By Nicholas Porter

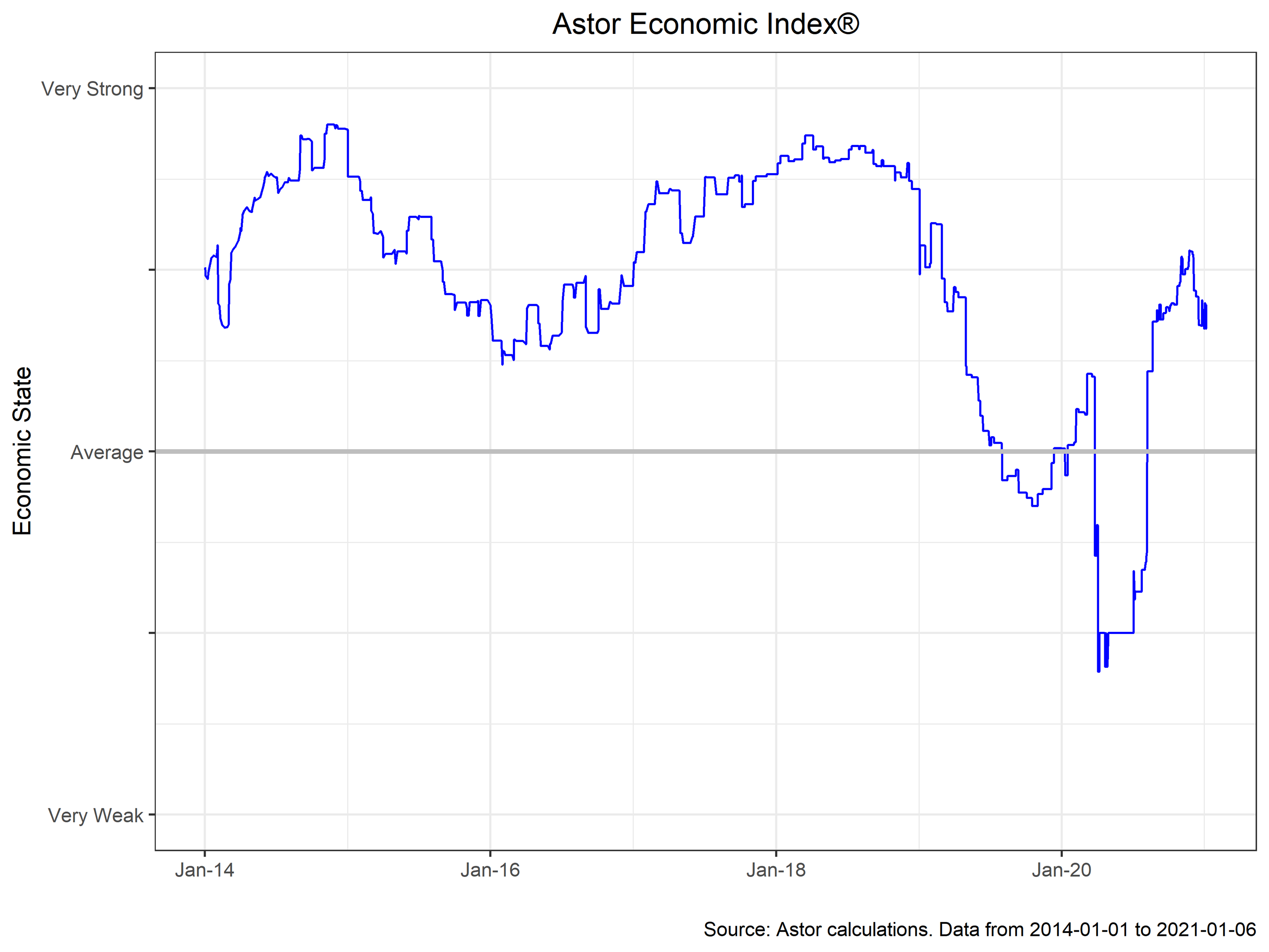

With COVID-19 still spreading throughout the United States, the Astor Economic Index continued its weakening trend in the month of December, ending the quarter down from its peak several months ago but still well into solid growth territory.

Nonetheless, as we look ahead to 2021, there are several reasons to be optimistic. First, more stimulus is likely on the way, with the Biden administration proposing $1.9 trillion of additional government spending. Importantly, much of the proposed aid will directly boost consumer’s wallets, with a potential for $1,400 stimulus checks, rental assistance, a new small business grant program, expansion of the Earned Income Tax Credit and supplemental unemployment benefits. Aid for local and state governments would be an additional tailwind for the economy.

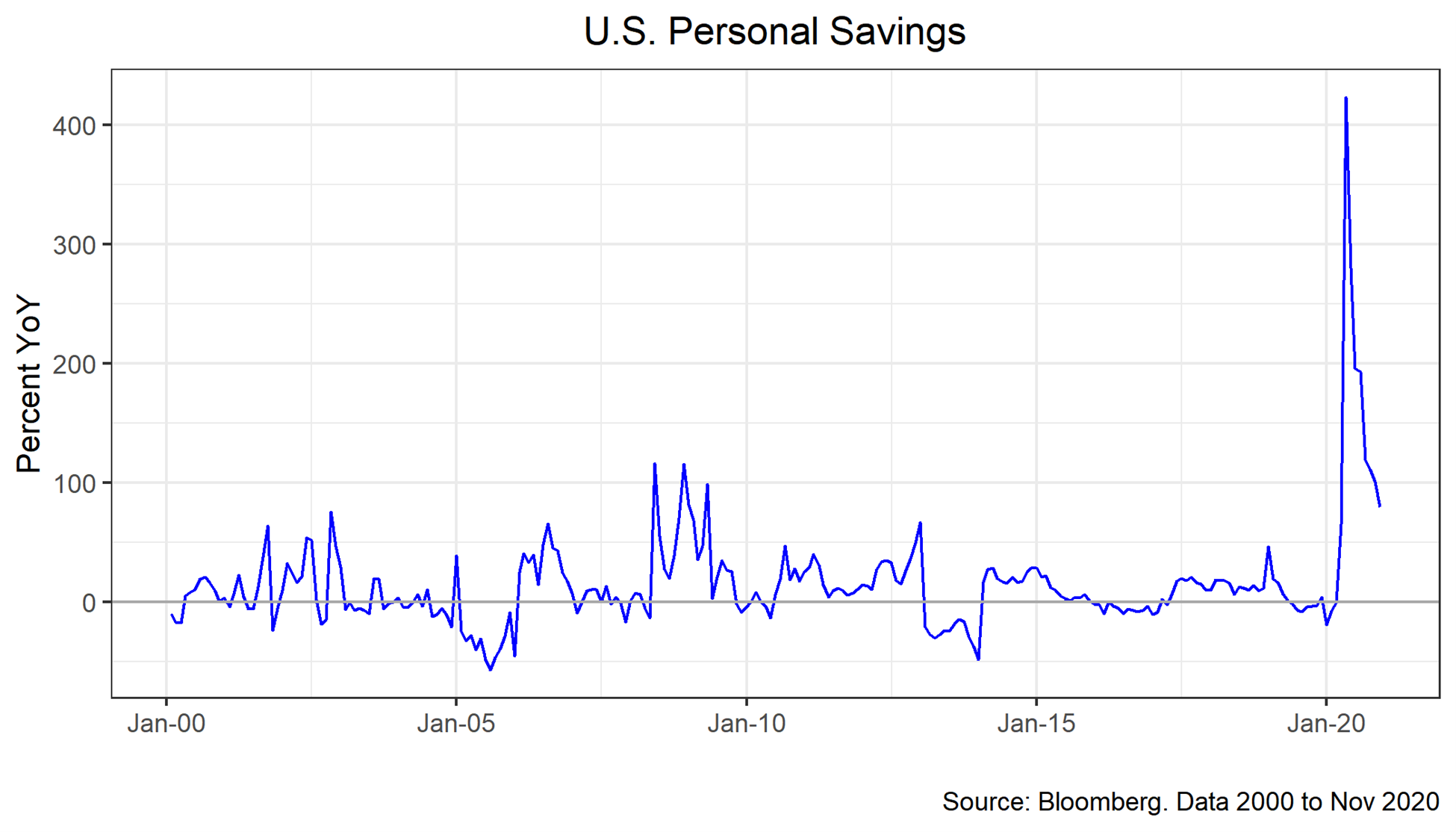

Second, even absent further stimulus, consumer and corporate balance sheets are well positioned to capitalize on a reopening economy and leads credence to the belief that the closing of the output gap will be quicker than previous recessions. U.S. personal savings (household disposable income less consumption) are artificially elevated by weak spending but nonetheless indicate flush households.

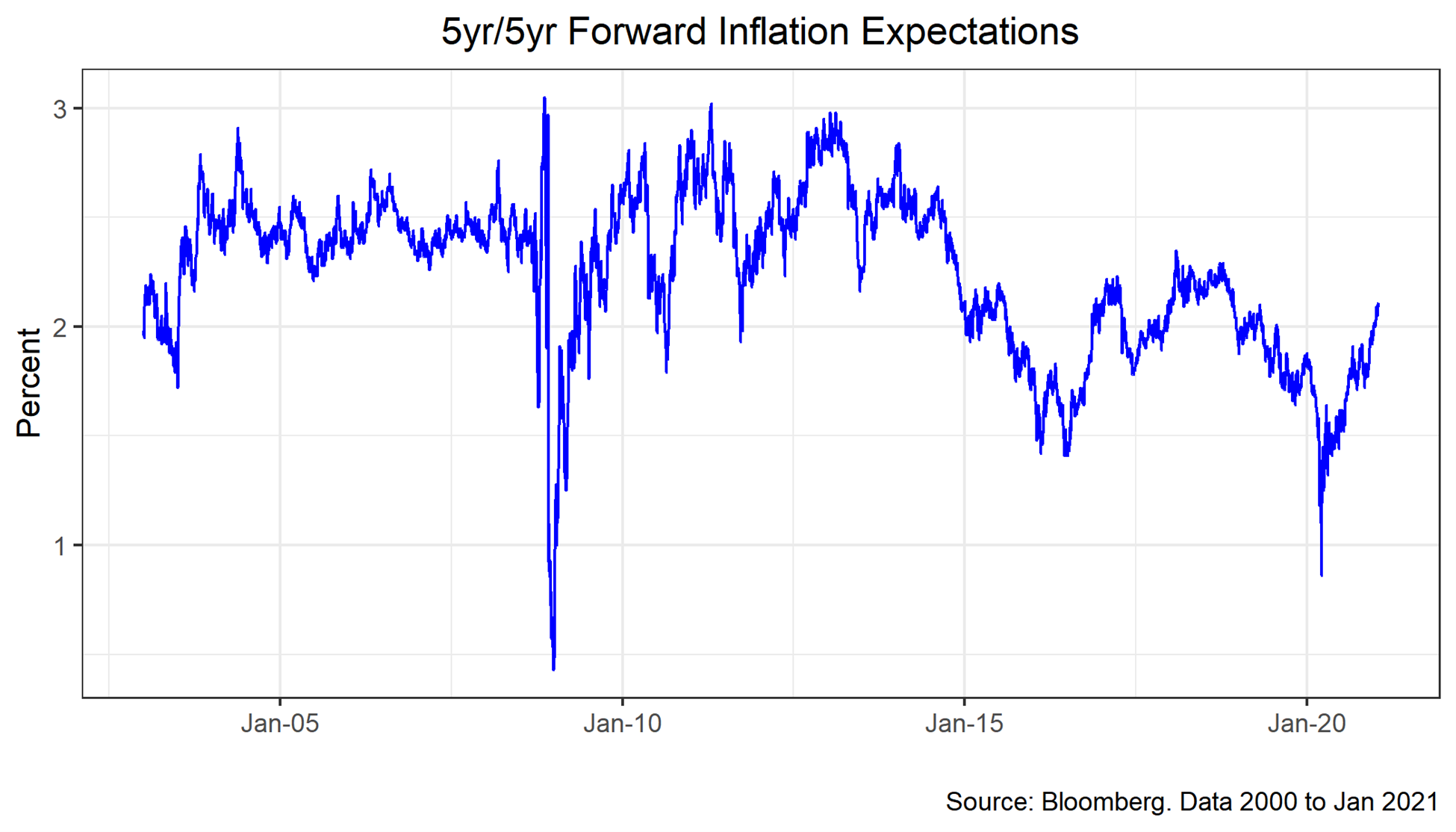

Of course, consumers primed to spend coupled with a constrained supply chain bring about concerns of above trend inflation. Market participants have been squarely focused on the prospect for rising inflation and the potential balancing act between increased growth and a hotter or overheating economy. Inflation breakevens, a market-based measure of inflation expectations, have steadily ticked higher. Similarly, 5-year 5-year forward inflation expectations (a measure of average inflation over five years, five years from now) have steadily moved up throughout 2020 and now sit above 2%.

For now, however, core PCE is low at 1.37% YoY, and real rates are low. In sum, the U.S. looks well positioned to return to solid growth in the second half of the year, but we will closely watch the data for any nascent signs of above trend price pressures as well as continued deleterious effects from the pandemic that may prove to be persistent.

The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points: including output and employment indicators. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. When investing, there are multiple factors to consider. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. The Astor Economic Index® is a tool created and used by Astor. All conclusions are those of Astor and are subject to change.

AIM-12/17/20-OP248

All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. Astor and its affiliates are not liable for the accuracy, usefulness or availability of any such information or liable for any trading or investing based on such information. Please refer to Astor’s Form ADV Part 2 for additional information regarding fees, risks and services.