By Lawrence Carrel, ETFs for the Long Run

Key Assumptions

- Income earned in an Exchange Traded Fund (ETF) retains its classification when distributed to investors.

- An investor’s unrealized capital gains in an ETF are not taxed until an investor liquidates his position, or if not liquidated, can be eliminated due to step-up provisions of the federal estate tax.

- Returns of capital are paid out of shareholder equity, which is the equivalent of an ETF’s Net Asset Value (NAV). Returns of capital are not taxed.

- With the exception of qualified dividend income (QDI), which is taxed at a reduced rate, traditional dividends and bond interest distributed by an ETF are taxed at an investor’s ordinary income tax rate.

- Capital Dividends are paid out of an ETF’s NAV and, while not taxable, reduce an investor’s cost basis in an investment.

- Lowering an investor’s cost basis in an ETF increases the capital gain on the shares when the shares are sold.

- The tax rate for long-term capital gains is lower than the tax rate on ordinary income.

SUMMARY

A return of capital is typically considered a less than desirable form of distribution from an ETF because it is drawn from shareholder equity rather than a fund’s income. However, if used correctly, paying returns of capital can be a useful strategy to minimize an investor’s taxes on the total return earned by an investment.

People who rely upon their investment portfolios to fund consumption can enhance the tax-efficiency of their spending dollar by consuming returns of capital and indefinitely deferring the recognition of capital gains.

DIFFERENCE BETWEEN A RETURN OF CAPITAL AND A TRADITIONAL DIVIDEND

Traditional dividends are distributions to shareholders that an ETF pays out of its income. In contrast, returns of capital are paid out of an ETF’s shareholder equity, or NAV. In simple terms, paying shareholders a return of capital is the equivalent of returning some or all of their investment to them.

The dividends of most real estate investment trusts (REITs) and Master Limited Partnerships (MLPs) contain a component of return of capital due to accounting depreciation, a non-cash charge that reduces taxable income without reducing the amount of cash flow that a REIT or MLP has available for distribution. However, in operating corporations that pay out dividends on a regular schedule, paying returns of capital is typically viewed as undesirable.

Operating companies hate to decrease their dividend payouts because it usually signals problems with the company’s main business. Returns of capital are typically considered an inferior way for operating companies to pay dividends because they are essentially giving shareholders back some of their own money. Using return of capital to make a dividend payment may mean an operating company didn’t earn enough profit to provide enough cash for the dividend payment.

RETURN OF CAPITAL OFFERS TAX BENEFITS

In the case of an ETF, however, a sophisticated fund manager can use return of capital to lower the taxes an investor incurs on the total return generated by the ETF.

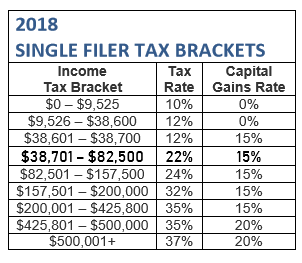

With the exception of QDI, which is taxed at a reduced rate, traditional dividends from stocks and interest paid from fixed-income securities are taxed at the investor’s ordinary tax rate. In 2018, ordinary income tax brackets range from 10% to 37%, depending on the individual’s annual income. Short-term capital gains, or profits on investments held less than one year, are also taxed at the investor’s ordinary tax rate.

However, long-term capital gains, the profits on investments held longer than one year, are taxed at lower rates, either 0%, 15%, or 20%, depending on the investor’s taxable income and filing status.

Returns of capital are not taxed at all because they aren’t income or profits from the investment, but rather a return of an investor’s own money.

For instance, if an investor bought 1,000 shares of an ETF called ABC Fund at $100 per share, the initial capital investment would be $100,000. If the investment paid

an annual income distribution of $7,000. That income would be taxed at the investor’s ordinary tax rate.

However, assume that $7,000 distribution was a combination of $3,500 income from the investment, either dividends or interest, and $3,500 return of capital. The investor would only pay taxes on the $3,500 of income because return of capital isn’t taxed. This would lower the amount of the distribution that is taxable in one way or another by 50%. The total distribution is still the same, but the tax consequences differ. Furthermore, by favoring an investment strategy that can produce capital growth using a structure than minimizes realized capital gains, the investor can defer taxes on capital growth and even, potentially, avoid such taxes completely.

RETURN OF CAPITAL LOWERS THE INVESTMENT’S COST BASIS

Distributions that include a return of capital reduce an investor’s cost basis in the investment.

Returning to the example above, the investor’s cost basis for the purchase of shares of ABC Fund was $100,000 (1,000 shares times $100 per share). The annual distribution from that investment was $7,000, with $3,500 constituting return of capital. The distribution would therefore lower the investor’s cost basis by $3,500, bringing it down to $96,500 ($100,000 minus $3,500).

For the sake of simplicity, let’s assume the investor is the only shareholder of ABC Fund and that during the period covered by the distribution, ABC Fund generated investment income of $3,500 and experienced $3,500 of unrealized capital gains in its investment securities. In other words, let’s assume ABC Fund increased in value by a total of $7,000 during the period.

While funds generally must distribute investment income annually, ABC Fund has some flexibility in choosing how to fund its $7,000 distribution for the period. One approach would be to sell its appreciated securities and distribute $3,500 in investment income and $3,500 in capital gains to investors. With this approach, the entire distribution would be taxable either as income or capital gains. Alternatively, ABC Fund could elect to retain its appreciated securities and instead distribute $3,500 in investment income and a $3,500 return of capital (either from cash on hand or by selling unappreciated securities). With the latter approach, the investor would not pay tax on the $3,500 return of capital but would instead experience a reduction in his cost basis from $100,000 to $96,500.

On a pre-tax basis, the investor’s position is unaffected by how ABC Fund chooses to fund the distribution. The investor began with a $100,000 investment, which grew by $7,000 during the period, and is now receiving a $7,000 distribution. The only difference between the two approaches concerns the tax treatment of the distribution. In the first instance, the entire distribution is taxable either as investment income or capital gains. In the second instance, ABC Fund enables the investor to defer taxes on unrealized capital gains by instead funding that portion of the distribution out of paid-in capital.