Cash and ultra-short fixed income investors continue to enjoy the fruits of nine Fed rate hikes. Yields on cash hover around 3% with relatively low interest rate sensitivity. However, with the Fed done raising rates, core yields now 60 basis points lower than six months ago, and the economy in the later part of the cycle, bond investors who tactically shifted to cash and ultra-short allocations should start to think about whether or when to extend out the curve. The decision to extend duration to a short or intermediate duration strategy depends largely on an investor’s expectation for the yield curve.

What is curve telling us and where does it go from here?

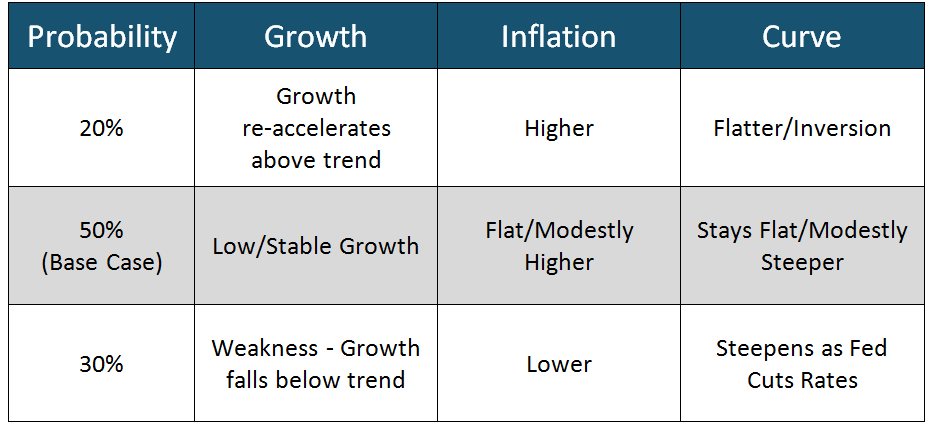

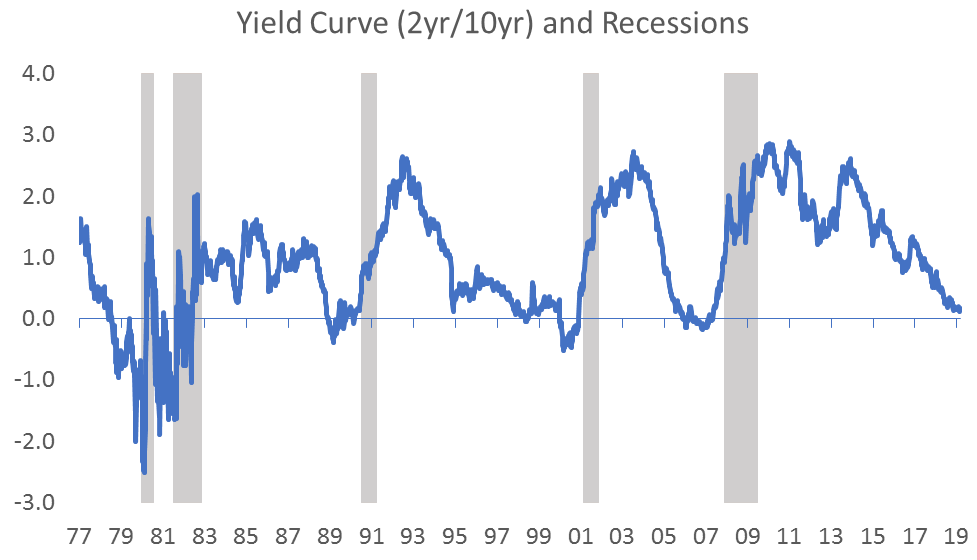

The yield curve has flattened to near zero, as it typically does during a Fed tightening cycle, usually as a precursor to an inversion and a recession. With the Fed signaling no further hikes and the U.S. still experiencing decent grow, curve inversion in the near-term appears unlikely. In fact, markets are now pricing in a probability, albeit low, of an interest rate cut as early as the end of 2019. Where we go from here requires an outlook call on growth and inflation. Below we outline our outlook in three scenarios, including their likely impacts on the curve.

Outlook Scenarios (Next 6-12 Months)

Base Case and Recession Expectations

Our base case is for low, but stable growth in the U.S.; a modest uptick in inflation, which keeps the curve flat; and a modest steepening bias possible. We see the greater risk of this backdrop eventually transitioning to weakness, rather than above trend growth, and expect the next directional move in the curve to be a steepening bias as the Fed cuts rates. This part of the scenario looks further down the road, as the curve and data suggest near-term recession odds remain low. While portions of the curve briefly inverted in March, it didn’t last more than a couple days and regardless, the lag time between curve inversion and recession or even market peaks are typically several quarters. Recent data trends in the U.S. have been improving, which has been putting more slope back in the curve, but not so strong as to put the Fed hikes back on the table and cause a flattening/inversion trend to resume.

Extending and Historical Returns

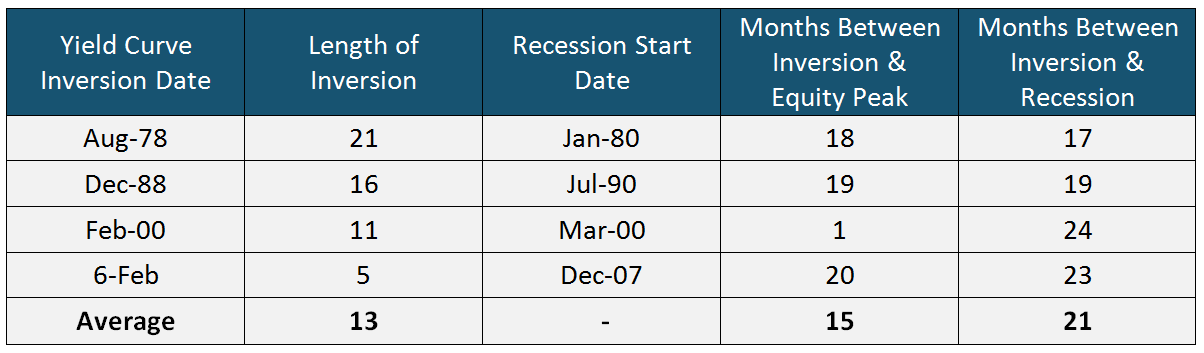

Given our outlook, the idea of at least beginning to consider a strategy extension makes sense given the higher probability of a flat-to-modest steepening environment and a more limited chance of near-term inversion or meaningfully higher long rates. We also looked at past curve environments to understand return differences historically when moving out in duration. We used the last four curve inversions referenced in the table below as a basis.

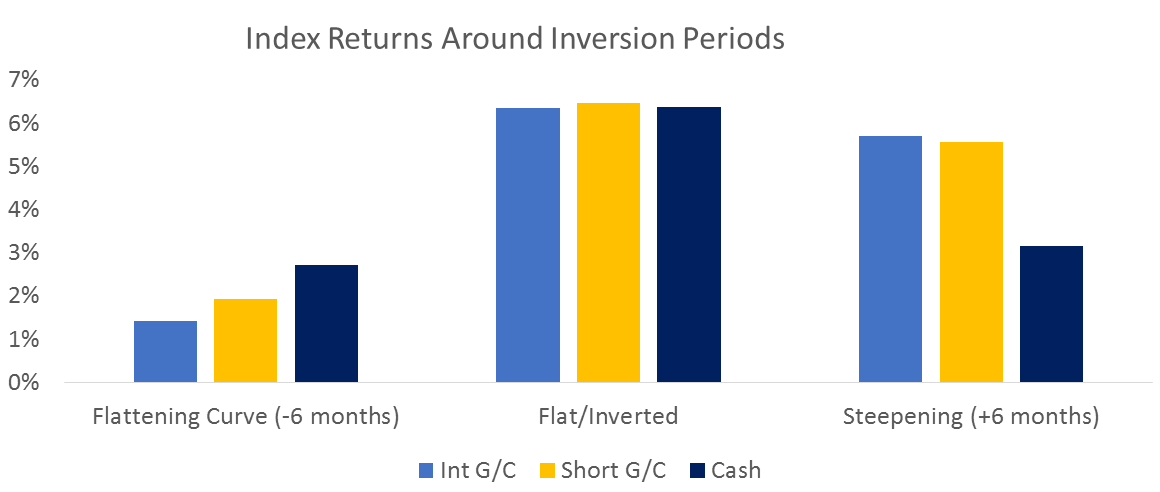

For each period, we calculated returns across cash, short gov/credit, and intermediate gov/credit across three periods:

- Flattening: 6 months leading up to the inversion

- Flat/Inverted: the inversion period

- Steepening: 6 months after the end of the inversion period

The results illustrated below also support the idea that cash makes sense in periods when the yield curve is flattening during a tightening cycle, but that post-cycle it has made sense to move out on the curve.

Conclusion

Given our current outlook, likely curve scenarios, and historical returns data, cash and ultra-short strategies still makes sense, but investors should start considering at least a push out to short strategies. Further, as the curve continues to steepen near-term, the risk/reward will become increasingly favorable for extending to an intermediate duration strategy.

This article was written by the team at Sage Advisory, a participant in the ETF Strategist Channel.

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our web site at www.sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.