By Dan Suzuki, CFA, Deputy Chief Investment Officer

We’ve all heard the famous Yogi Berra quote, “Nobody goes there anymore. It’s too crowded.” Investors today seem jazzed up on an opposite but similarly absurd concept: Wall Street thinks it’s a huge buying opportunity because everybody’s too bearish.

We think true investor capitulation is a ways off

The topic du jour is investor “capitulation,” the idea that investors have given up hope in stocks as an attractive investment. With such immense bearishness embedded into today’s stock prices, some suggest now is the time to add significant equity exposure. To be sure, markets very well may be oversold technically, and we think the long-run outlook for stock returns has improved markedly since the start of the year, but that is very different from saying the markets have bottomed. If everybody is itching to get into the market at the bottom, it probably means we are still quite a ways from true capitulation. Here are seven other signs that suggest that investors have yet to capitulate (see accompanying charts on following pages):

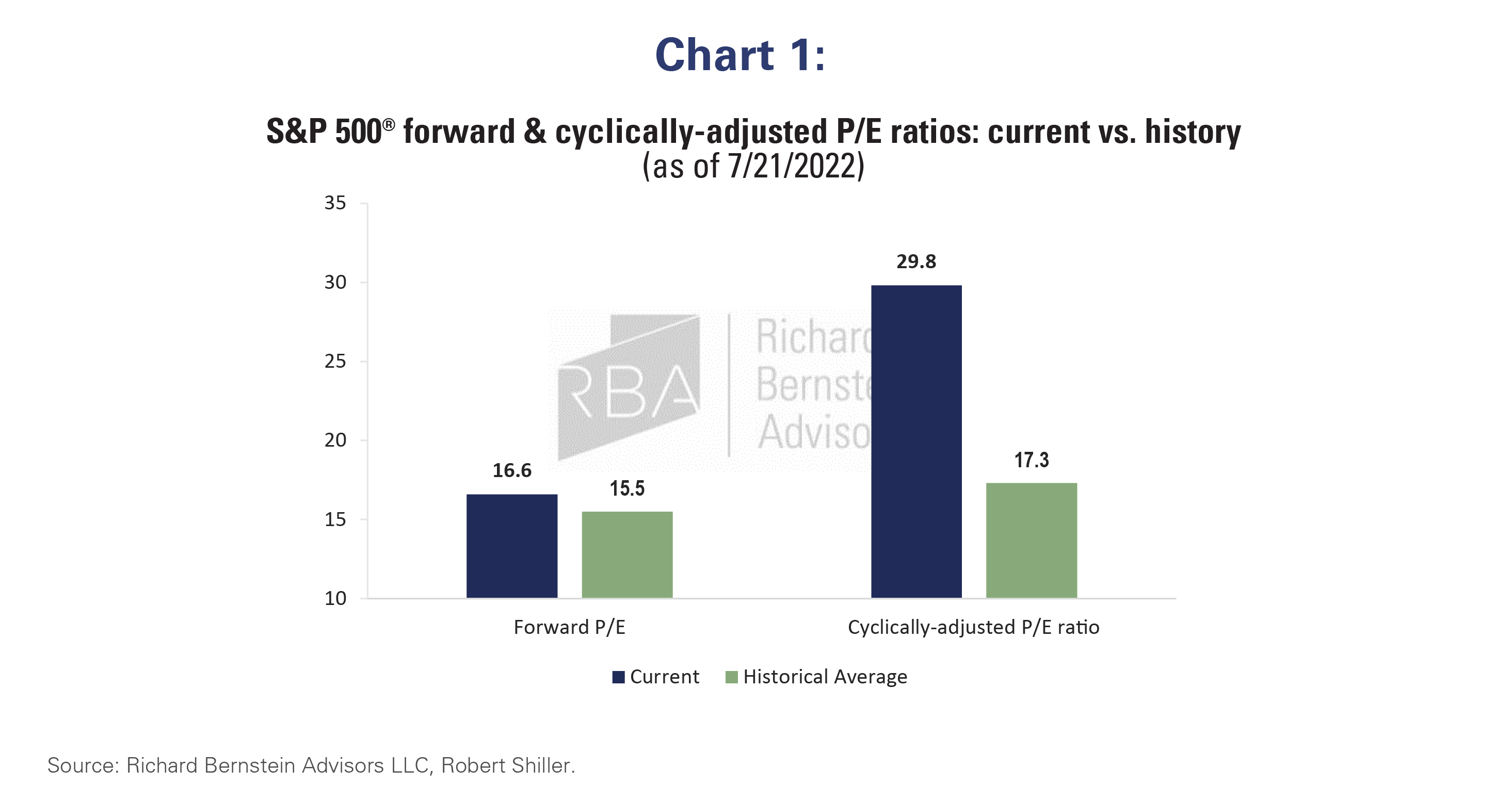

- Valuations are still elevated. While down significantly from the peak, the S&P 500® still trades at a premium to history on forward P/E (16.6x vs. the long-term average of 15.5x) based on EPS forecasts that are still near a potential cyclical peak. Stocks also trade rich on a cyclically-adjusted basis, which admittedly has its flaws (29.9x vs. long-term average of 17.3x). (Chart 1)

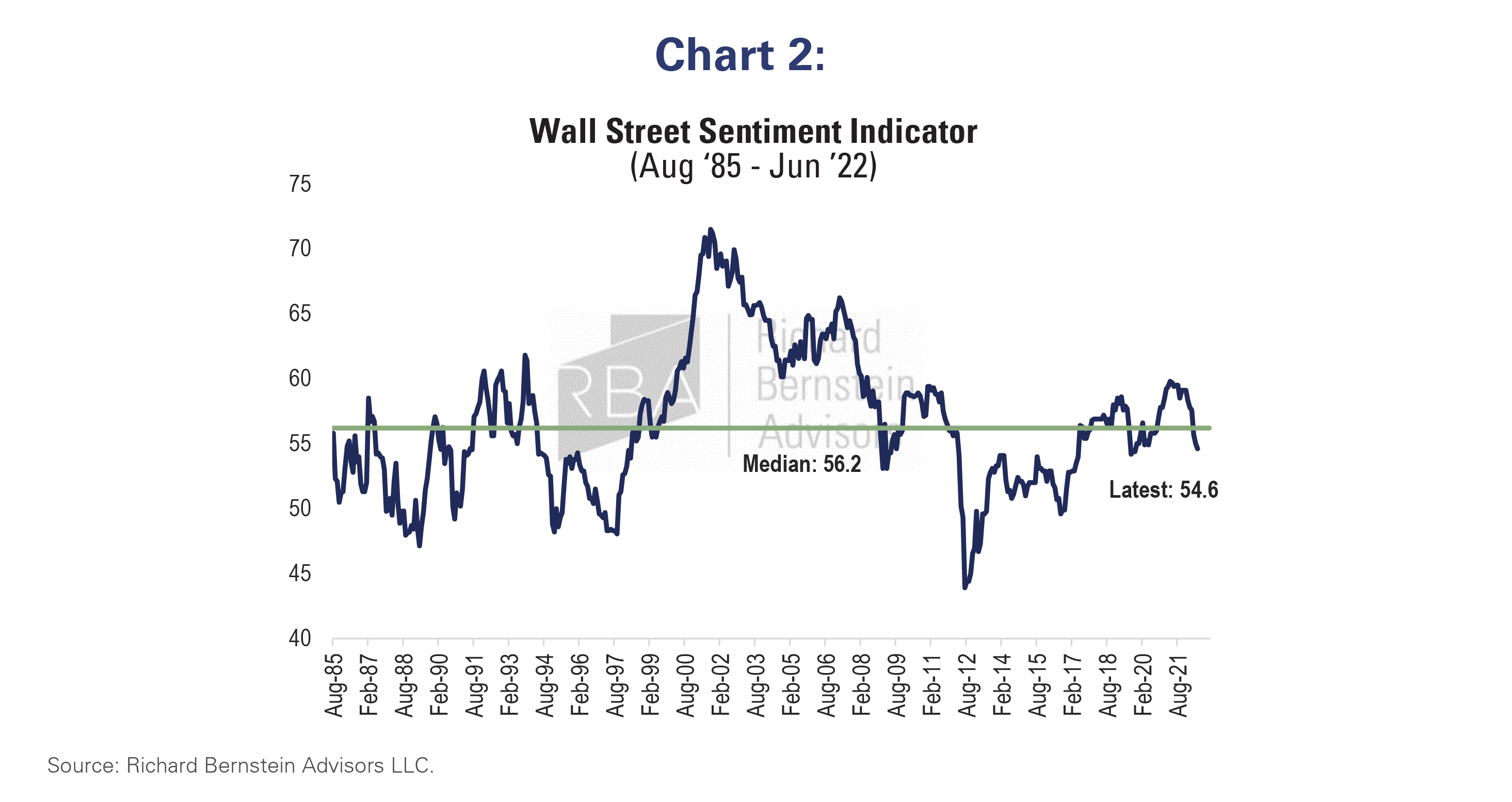

- Wall Street is pretty neutral on stocks. While Wall Street strategists have gotten more cautious, their recommended equity allocation of 54.6% is only slightly below the long-term median of 56.2%. (Chart 2)

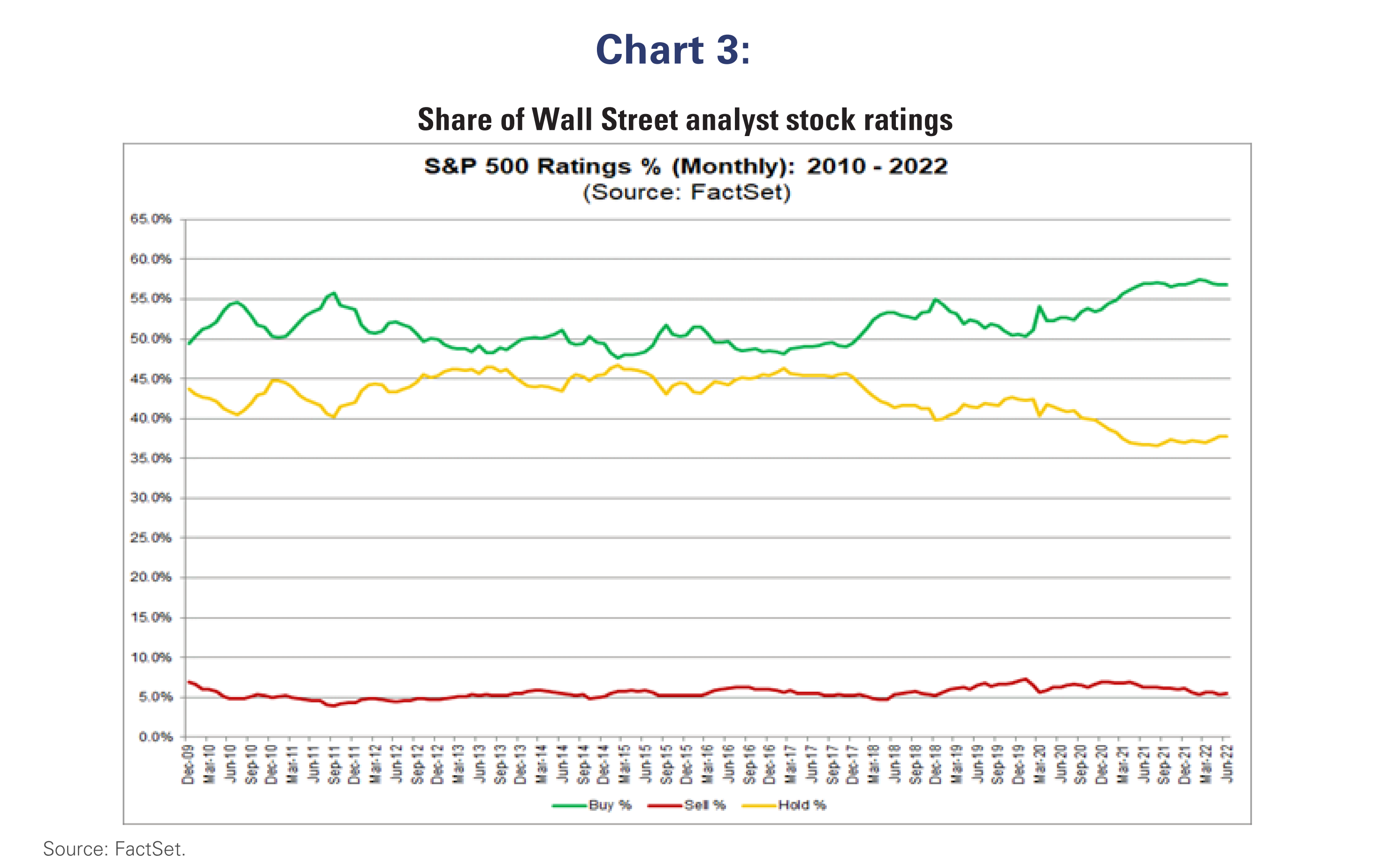

- Analysts are the most bullish in a decade. Of all the Wall Street analyst ratings on stocks, 57% are Buy ratings vs. the 53% 5-year average, near the highest in over a decade. (Chart 3)

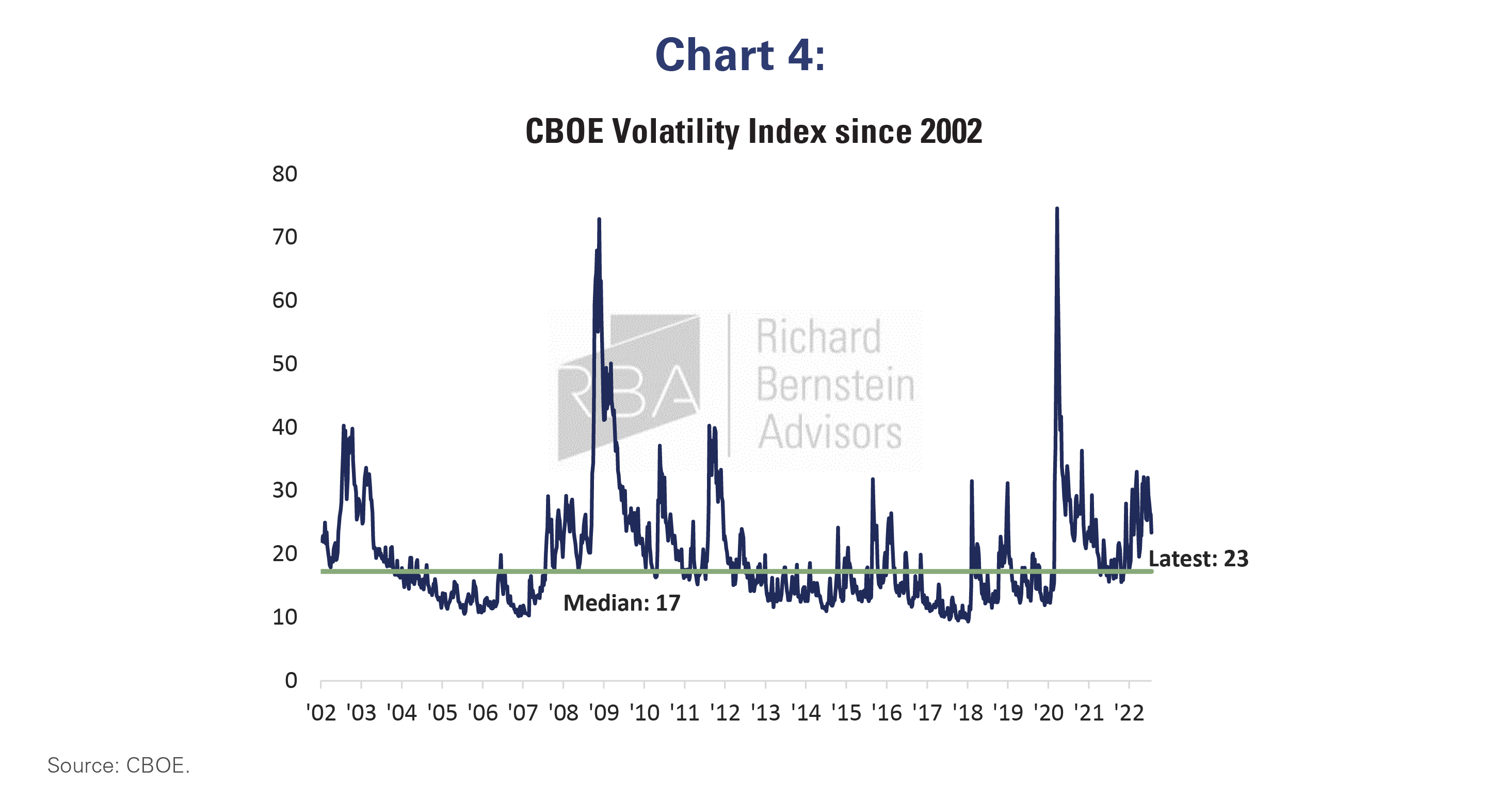

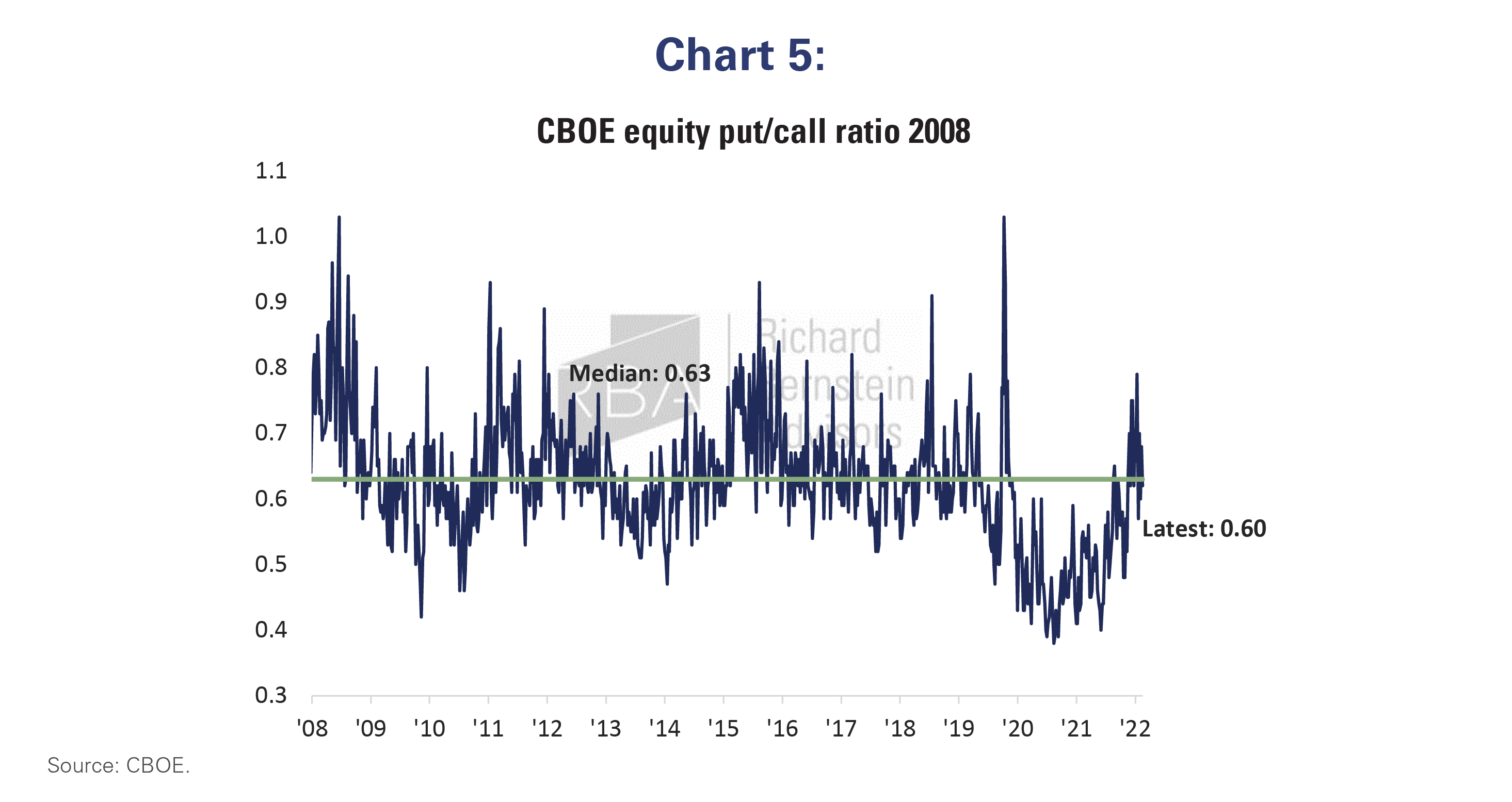

- Traders aren’t panicking. The CBOE Volatility Index (VIX) below 25 and CBOE ratio of equity puts to calls below its historical median suggests that traders aren’t panicked or fleeing for downside protection. (Charts 4 & 5)

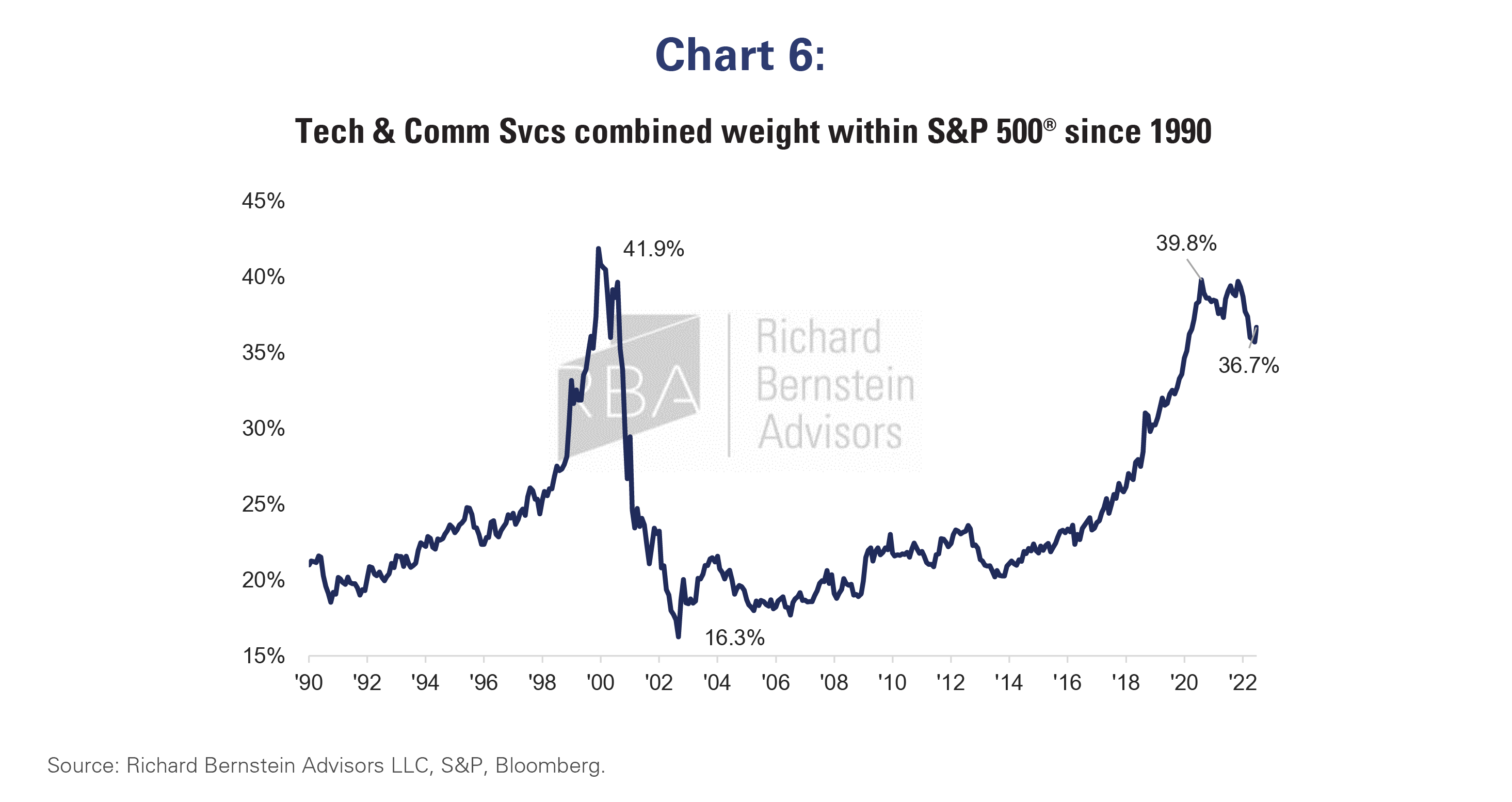

- Bubble stocks still dominate portfolios and headlines. Despite the bear market and ever-tightening liquidity, the market’s concentration in bubble stocks has barely budged from the peak. In the last Tech bubble collapse, the share of the S&P 500® market cap in Tech and Telecom stocks went from 41% to 16%. This time it’s only gone from 40% to 37%. (Chart 6)

- US household equity allocations are near record highs as of the first quarter. Even if these fell by as much as the biggest quarterly drop in history (during the pandemic), they would still be in the 92nd percentile of their historical range. (Chart 7)

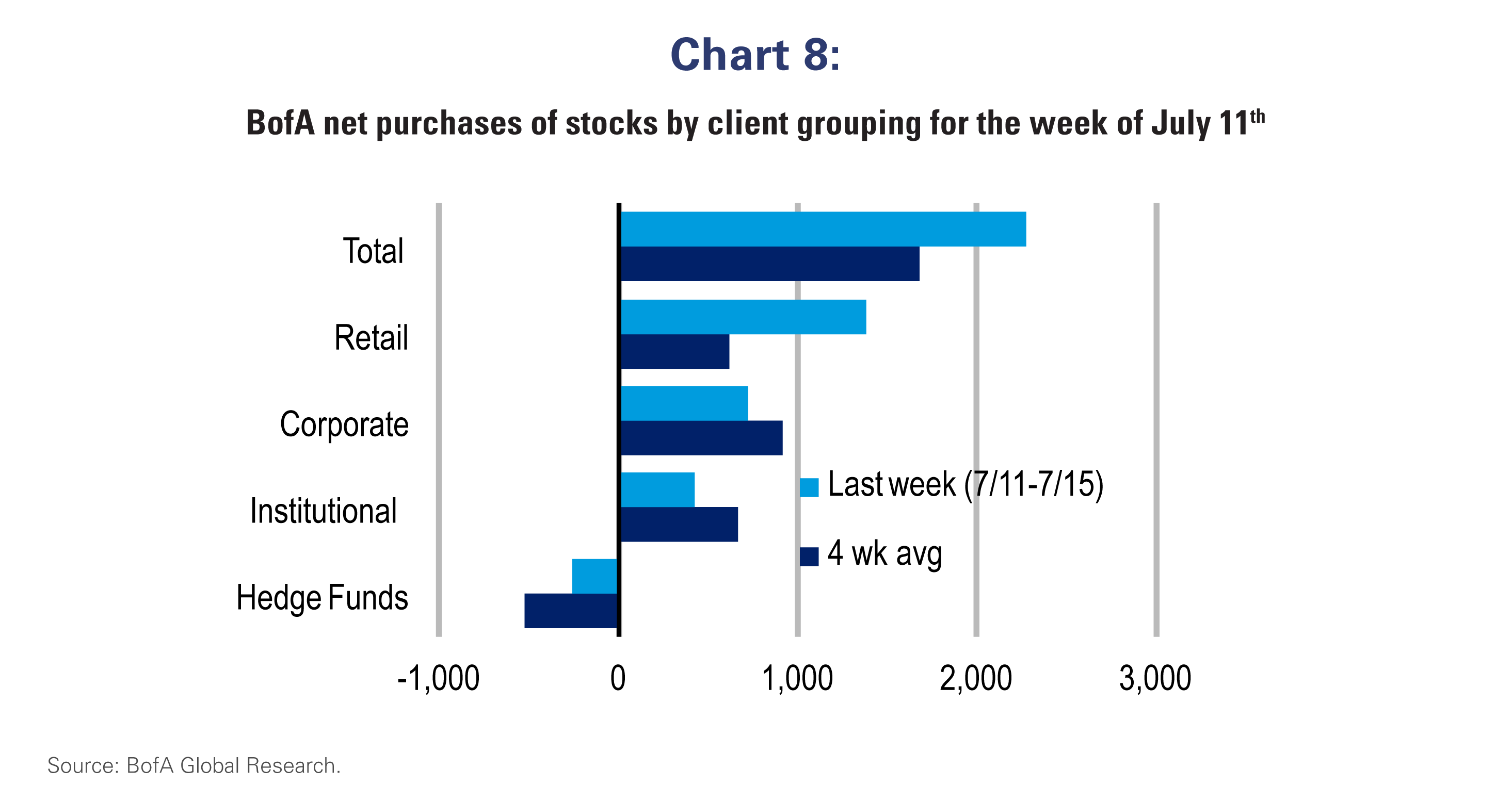

- Investors are still buying. Perhaps most importantly, it is hard to call for capitulation when investors are still buying stocks. According to Bank of America, their client equity flows actually accelerated last week to $2bn, with participation from all client types except hedge funds. (Chart 8)

Please feel free to contact your regional portfolio specialist with any questions:

Phone: 212 692 4088

Email: [email protected]

Dan Suzuki is registered with Foreside Fund Services, LLC which is not affiliated with Richard Bernstein Advisors LLC or its affiliates.

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. RBA information may include statements concerning financial market trends and/or individual stocks, and are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment which may differ materially and should not be relied upon as such. The investment strategy and broad themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information contained in the material has been obtained from sources believed to be reliable, but not guaranteed. You should note that the materials are provided “as is” without any express or implied warranties. Past performance is not a guarantee of future results. All investments involve a degree of risk, including the risk of loss. No part of RBA’s materials may be reproduced in any form, or referred to in any other publication, without express written permission from RBA. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor’s investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment’s value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment’s value. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.