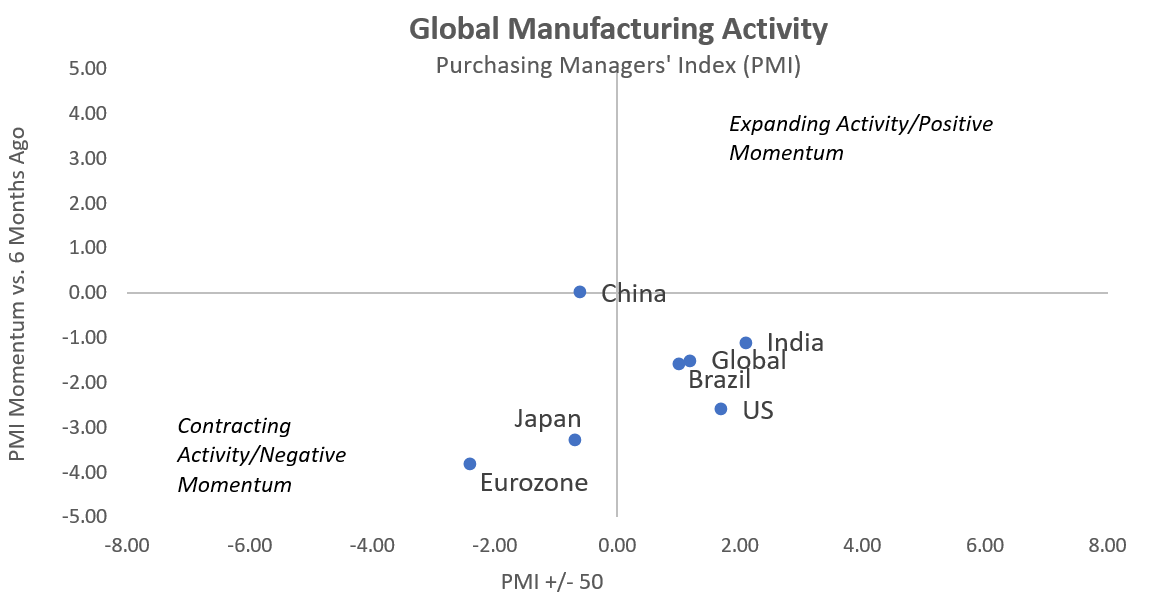

1. Manufacturing activity, which is a leading indicator for economic growth, has slowed down in nearly every major economy, especially Europe and Japan. The U.S. remains relatively healthy, but how much will the slowdown overseas seep into the U.S. economy?

Source: Bloomberg

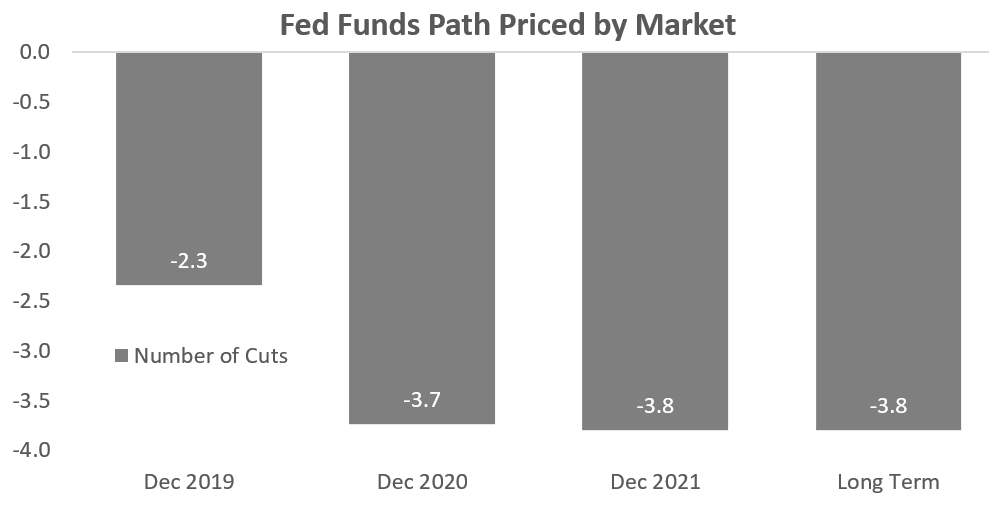

2. Slowing U.S. data and risks abroad, particularly trade, give the Fed the green light to cut rates. The market has priced in this expectation, with 4 cuts expected in the next 12 months.

Source: Bloomberg

3. Relative to fixed income, global equity valuations look attractive given the positive yield gap, and equities should benefit from continued monetary policy support.

Source: Bloomberg

4. Cyclical sectors (e.g., technology and materials) are favorable, as they are still lagging defensive sectors – even with the huge equity market rebound this year.

Source: Goldman Sachs

5. Central bank policy has become supportive again, which should underpin equities even as trade and other geopolitical risks increase volatility. Given strong returns, weaker overseas data, and rising trade concerns, attractive segments include U.S. large-caps, and the quality, value, and high-dividend markets.

Source: Bloomberg

For Sage’s Fixed Income Outlook in 5 Charts, click here.

This article was written by the team at Sage Advisory, a participant in the ETF Strategist Channel.

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our web site at www.sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.