SUMMARY

- We believe bull markets inevitably involve corrections.

- In our view, a ‘healthy’ correction is one where pullbacks are contained to less than half of the advance.

- We believe the markets are going through a ‘healthy’ correction, but we remain vigilant as these important levels are being tested.

Ukraine Tensions and Higher Rates Will Likely Decide

Market declines are no fun, but volatility is part of the process of being a stock owner. Sometimes market declines can be viewed as a healthy part of a bull market, and other times they are the start of bear markets. Today we will try and examine the differences. A legendary trader, Larry Hite famously said he had two rules: “If you don’t bet, you can’t win…if you lose all your chips you can’t bet”. We agree with the premise which is why risk-taking and disciplined risk management are embedded into RiverFront’s processes.

Healthy Corrections

One good rule of thumb we abide by is that the steeper the trend, the bigger the reversal. We think corrections are best judged as a percentage of the advance. If an asset corrects by a quarter or a third of its advance, and the uptrend remains in place, then we would generally regard that as ‘healthy’. More challenging, from a longer-term perspective, is an asset whose trend is unsustainably high to us, where optimism is universally

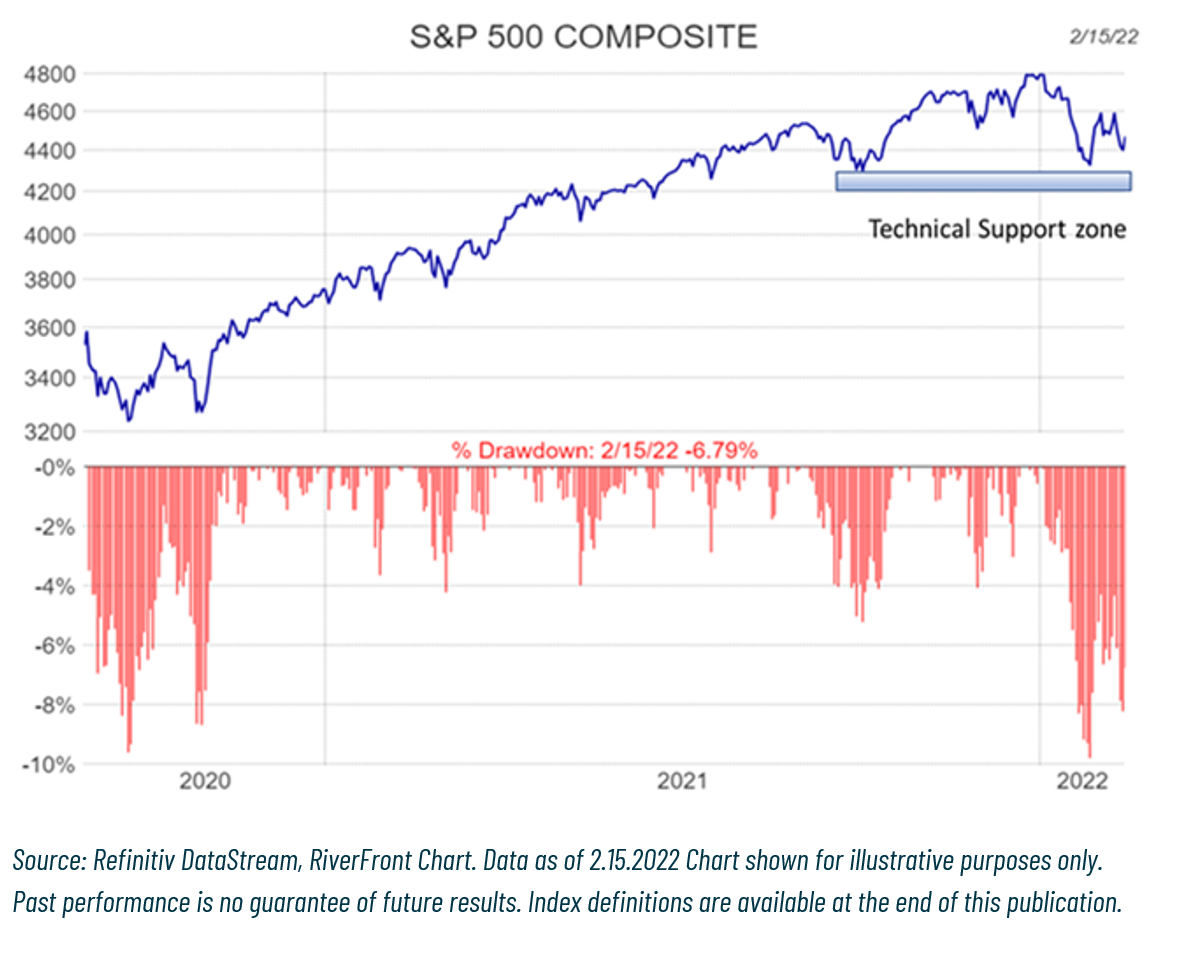

pervasive, and fundamentals deteriorate. Remembering RiverFront’s rule of ‘Beware the Crowd at Extremes’, we become more cautious when optimistic sentiment becomes extreme. All these scenarios are generalizations, so let’s see how this applies to today’s stock market. Using round numbers, the Standard & Poor’s (S&P) 500 Index broke decisively above its pre-COVID-19 high of 3400 in November of 2020 and then rose in a powerful move to its January 2022 high of 4800 – a 41% advance in 14 months (see chart above). More remarkably, the largest drawdown during this advance was just 5% in September of 2021. We believe that the current decline warrants close attention from a risk perspective since recent decline to 4300 is the first significant correction since the summer/fall of 2020 and so far, has retraced just over a third of the advance. If the S&P 500 can find a low around 4200 and build a base for another advance to new highs, then we describe this as a ‘healthy’ correction. Thus far, what we think has occurred is a normal pullback in the context of the rapid rise in stock prices since the low in March 2020.

Bear Markets

One widely used definition of a bear market is a decline of 20%. We agree, but also believe there is a time element. We think a relatively sharp 20% decline followed by a return to new highs, within a few months, has a very different psychological effect than one that lasts a year or more involving multiple drawdowns. Also, a market that has doubled, then loses 20%, is a different scenario from one where a 20% decline wipes out a year or more of gains. Applying this thinking to today’s situation means we suggest being less focused on the magnitude of the decline and more on how much of the advance is given back.

Ignore the Noise, Smooth Out Returns

At RiverFront we like to focus on the S&P 200-day (50 week) moving average as a means of measuring the primary trend. We believe it smooths out returns and cuts through the normal headline noise. In the chart (left) we show the S&P 500 in black and the 200-day moving average in red. As you can see, this moving average barely dipped in the first quarter of 2020- the decline and recovery was so rapid. In a secular bull market such as we have seen from 2009, the moving average has only dipped a few times. What occurred in these incidences was very different from the prolonged decline in 2008/2009 or in the early 2000’s which were clear bear markets, in our view. When the moving average is falling (not the case today) or important levels are breached, our risk management process is on especially high alert, and we must make tactical judgments as to whether to take action.

To the extent that you can, we encourage investors to focus more on the primary trend and less on the week-to-week movement of the market. Imagine if your monthly statements were based solely off this average and the media only reported the change in the moving average. Your returns would seem so much less volatile.

During 2021 we often wrote that the pace of the 200-day moving average was unsustainable and would likely level off at some point. We believe this is what we are seeing now with the latest slope of the 200-day falling to a +9% rate. For us to consider this to be a ‘healthy’ correction, we would like to see the 200-day moving average behave similarly to its 2018/2019 pattern (see circle on chart above). This is the last time the Federal Reserve (Fed) raised rates. This would allow the index to reset in preparation for a move to new highs later this year.

The Fed’s policy response to inflation (which we have written about extensively), and geopolitical tensions are two important components in this decision. The situation in the Ukraine is evolving quickly and potentially increases longer term inflationary pressures. Our team will be evaluating the latest move by Russia to support the annexation of two states in eastern Ukraine and monitoring the response from the West. There are lots of crosscurrents causing volatility right now, both good and bad (see last week’s Weekly View: Macro Economic Cross Currents Make for a Choppy Start to the Year) and we will weigh these in the coming weeks and make changes if we see the need.

For investors approaching or in retirement, what we refer to as the Sustain and Distribute phases, recent events reenforce the importance of maintaining balance in accordance with a predetermined strategy. For those in the Accumulate phase, we reiterate our advice that investors should look on these types of corrections as part of the journey and as opportunities to add to their portfolios at lower prices.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

Technical analysis is based on the study of historical price movements and past trend patterns. There are no assurances that movements or trends can or will be duplicated in the future.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

For each outcome category (accumulate, sustain, and distribute) RiverFront’s portfolio management team has assigned one or more RiverFront product(s) based on their assessment of the product’s investment objective as it relates to a typical client’s return and risk objectives when seeking investment outcomes of accumulating wealth, sustaining wealth and distributing wealth. The team has also designated RiverFront product alternatives for those clients looking to take more or less risk with the outcome category. The ‘more aggressive’ (or more risk) alternatives will generally have greater equity and international exposure as well as longer time horizon targets, while those designated as ‘more conservative’ (or less risk) will have fewer equities, a lower exposure to international and shorter time horizon targets. Since the risk assessments are dependent on the outcome category selected, RiverFront products may fall in multiple categories. All investments carry a risk of loss and there is no guarantee that an investment product or strategy will meet its stated objectives.

Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

In a rising interest rate environment, the value of fixed-income securities generally declines.

Definitions:

Beware the Crowd at Extremes – Terms correlate to the NDR Crowd Sentiment Poll and its measurement of Extreme Optimism (Bearish), Neutral, or Extreme Pessimism (Bullish).

Index Definitions:

Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.RiverFrontig.com and the Form ADV, Part 2A. Copyright ©2022 RiverFront Investment Group. All Rights Reserved. ID 2049605